The “Magnificent 7” have held up better than many investors expected through a choppy stretch in the market, and Apple (AAPL) is no exception. The stock climbed in late 2025 on the back of strong iPhone sales, but 2026 has started on a softer note. Concerns around the delayed foldable iPhone and a lingering chip shortage have kept sentiment somewhat restrained in the near term.

Still, the long-term setup remains intact. Wedbush Securities turned more constructive on Apple after pointing to a positive signal in the company’s Mac lineup. Lead times for the Mac mini and Mac Studio now stretch weeks, and in some cases months, after orders are placed. Wedbush said that is a good sign, since it suggests demand is running ahead of supply.

For investors, it shows even with some near-term headwinds, Apple continues to show signs of healthy underlying demand.

Apple Intelligence and the Next Wave of Innovation

With a market cap of $3.8 trillion, Apple is one of the world’s most valuable tech companies. It makes iPhones, iPads, and Macs, plus services, under CEO Tim Cook. Apple thrives on design and ecosystems; people buy Apple gear and stick around for software and services.

The company’s 2026 story is being shaped by Apple Intelligence, its push into AI, along with upcoming devices such as the MacBook Neo and the iPhone 18 later this year.

At the same time, some challenges have started to surface. Analysts pointed to issues including a patent dispute in China and a slight slowdown in App Store growth, both of which raised questions around the services business. Apple also remains exposed to geopolitical risks because of its dependence on China for manufacturing and sales. Even so, the company is still active on the product front, with hiring tied to AI and reports that it is working on foldable iPhones for late 2026. New features across iOS and macOS are also expected to support the broader product cycle.

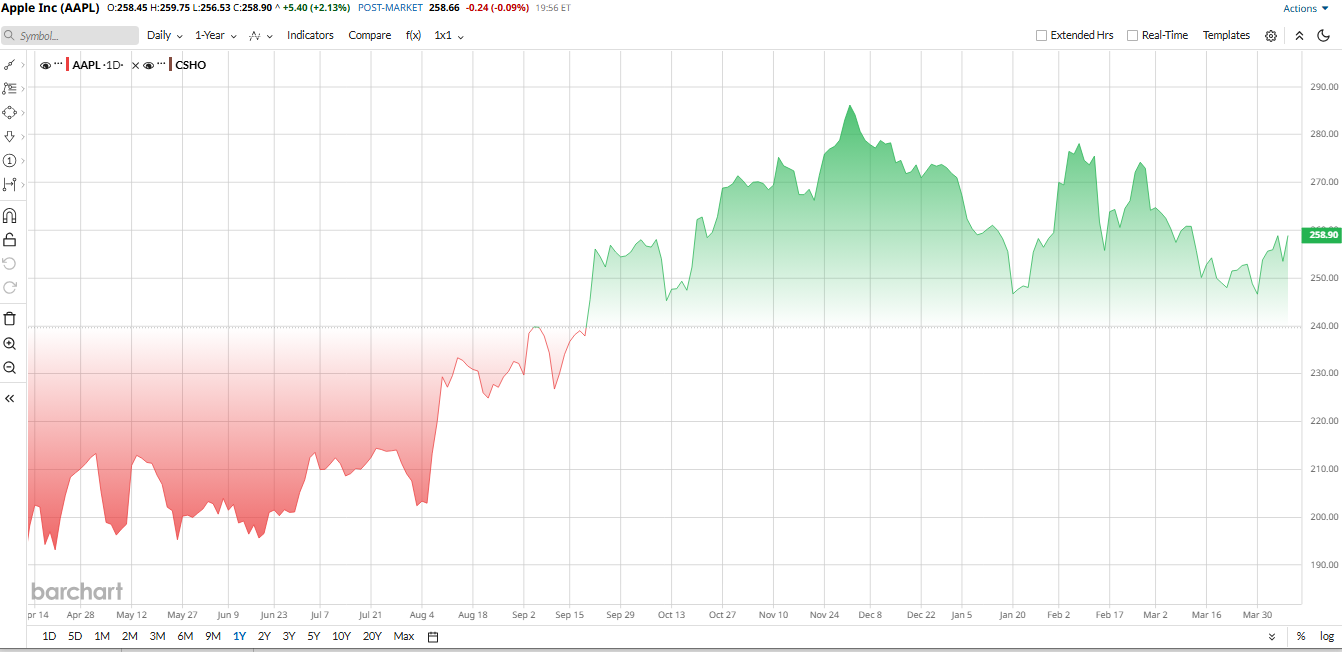

AAPL stock had a difficult first half of 2025, but it rallied sharply later in the year as China sales improved, leaving the shares up about 30% over the past 12 months. That momentum has cooled in 2026, with the stock down roughly 5% year-to-date (YTD). Still, the chart gives positive signals. Shares are trading near the 50-day moving average and above the rising 200-day average, suggesting the longer-term uptrend is still intact.

Valuation, though, is not cheap. Apple trades at a trailing P/E of about 32 times and a price-to-sales ratio of roughly 8.7 times. Both figures sit above broader tech averages and Apple’s own historical norms. Bulls argue the premium shows Apple’s strong margins, loyal customer base, and new growth drivers in AI. Skeptics, meanwhile, say the stock already prices in a lot of that optimism.

Long Mac Delays Mark “Victory”

Wedbush analyst Daniel Ives pointed out something very bullish: many Mac mini and Mac Studio models now show shipping delays of two to five months. In a note, Wedbush called these extended lead times a “victory,” meaning demand is far outstripping supply for Apple’s high-end desktops. Typically, long shipping times mean strong orders for hardware companies.

Apple’s expensive new Macs with its own chips are apparently flying off shelves, even with a global memory-chip crunch causing delays. Investors liked this news, as Apple shares jumped 2% on the Wedbush report. The market read it as evidence that customers want Apple’s latest Macs, helping revenue and margin outlooks. In other words, a solid Mac business can offset worries in other areas. It’s another sign that Apple’s strategy—making its own silicon and pushing into AI—is keeping customers engaged.

Apple Reports Record Q1 Results

Apple's first quarter of 2026 was historic. The company reported $143.7 billion in revenue, up 16% year-over-year (YoY). Profit was $42.1 billion, up nearly 19%. These set all-time highs for Apple: CEO Tim Cook noted it was a “record-breaking quarter” driven by its flagship products. In particular, iPhone sales were off the charts, and Apple had its best-ever iPhone quarter with $85.3 billion in iPhone revenue, 23% YoY.

Tim Cook highlighted the milestone: “iPhone had its best-ever quarter… and Services also achieved an all-time revenue record.” He also boasted that Apple’s active device base topped 2.5 billion, a testament to the company’s huge loyal user base. The strong growth lifted gross margins to 48.2%.

Behind the scenes, Apple generated boatloads of cash. Operating cash flow was nearly $54 billion, another all-time record. The company ended the quarter with $145 billion in cash and marketable securities and net debt of $54 billion. With all that free cash, Apple returned roughly $32 billion to shareholders via dividends and buybacks in the quarter.

Looking ahead, Apple gave relatively upbeat guidance. It projected about 13% to 16% revenue growth for the current quarter, fiscal Q2. (Apple doesn’t give full-year targets.) CFO Kevan Parekh noted these results set “a new all-time EPS record.” Analysts expect that momentum to carry forward. Wall Street’s models imply roughly mid-teens sales growth for fiscal 2026. Consensus forecasts from Barchart put FY2026 sales around the mid-$400 billion and adjusted EPS near $8.4.

Wall Street's Take on AAPL Stock

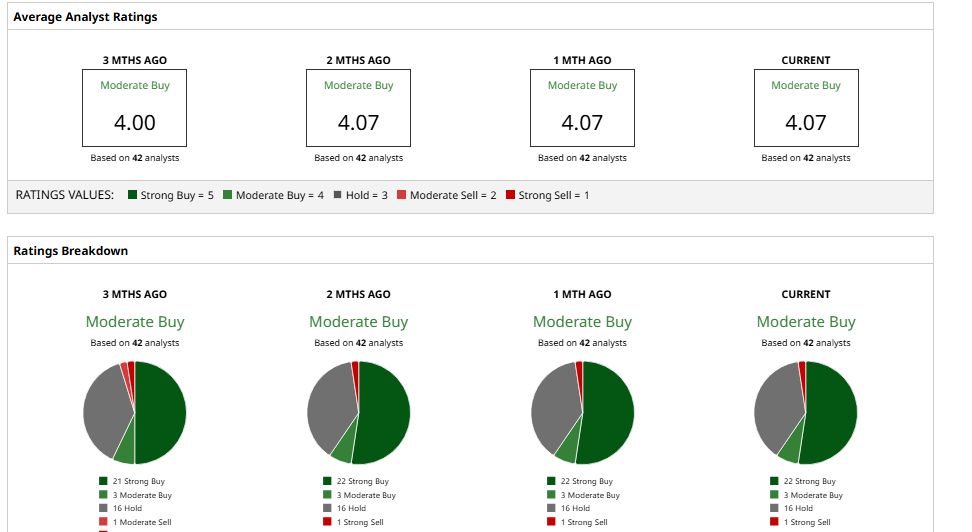

Most Wall Street analysts remain bullish on AAPL stock. The consensus among 42 analysts tracked by Barchart is “Moderate Buy.” Plus, the average price target is roughly $296, about a 14% upside from today’s levels.

Separately, many banks have revised their ratings lately. For instance, Morgan Stanley keeps an “Overweight” rating with a $315 target, citing record iPhone upgrade surveys and a rebound in China sales.

Wedbush, already upbeat on Apple’s AI plans, maintains a $350 target since late 2025, calling 2026 the year Apple’s new Siri/AI features will pay off.

Even more cautious firms like UBS rate Apple “Neutral” (price target in the mid-$200s), warning that high-margin services growth may slow

Overall, Analysts see Apple’s fundamentals as solid, so services and iPhone momentum should help earnings, and even conservative forecasts suggest low-teens growth. So while AAPL stock isn’t a value bargain, many are betting its long-term gains justify the premium valuation today.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)