/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)

The tech sector is heading into the second half of 2026 with investors on edge. The iShares Expanded Tech-Software Sector ETF (IGV) recently fell into bear-market territory, one of its sharpest drops since the financial crisis, after a “death cross” pushed many traders to pull back. Even Microsoft (MSFT), one of the biggest weights in the group, saw shares drop 10% when Azure growth slowed only slightly from 40% to 39%.

Apple (AAPL) had seemed to stand apart from this reset. AAPL stock hit record highs earlier this month, driven by steady iPhone demand and faster growth in its high-margin Services business. But signs of strain are starting to show. Apple now trades at about 36 times forward earnings. That's a rich valuation multiple at a time when rising memory costs are squeezing margins and analysts see earnings growth easing to 10% in fiscal 2027.

Right at this turning point, Hedgeye analyst Felix Wang flipped Apple from a long to a short, adding AAPL as a new short idea on July 9 with roughly 23% downside risk in view. Wang, who had previously been early in calling Apple’s upside, is now calling the end of the supercycle story.

With tech already under pressure and Apple priced with little room for disappointment, is Hedgeye’s bearish move a real warning that AAPL stock’s run is near its peak? Let’s take a closer look.

Financial Trends Behind the Call

Apple makes and sells consumer electronics, software, and services, with the iPhone still driving most of its revenue and a fast-growing Services business helping smooth out the ups and downs.

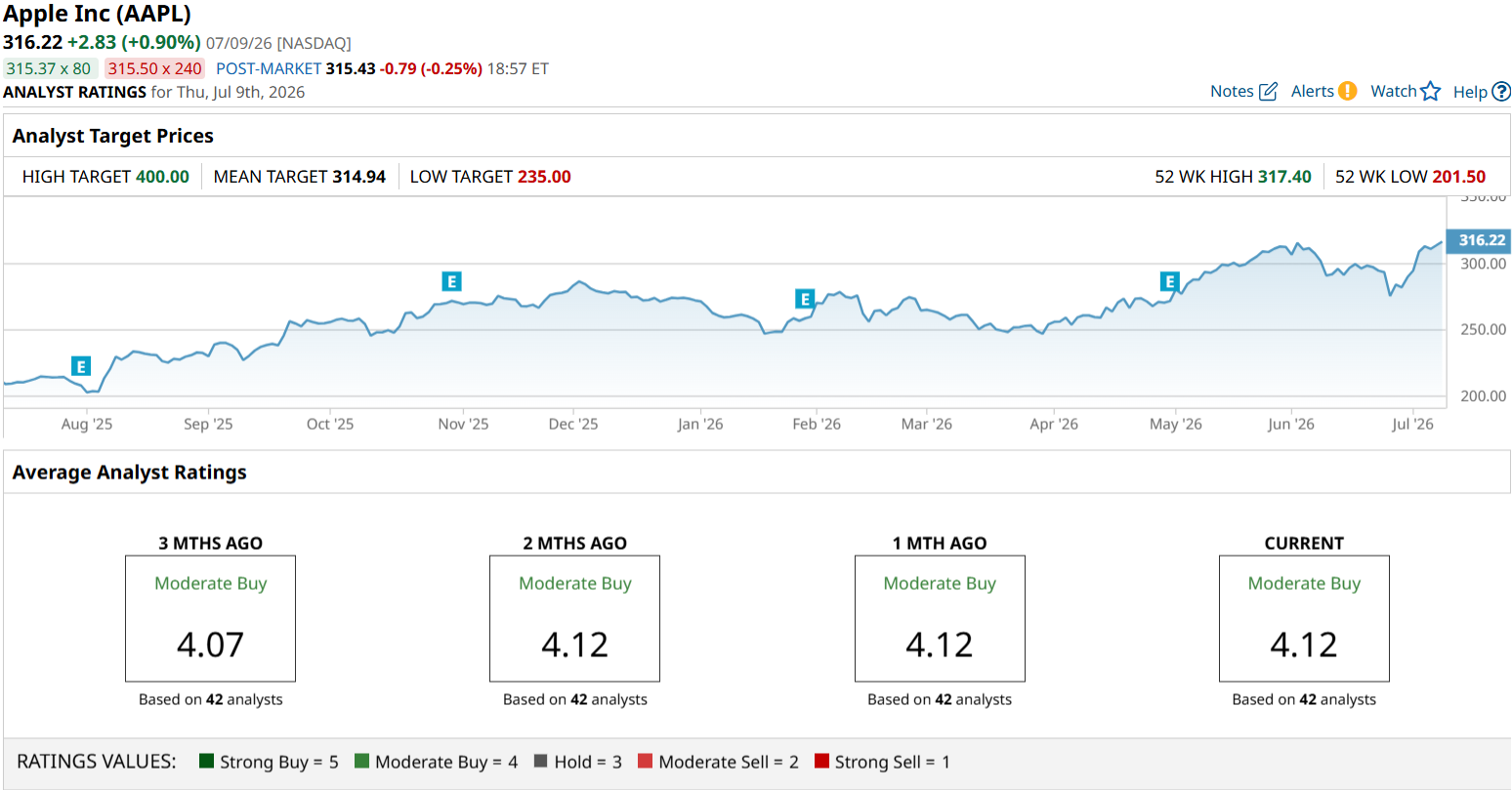

AAPL stock has had a strong run. Shares are up nearly 50% over the past 52 weeks and about 17% year-to-date (YTD), but the price has started to stall near recent highs around $317, putting the strength of the bull case to the test.

The valuation is part of that tension. Apple trades at a forward price-to-earnings (P/E) ratio of 36.1 times, well above the tech sector median of 24.5 times, so there is not much cushion if growth slows.

The latest numbers tell a similar story of strong results with a few yellow flags. In the fiscal second quarter of 2026, revenue hit a March‑quarter record of $111.2 billion, up 17% year-over-year (YOY), while diluted EPS came in at $2.01, up 22% YOY. Products revenue rose almost 17% to $80.2 billion, with iPhone net sales of $56.9 billion up 22%, Mac up 6% to $8.4 billion, iPad up 8% to $6.9 billion, and Wearables, Home & Accessories up 5% to $7.9 billion. Services revenue also grew 16% to $30.9 billion and reached a new high as a share of total revenue, showing how much Apple now leans on the segment to keep overall growth and margins in shape.

Growth Drivers Losing Momentum?

Apple rolled out a major Siri update at its Worldwide Developers Conference (WWDC), with the company confirming that Alphabet’s (GOOGL) Google Gemini will power key AI features through a multiyear licensing deal valued at approximately $1 billion per year for a custom 1.2 trillion parameter model. That leaves Apple’s AI story resting more on how well it integrates and monetizes these tools across its devices and services than on a big new platform it owns end-to-end.

Services remains Apple’s highest-margin business, though analysts flag a slight slowdown in App Store growth and ongoing China regulatory pressure. In response, Apple cut its mainland China App Store commission to 25% from 30% effective March 15, 2026 (and to 12% from 15% for smaller developers and certain subscriptions). A group of 48 Chinese developers filed a fresh antitrust complaint in June 2026.

At the same time, Apple still takes 30% of every dollar spent in the App Store, so even a modest cooling in App Store activity feeds straight through to one of its richest revenue streams.

What’s happening on the hardware side tells investors a lot. On the Q2 earnings call, Apple guided for double-digit revenue growth in fiscal Q3, but management made it clear the number could have been higher if not for persistent supply constraints, especially in Mac. Gross margin is guided in the 47.5% to 48.5% range for the June quarter, down sequentially from the 49.3% the company actually delivered in Q2. The team expects it will take several months for supply and demand to line up again on models like the Mac Mini, Mac Studio, and MacBook Neo, meaning that strong buyer interest is there but it can’t fully show up in results yet.

All of this lines up with why Hedgeye flipped to short. It’s another sign that the easy, straightforward growth Apple used to get from its main drivers is starting to feel more complicated.

Analysts Weigh the Bearish Shift

Apple is set to report fiscal Q3 2026 results on July 30 after the market close. Analysts expect EPS of $1.88 for the June quarter, up from $1.57 a year ago, which works out to almost 20% YOY growth. For fiscal 2026, the Street is looking for EPS of $8.74, a 17% YOY increase that still paints a solid earnings picture.

In late April, Argus Research analyst Jim Kelleher reaffirmed a “Buy” rating on AAPL stock with a $325 target, which implies modest potential upside from current levels. More recently, JPMorgan lifted its price target to $345 and kept an “Overweight” rating.

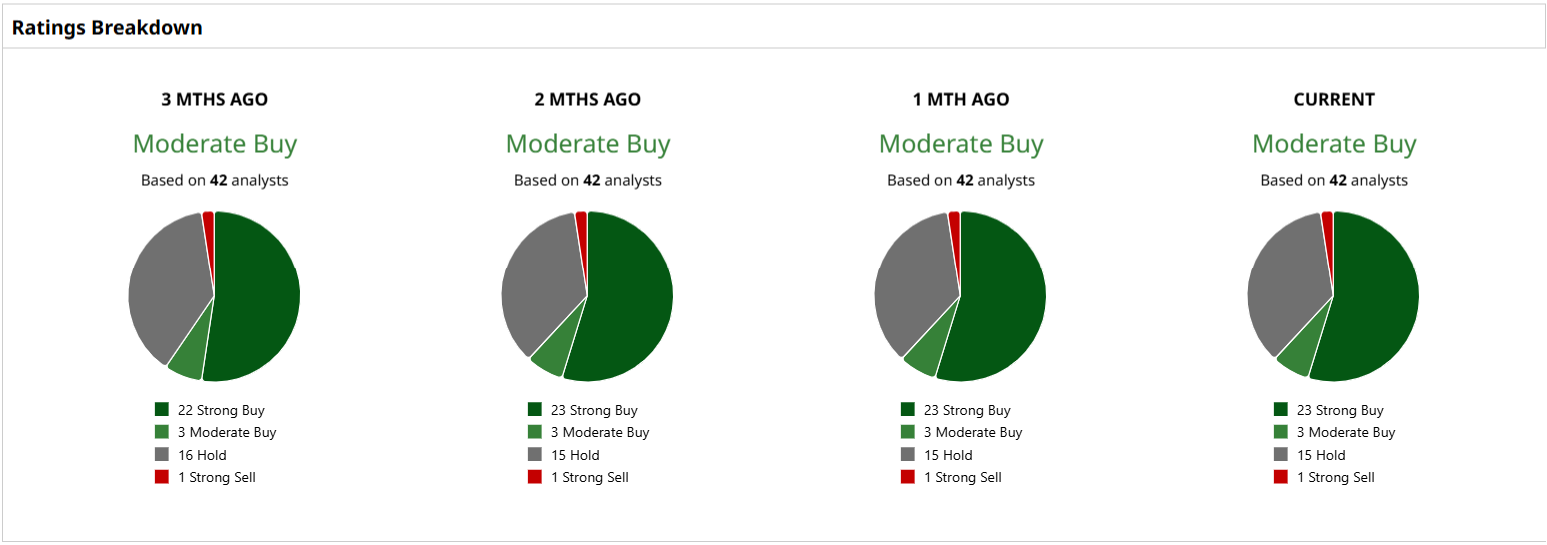

Across 42 analysts with coverage, Apple stock holds a consensus “Moderate Buy” rating. The average price target of $314.94 actually implies potential downside of less than 1% from current levels.

Conclusion

Hedgeye’s bearish turn on Apple looks less like a definitive red flag and more like a well-timed caution call. The stock is expensive, growth is moderating, and cracks in Services and AI execution are worth watching. But the broader picture still shows a company delivering solid earnings, strong cash flow, and resilient demand. Right now, this feels more like a valuation-reset risk than a structural breakdown. Most likely, AAPL stock trades sideways or pulls back modestly in the near term rather than seeing a sharp unwind, unless the upcoming earnings report materially disappoints expectations.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)