/Facebook%20like%20button%20on%20keyboard%20by%20athree23%20via%20Pixabay.jpg)

Meta Platforms (META), a powerhouse in the digital ecosystem, dominates global social technology through its core Family of Apps, including Facebook, Instagram, WhatsApp, and Threads. Driven by a massive advertising infrastructure, the tech giant connects billions of users while pivoting heavily toward the next frontier of computing. Meta continues to innovate through substantial investments in artificial intelligence, digital ads, and the metaverse via Reality Labs. Capitalizing on cutting-edge generative AI tools and augmented reality, like its popular AI Glasses, the firm remains a premier player in the tech sector, positioning itself for long-term dominance across digital environments.

META Stock's Choppy Year

META stock was trading around $671 as of the morning of July 10, up 6% for the day. The stock is still well below its 52-week high of $796.25 reached on Aug. 15, 2025, with a 52-week low of $520.26 recorded on March 27, 2026. META is up approximately 2% year-to-date (YTD) but still down roughly 7% over the trailing 12 months, a notably weak stretch for a company delivering record revenue and earnings growth. With a market capitalization of approximately $1.53 trillion, META trades at a meaningful discount to its all-time closing high of $787.42, while its next earnings report on July 29, 2026, looms as a potential catalyst.

Compared to the S&P 500 Information Technology Index, which has advanced roughly 19% YTD on broad AI semiconductor and software tailwinds, META has significantly lagged its tech peers, a stark fundamental disconnect that analysts argue makes the stock one of the most attractively priced large-cap AI names in the market today.

Strong Q4 Results

In its latest fourth-quarter earnings report, Meta delivered a blockbuster revenue of $56.31 billion, registering a staggering 33% year-over-year (YoY) growth that easily beat Wall Street analysts' estimates of $55.52 billion. The company posted an official GAAP EPS of $10.44. However, adjusting for a substantial one-time $8.03 billion income tax benefit, its underlying adjusted EPS came in at $7.31. This core financial performance comfortably surpassed the consensus analyst projection of $6.66 per share, representing a decisive earnings beat fueled by a robust, broad-based recovery across its digital advertising segments.

Diving deeper into operational metrics, the tech giant reported that Family Daily Active People (DAP) hit an impressive 3.56 billion, expanding its digital footprint by 4% YoY. Monetization remained highly efficient, with ad impressions across its portfolio surging 19% and the average price per ad climbing 12%. This twin acceleration reflects a powerful health signal for online advertising, further optimized by AI conversion tools. Financially, the company sustained a powerful 41% operating margin, closing the quarter with $81.18 billion in cash, cash equivalents, and marketable securities, while generating a healthy free cash flow of $12.39 billion.

Looking ahead, management provided a confident outlook, issuing quarterly revenue guidance of $58 billion to $61 billion, signaling sustained top-line momentum. Full-year total expense guidance was comfortably maintained at $162 billion to $169 billion. Crucially, management raised its full-year capital expenditures guidance to a massive $125 billion to $145 billion to aggressively scale up AI server infrastructure and data centers. Despite this aggressive spending, executives explicitly committed that full-year operating income will exceed the previous year’s levels, demonstrating profound conviction in its long-term AI monetization strategies.

Meta to Begin Chip Production

Meta is set to begin mass production of its in-house AI chip, codenamed "Iris," as early as September, according to a Reuters report citing an internal company memo. Iris is the latest iteration of Meta's MTIA chip program, co-designed with Broadcom (AVGO) and manufactured by TSMC (TSM), with testing completed in just six weeks without any major issues identified.

The chip forms a central pillar of Meta's ambition to double its computing capacity from approximately 7 gigawatts this year to 14 gigawatts by 2026, dramatically reducing its historical dependence on third-party processors from Nvidia (NVDA) and AMD (AMD).

The memo also revealed that Meta has secured long-term multi-year supply agreements with Samsung for memory chips, SanDisk (SNDK) for flash storage, and Sumitomo Electric (SMTOY) for fiber optic infrastructure, signaling a sweeping push toward vertically integrated AI hardware self-sufficiency across its entire data center stack.

Should You Get META Stock?

Meta's targeted September production launch of its "Iris" AI chip marks a decisive step toward hardware independence, with a doubling of compute capacity to 14 gigawatts by 2026 signaling that Zuckerberg's vertical integration ambitions are moving from memo to manufacturing floor.

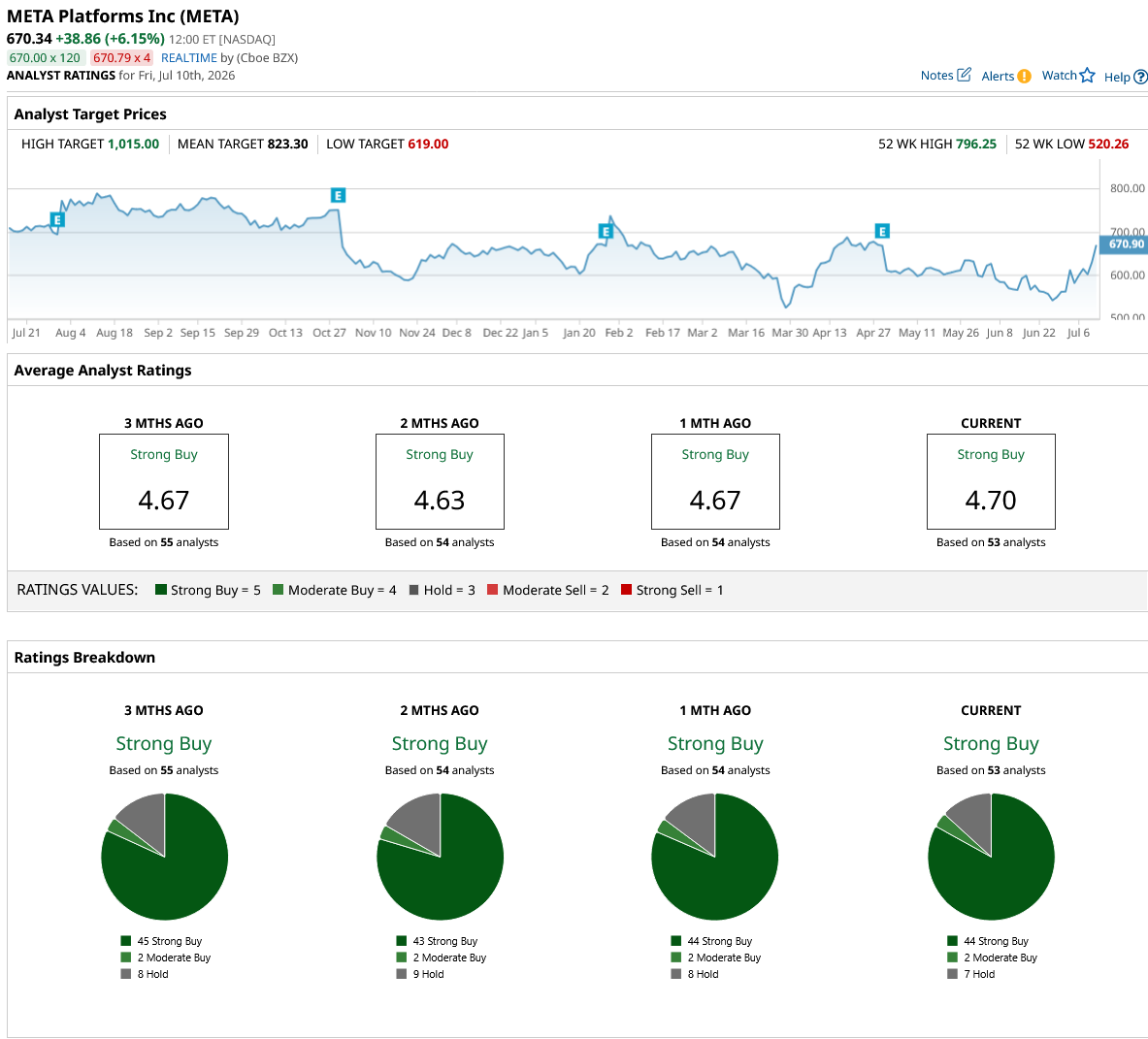

Wall Street remains firmly bullish: META stock carries a consensus "Strong Buy" rating across 53 analyst ratings, comprising 44 “Strong Buy,” two “Moderate Buy,” seven “Hold,” and zero sell recommendations. The mean price target of $823.30 implies a compelling 23% upside from current levels, suggesting that now may be an attractive entry point as the social media juggernaut starts properly executing on its AI ambitions.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)