/AI%20(artificial%20intelligence)/3D%20Graphics%20Concept%20Big%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Marvell Technology (MRVL) has just registered a quiet win on the AI supply chain front. Tower Semiconductor (TSEM) has successfully shipped five million coherent photonic integrated circuits (PICs) to customers. Marvell, which designs optical networking products that enable high-speed optical data transfer, is a direct beneficiary of this development as it promotes the company’s ecosystem.

While the technology has already gained traction among investors as the future of high-speed data transfer, its implementation is still in the early stages. With developments like above, the thesis is only gaining strength, and with photonics already the highest-growing segment for Marvell, things could quickly shift to talk of the company’s dominant position in Photonics.

When Jensen Huang talked of Marvell being a trillion-dollar company, he was referring to the company’s strength in networking and connectivity hardware that will drive future AI data centers. With MRVL's photonics business picking up, Jensen’s vote of confidence, and an increasing willingness from hyperscalers to increase their capex no matter the cost, Marvell’s prospects look bright.

About Marvell Stock

Marvell is a semiconductor company that designs data infrastructure solutions for data centers, artificial intelligence, networking, and cloud computing. Its product portfolio includes networking processors, custom AI accelerators, storage controllers, and optical connectivity solutions. Founded in 1995 and headquartered in Santa Clara, California, the company is led by Chairman and CEO Matt Murphy .

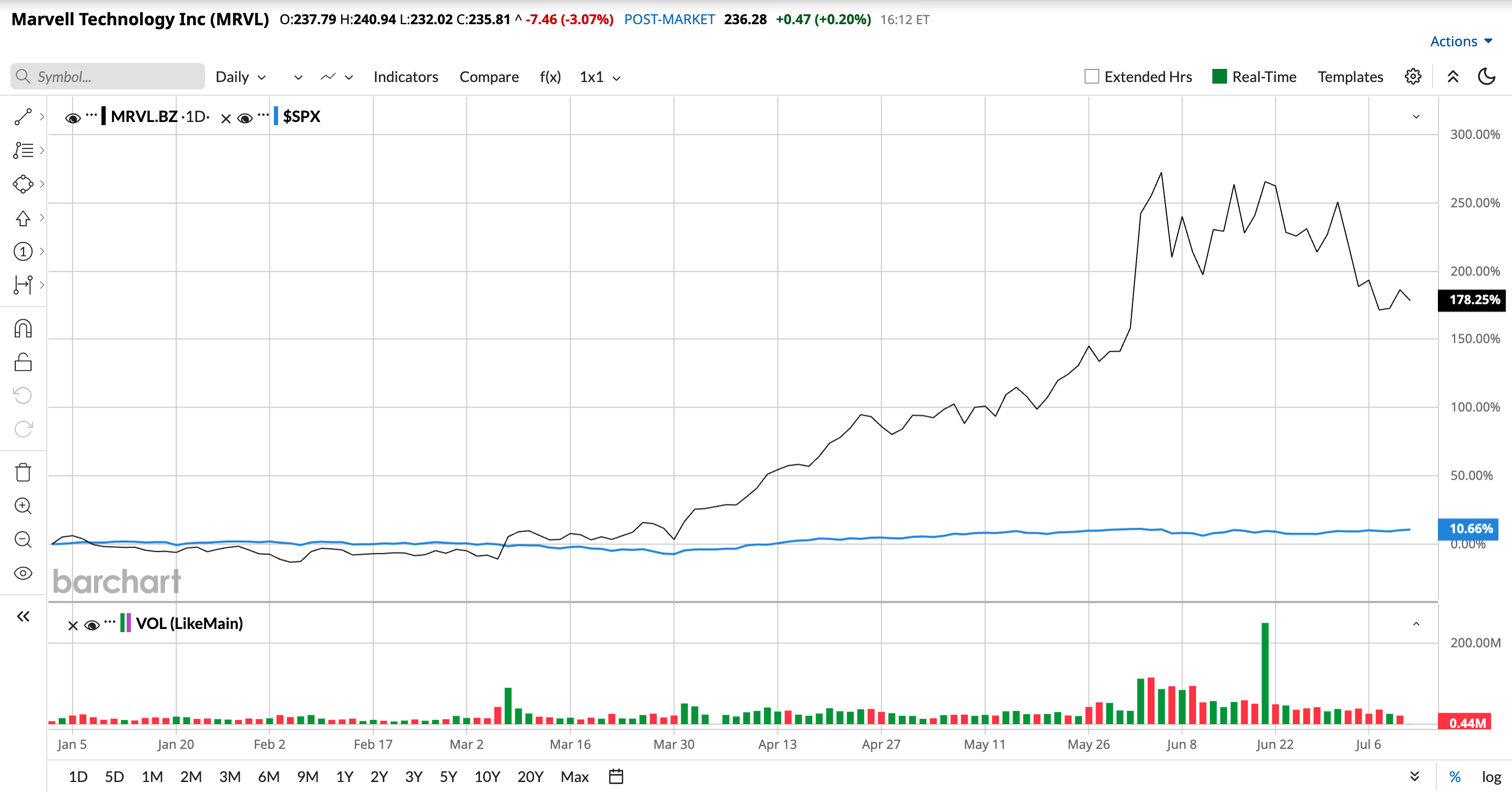

Over the last 12 months, Marvell stock has surged 223.5%, far outperforming the S&P 500 Index’s ($SPX) 20.6% gain. The stock registered most of its gains in the second quarter of the year, primarily due to the boom in AI infrastructure demand, with Marvell being a key designer of custom AI chips for major cloud providers.

Marvell’s valuation remains the most debated aspect of the stock. The forward GAAP price-to-earnings is 131.38 times, more than five times the sector median of 33.87 times, making it one of the most expensive semiconductor stocks on an earnings basis. The forward price-to-sales ratio further makes the firm look overvalued, sitting at 18.46 times, more than 6.5 times the sector median and well above the company’s 5-year average of 9.95 times. The EPS growth trajectory offers some justification for these extraordinarily high numbers, with analysts expecting a healthy growth of 43% in 2027, accelerating to 53% in 2028 and 59% in 2030. The net debt of $1.44 billion also looks easily manageable for a company with a $212.8 billion market cap. While the valuation looks steep, the estimated revenue of $16.5 billion by fiscal 2028 could significantly compress the price-to-sales ratio. For now, the valuation reflects the confidence of the investors for Marvell’s AI infrastructure momentum.

Marvell Beats Earnings Expectations

Marvell reported its first-quarter fiscal 2027 earnings on May 27. The firm marginally beat the analyst consensus on both key metrics. A record revenue of $2.42 billion was reported, up 28% year-over-year (YOY), and above the $2.40 billion consensus. The non-GAAP EPS was $0.80, compared to the $0.79 consensus. The primary driver was the data center, contributing 76% of the quarterly revenue. The company also reported a record operating cash flow of $638.8 million. During the quarter, Nvidia’s CEO publicly referred to Marvell as the next trillion-dollar company, strengthening investor confidence in the firm’s growth.

For the next quarter, Marvell guided revenue of approximately $2.7 billion, a 35% YOY growth. The firm is also expecting the revenue to grow by at least 10% sequentially in Q3 and Q4. The third-quarter revenue guidance is $3 billion, which is one full quarter earlier than Marvell previously expected, indicating faster growth than the firm’s own projections. For fiscal year 2028, the CEO states that the revenue is estimated to grow by a significant 45%, reaching an approximate $16.5 billion. Addressing an analyst’s concern about capacity and guidance, the COO confirmed that Marvell has secured enough manufacturing capacity through long-term supply agreements, and the guidance should hence be met.

What analysts are Saying About Marvell Stock

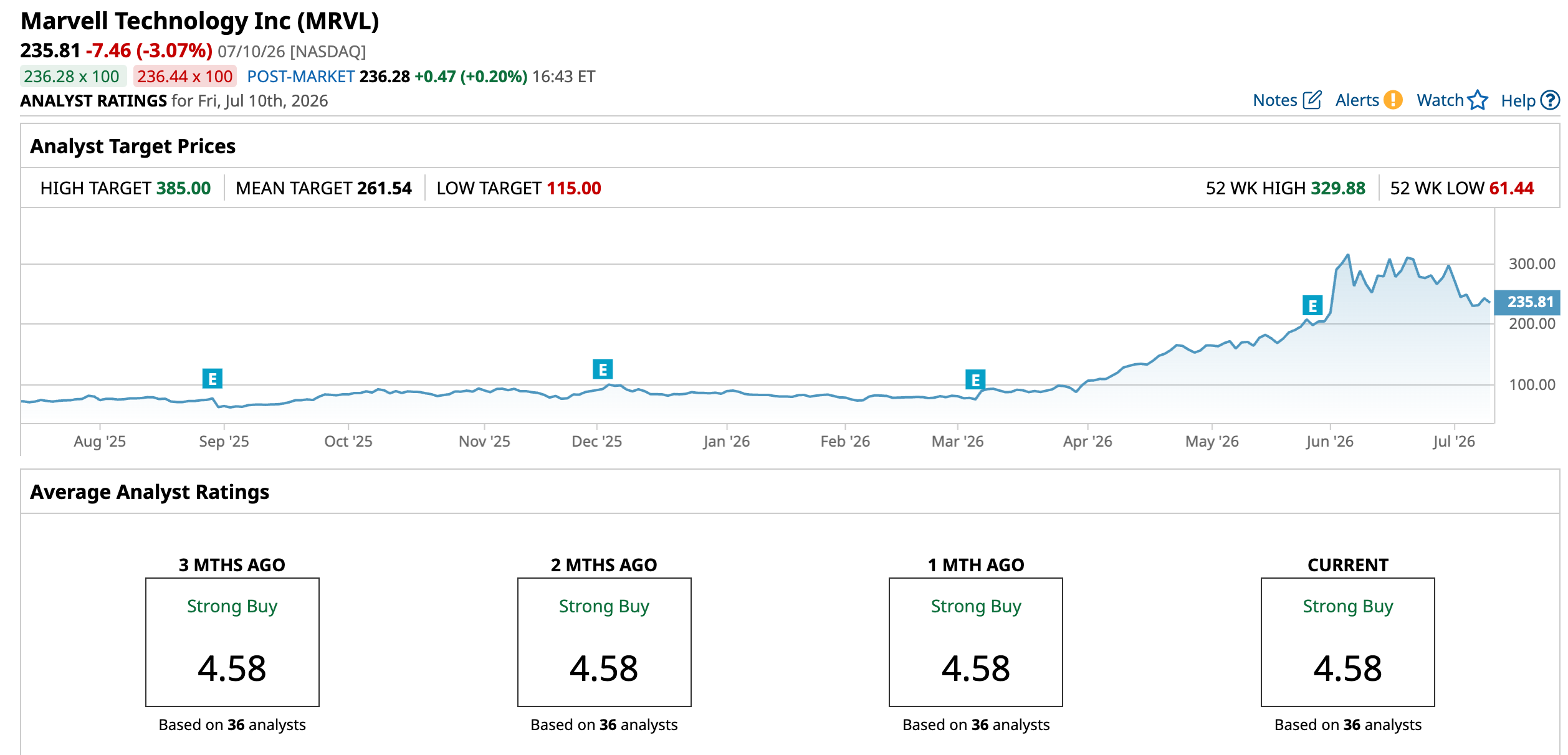

KeyBanc analyst John Vinh increased his Marvell price target from $260 to $385 while maintaining a “Buy” rating. The analyst believes Marvell’s networking business to be a long-term growth opportunity and has confidence in the firm’s strong position in the optical networking market. B. Riley analyst Craig Ellis also increased the firm’s price target from $240 to $345 while maintaining a “Buy” rating due to Marvell’s expanding collaboration with Nvidia.

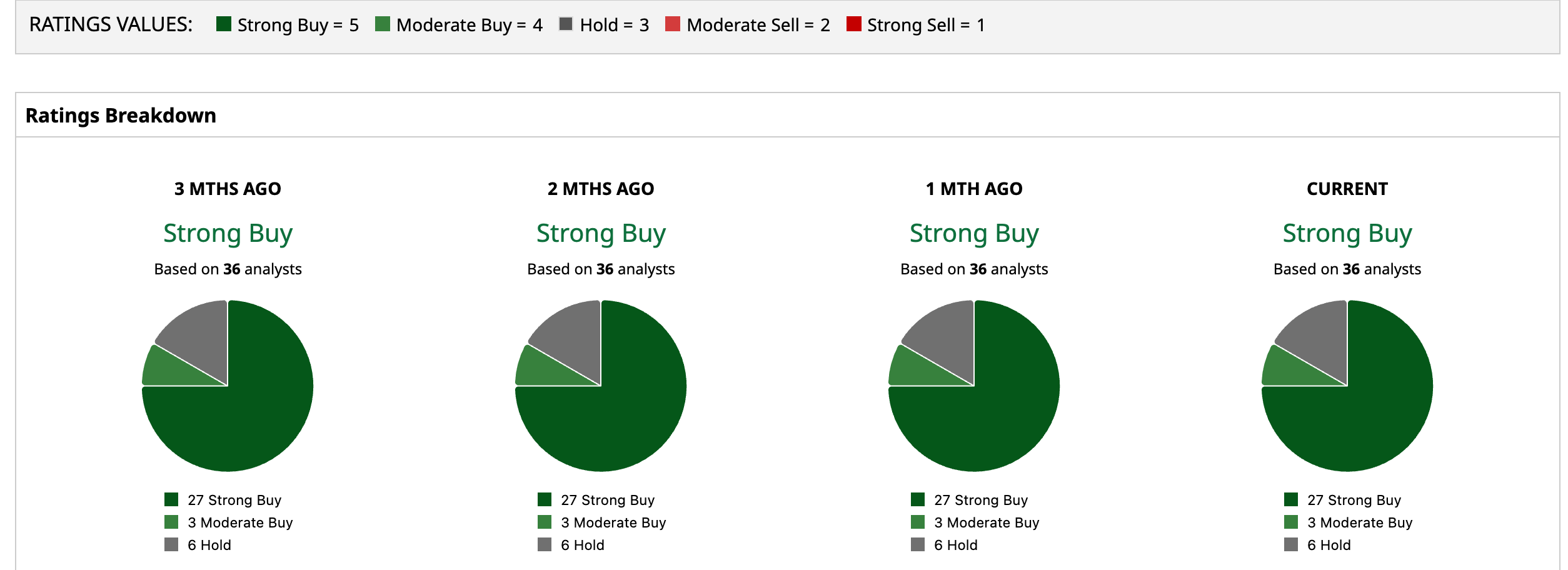

Based on the 36 Wall Street analysts, Marvell holds a “Strong Buy” consensus rating. The mean price target is $261.54, indicating an 11% upside. Meanwhile, the Street-high target price of $385 implies a possible climb of 63.3% upside over the next 12 months.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)