/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)

Apple's stock climbed to a record high of $317.40 earlier this month, driven by resilient iPhone demand and accelerating growth in its high-margin Services business. Although the shares have pulled back, rising component costs, primarily higher memory prices, and Apple’s rich valuation dampen the bull case despite the company's strong operating performance.

Rising Memory Costs Could Pressure Apple’s Margins

Apple has consistently delivered impressive revenue growth while expanding profitability, but that trend could change. During the March quarter, management said the impact of higher memory costs on gross margins was limited because the company benefited from lower-cost inventory accumulated earlier. However, executives warned that substantially higher memory prices are expected to weigh on margins in the June quarter, with the pressure likely to intensify in subsequent quarters.

To offset rising component costs, Apple has increased prices across several product categories, including MacBooks, iPads, and home devices. Whether these price increases will fully offset higher input costs remains uncertain, especially if memory prices continue to rise.

Strong iPhone Demand Continues to Drive Growth

Despite these headwinds, Apple's core business remains exceptionally strong. The company reported fiscal Q2 revenue of $111.2 billion, up 17% year-over-year (YoY). The iPhone remained the primary growth engine, generating $57 billion in revenue, up 22% from the prior year despite ongoing supply constraints.

Demand for the iPhone 17 lineup remained healthy across major markets, including the U.S. and Greater China. Apple also reached a record active installed base for iPhones, while the number of customers upgrading their devices set a new March-quarter high. These trends suggest that demand for Apple's flagship product remains resilient.

Services Continue to Be a Profit Engine

Apple's Services segment remains a major driver of both revenue growth and profitability. Supported by an installed base of more than 2.5 billion active devices, the company continues to expand recurring revenue through subscriptions, digital content, payments, and cloud services.

During the quarter, Services revenue increased 16% year over year to $31 billion, with double-digit growth across most markets and categories.

More importantly, Services continues to lift Apple's overall profitability. Company-wide gross margin improved to 49.3%, while product gross margin declined to 38.7%. In contrast, Services' gross margin expanded to an impressive 76.7%, highlighting why the segment has become central to Apple's long-term earnings growth.

Apple’s Revenue Outlook Remains Solid

Management expects the June-quarter revenue to grow between 14% and 17% YoY. While iPad sales may face difficult comparisons because of last year's product launches, Services growth is expected to remain broadly consistent with the March quarter.

Apple's expanding ecosystem, loyal customer base, and growing recurring revenue continue to provide a solid foundation for long-term growth.

AAPL's Rich Valuation Limits Upside

While Apple's fundamentals remain strong, much of that optimism already appears reflected in the stock price. Moreover, rising memory costs could pressure product margins in the coming quarters, potentially offsetting some of the earnings benefits from the fast-growing Services business.

AAPL stock currently trades at 33.5x forward earnings, a premium valuation that looks demanding relative to its expected growth. Wall Street forecasts earnings per share (EPS) to rise 17.2% in fiscal 2026. Moreover, AAPL’s EPS growth rate is expected to moderate to 9.5% in fiscal 2027.

Final Take

Apple’s long-term prospects remain solid, supported by resilient iPhone demand, an expanding installed base, and a high-margin Services ecosystem that continues to drive recurring revenue and earnings growth.

However, rising memory costs threaten product margins, potentially limiting profitability. At the same time, Apple’s rich valuation warrants caution.

Overall, while Apple is well-positioned to deliver long-term growth, the current risk-reward profile appears less compelling at existing valuation levels and margin pressure.

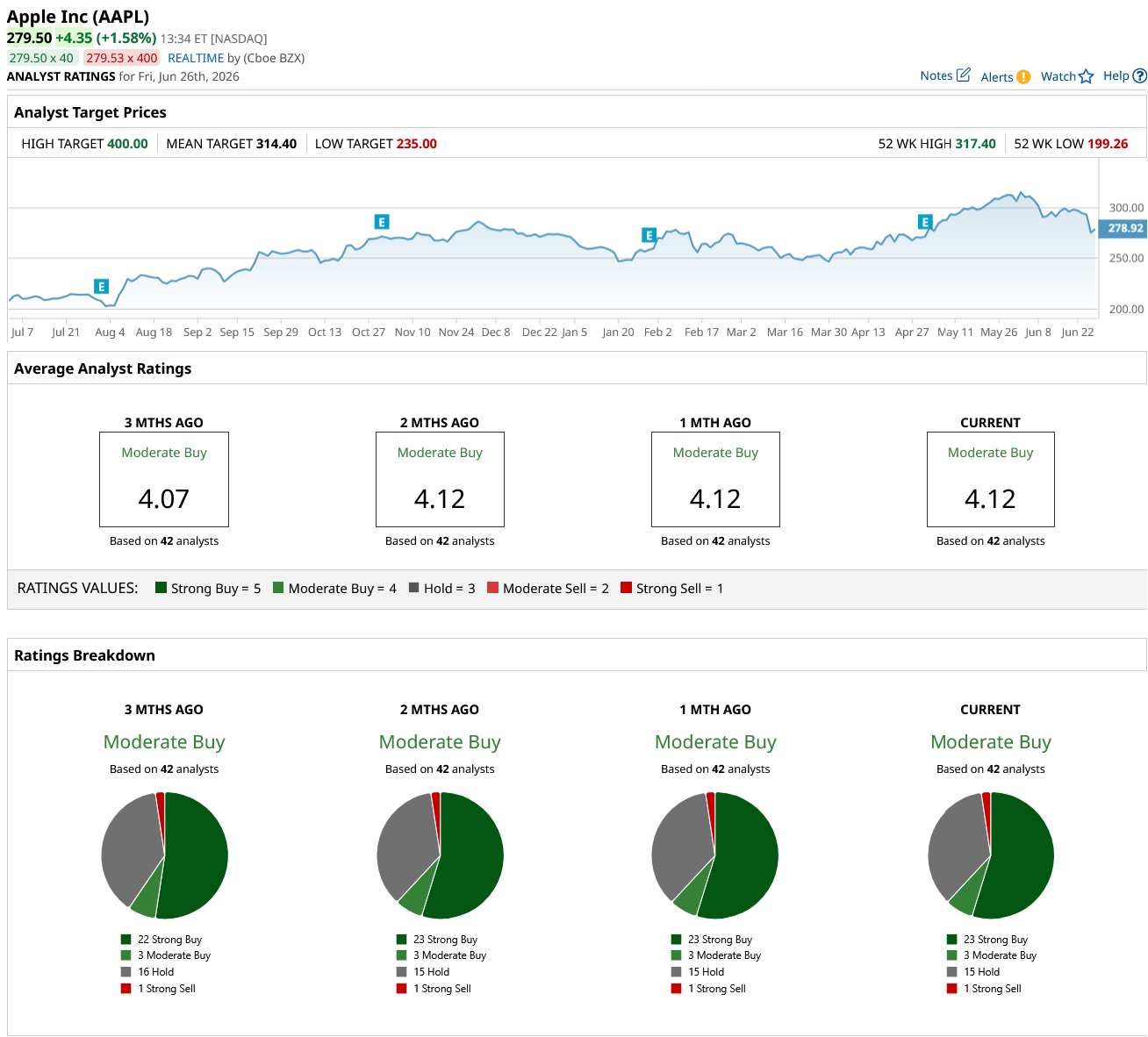

Given the short-term challenges, Wall Street analysts maintain a “Moderate Buy” consensus rating on AAPL stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)