With a market cap of $38.8 billion, Archer-Daniels-Midland Company (ADM) is a global food processing and commodities trading company that provides agricultural, nutrition, and ingredient solutions for both human and animal consumption across multiple international markets. It operates through three main segments: Ag Services and Oilseeds; Carbohydrate Solutions; and Nutrition, offering products ranging from oilseeds and vegetable oils to plant-based proteins, probiotics, and specialty food ingredients.

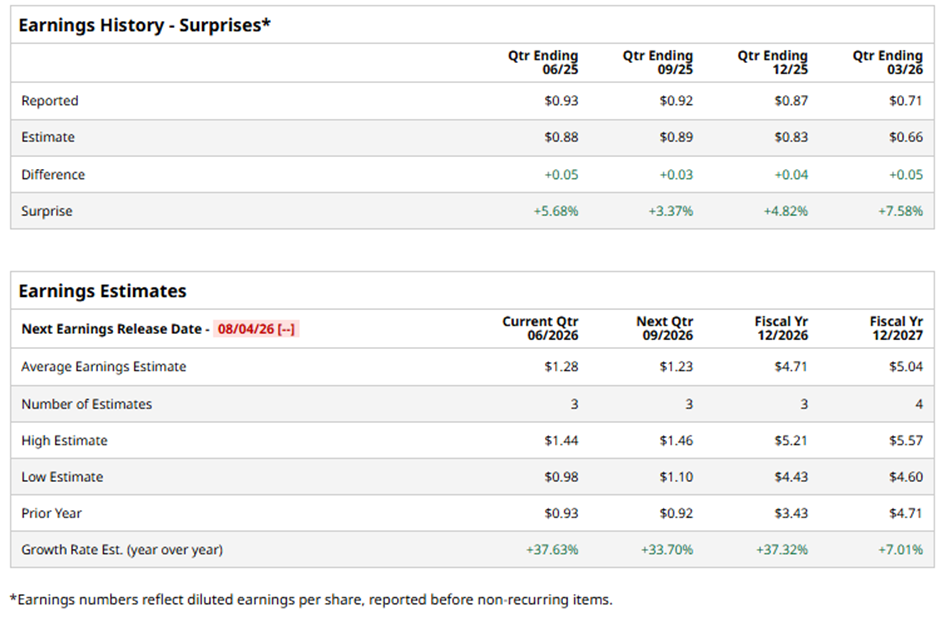

The Chicago, Illinois-based company is expected to announce its fiscal Q2 2026 results soon. Ahead of this event, analysts predict ADM to report an adjusted EPS of $1.28, an increase of 37.6% from $0.93 in the year-ago quarter. It has surpassed Wall Street's earnings estimates in each of the last four quarters.

For fiscal 2026, analysts forecast the agricultural giant to post an adjusted EPS of $4.71, a surge of 37.3% from $3.43 in fiscal 2025.

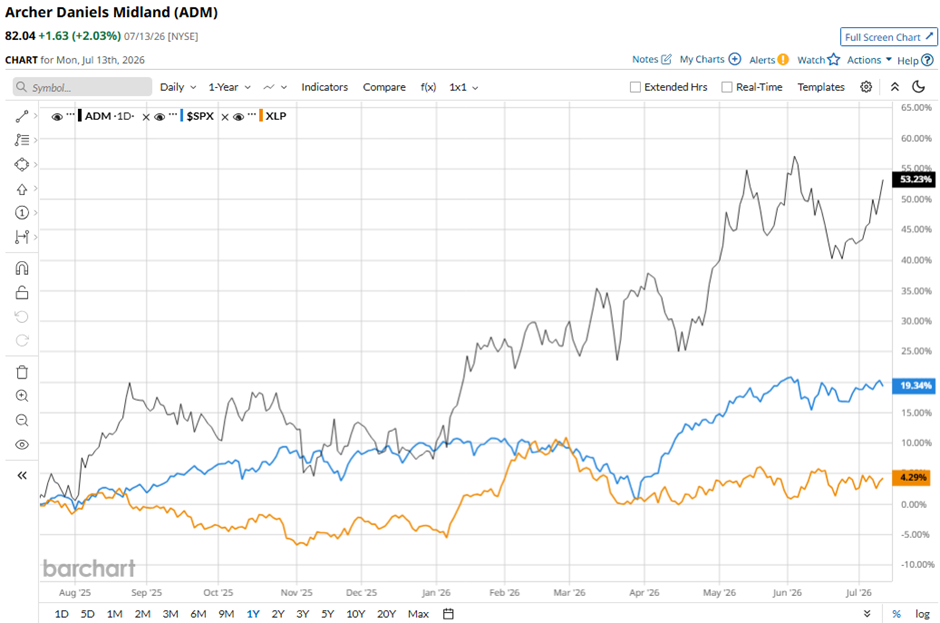

ADM stock has soared 49.3% over the past 52 weeks, exceeding both the S&P 500 Index's ($SPX) 20.1% rise and the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) 4.7% gain over the same period.

Shares of Archer-Daniels-Midland rose 3.8% on May 5 after the company reported stronger-than-expected Q1 2026 results, including adjusted EPS of $0.71, net earnings of $298 million, and a 2% rise in total segment operating profit to $764 million. Investor sentiment was further boosted after ADM raised its full-year 2026 adjusted EPS guidance to $4.15 - $4.70, driven mainly by expected earnings improvement in its crushing and ethanol businesses following supportive U.S. biofuels policy changes.

The rally was also supported by strong segment performance, including a 48% jump in Carbohydrate Solutions operating profit to $356 million and a 42% increase in Nutrition operating profit to $135 million, which helped offset a 34% decline in Ag Services & Oilseeds profit caused by approximately $275 million in negative mark-to-market and timing impacts.

Analysts' consensus view on ADM stock is cautious, with an overall "Hold" rating. Among 10 analysts covering the stock, one recommends "Strong Buy," six suggest "Hold," one "Moderate Sell," and two advise "Strong Sell." As of writing, it is trading above the average analyst price target of $78.11.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)