/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

Since its blockbuster debut on April 2, the Roundhill Memory ETF (DRAM) has shattered every historical funding record. It crossed the $1 billion mark in just its first 19 days and rocketed past $6.5 billion in assets over its first few weeks. That’s because it’s devoted specifically to the hottest segment of the hottest trade on Wall Street – memory solutions for AI.

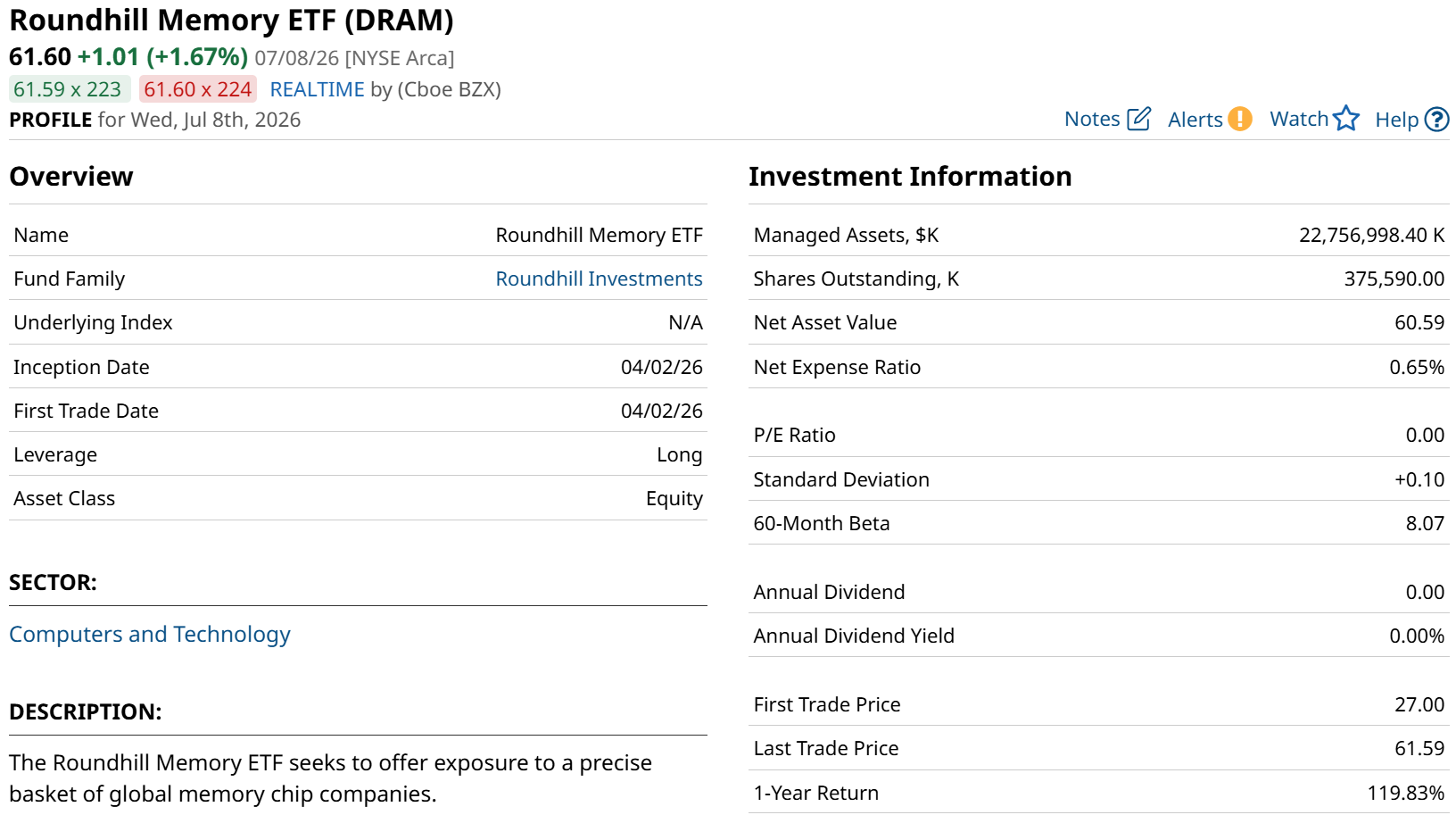

Look at where it sits today, about 14 weeks after its launch. More than $22 billion in assets. Not bad for an ETF which is about 75% allocated to just three stocks. And when we add in the next four by weight within DRAM, we get more-than-90% allocation.

There’s also a lot not to like here. For starters, I think the stocks it holds are likely to crash sooner rather than later.

Then, you can look at investors paying a 0.65% expense ratio for this ETF when you can essentially replicate its performance, fee free, by outright holding its three biggest holdings.

Until this week, its one silver lining was that DRAM provided rare access to SK Hynix for U.S. investors. The leading memory company has a thinly traded over-the-counter listing, and you can access it through a single-country South Korea ETF. But nothing quite compared to DRAM.

Before DRAM launched, if you wanted direct exposure to the high-bandwidth memory chips powering the AI boom, your choices were highly limited. You either had to put all your eggs into one basket with a U.S. stock like Micron (MU), or wade through complex international accounts to buy Asian giants like Samsung or SK Hynix. DRAM wrapped the entire specialized hardware pipeline into a single, easy-to-buy U.S. ticker.

Its top holdings are a powerful triumvirate of Samsung, Micron, and SK Hynix. DRAM is far from the traditional “diversified” ETFs we are used to. That allows investors to truly target this trio of HBM leaders.

But the memory landscape is about to dramatically change. Later this week, SK Hynix will list American Depositary Shares (ADSs) under the ticker SKHY, opening the door wide to U.S. investors. Does that make the DRAM ETF irrelevant?

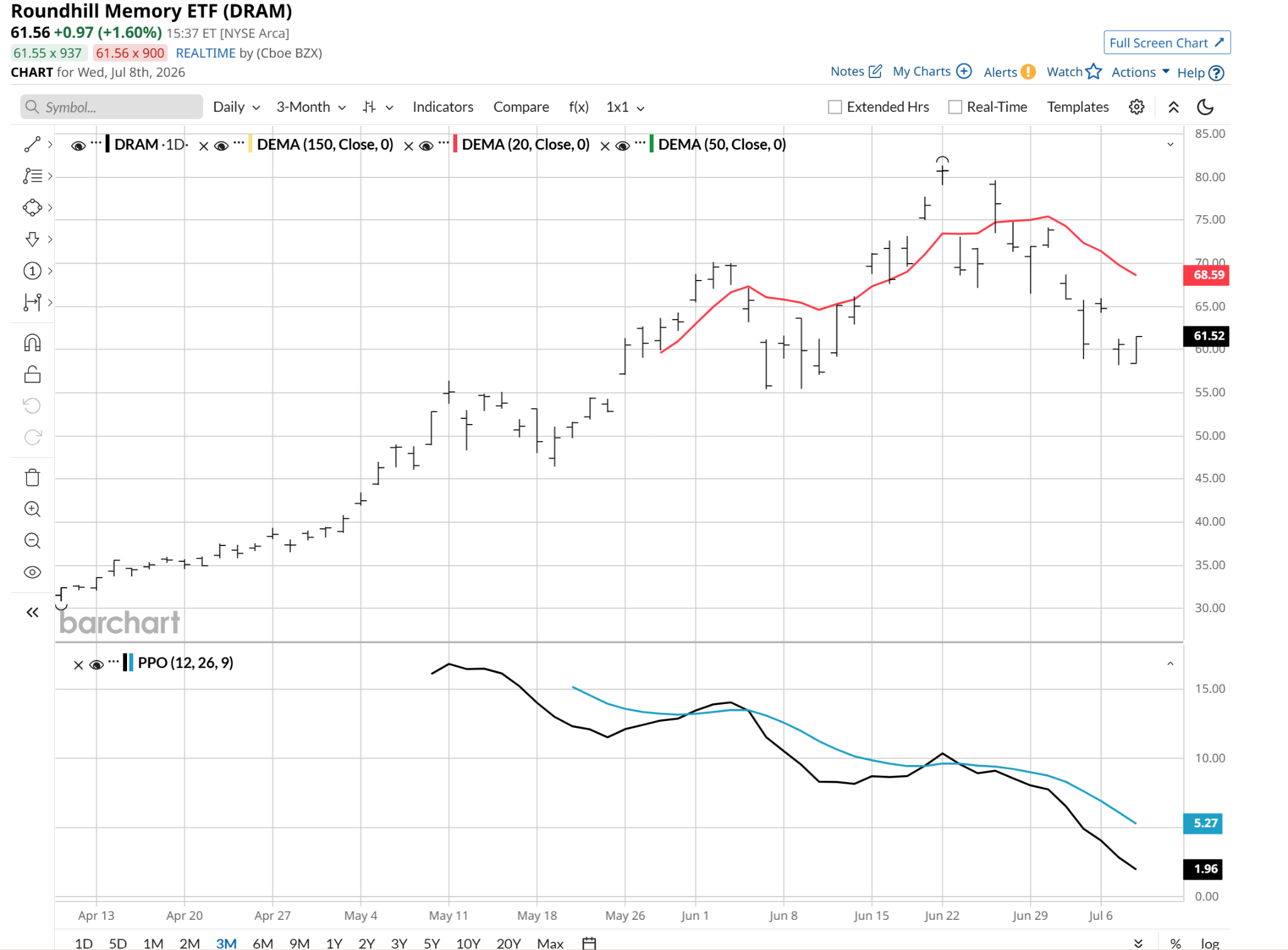

Plus, the memory chip market is famous for its extreme price swings, and the fund’s honeymoon phase is facing its first major reality check.

The primary catalyst for this recent bump came straight from South Korea, where tech giant Samsung Electronics reported preliminary quarterly financial results. On paper, the numbers looked incredible. Samsung’s operating profits jumped significantly, driven by skyrocketing global memory demand and higher microchip selling prices. Yet, instead of zooming higher on the stellar news, major memory stocks immediately faced a wave of aggressive profit-taking.

This dramatic “sell the news” reaction highlights a common trap in cyclical tech investing. Because investors had spent months aggressively buying up chip stocks ahead of these earnings releases, the blowout numbers were already fully priced into the market. The sudden drop proves that Wall Street is no longer questioning whether these chip companies are highly profitable today. Instead, big money is actively worrying about how long this massive AI demand cycle can last before supply catches up.

Adding fuel to the fire, the explosive popularity of the DRAM fund has triggered the creation of even riskier trading tools built right on top of it. Wall Street issuers recently launched (RAM) and (DRAL), a pair of 2x leveraged versions of DRAM’s portfolio. Of note, while there is an application filed for an inverse DRAM ETF, it has yet to reach the market.

While these hyper-aggressive tools are pulling in massive short-term trading volumes, they add an immense layer of risk for normal investors. When an elite, go-go market theme starts to experience heavy profit-taking and daily price swings get choppy, the daily math inside a leveraged fund can erode your cash surprisingly fast.

The SK Hynix U.S. listing creates a, dare I say, dramatic situation for holders of DRAM. It is not exactly “why buy the cow if you can get the milk for free,” but more like “why own DRAM when you can just own SKHY?” Not to mention, Micron is easy enough to buy, other than the fact that it takes about $950 to own one full share. That’s half of DRAM right there.

That said, investors have a psychological attraction to what has worked for them. So my suspicion is that DRAM’s asset base is not likely to flow out so quickly, simply because SKHY now exists. (QQQ) and (SPY) holders can similarly own 5-10 stocks and get a similar vibe to those market-trackers, and they still pile in.

At the end of the day, then, DRAM’s recent post-earnings stumble is a clear reminder that the memory space remains a highly volatile arena where yesterday’s winners can cool off in a hurry. SK Hynix’s U.S. listing only complicates that.

Rob Isbitts is a semi-retired CIO, former fiduciary investment advisor, and Barchart columnist. Check out his other work at ETFYourself.com (featuring the Fresh Charts weekly trading post), and ROAR.PiTrade.com, helping investors to better-manage their own portfolios.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)