/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

Super Micro Computer (SMCI) stock has been an underperformer among technology names with negative returns of 42.6% in the last 52-weeks. Even with AI-driven demand coupled with robust top-line growth, SMCI stock has failed to impress.

However, with manufacturing expansion and “Data Center Building Block Solutions” being a growth driver, a potential stock reversal seems to be brewing. In April 2026, SMCI established its largest and fourth Silicon Valley campus. Further, the company is also expanding its manufacturing footprint in Taiwan and the Middle-East.

The capacity expansion provides SMCI with top-line growth potential and scale-driven cost-efficiency. In another positive news, Super Micro announced a collaboration with Everpure (P) and IBM's (IBM) Red Hat to launch Kubernetes Edge AI appliances. This partnership can potentially support business growth for SMCI as cloud-native enterprises are likely to find this package attractive.

About Super Micro Computer Stock

Headquartered in San Jose, Super Micro Computer is a developer and seller of servers, storage systems, modular blade servers, workstations, full-rack scale solutions, networking devices, server sub-systems, and server management. The company’s addressable market includes enterprise data centers, cloud service providers, and edge computing applications, such as 5G Telco, Retail and embedded.

Super Micro has global presence and for fiscal year which ended June 30, 2025, the company sold to over 1,000 customers in over 100 countries. Further, as of FY25, sales to customers outside the United States was 40.6% of the total revenue.

For the first nine months of FY26, SMCI reported revenue of $27.9 billion, which was higher by 72.2% year-over-year (YOY). For the same period, the company’s adjusted EBITDA was $1.8 billion.

While the company’s top-line growth has been robust, EBITDA margin has compressed by 170 basis points in the first nine months of FY26. Therefore, it's not surprising to see SMCI stock declining marginally by 6.41% in the last six months.

DCBBS to Boost Growth and Profitability

SMCI is positioning itself as an end-to-end provider of Data Center Building Block Solutions. The DCBBS components include rack, in-rack CDU, chilled door, battery back-up, cooling tower, among others. At the same time, SMCI is providing software and deployment services.

According to Charles Liang, Founder, Chairman, President & CEO, DCBBS will help the company “gain market share in large, medium and small AI infrastructure deployments.” Further, the segment profit contribution is expected to grow to “double digits” by the end of calendar year 2026.

As DCBBS revenue swells, it’s likely to support margin expansion. With DCBBS significantly reducing the data center build time, the demand is likely to remain strong well beyond 2026.

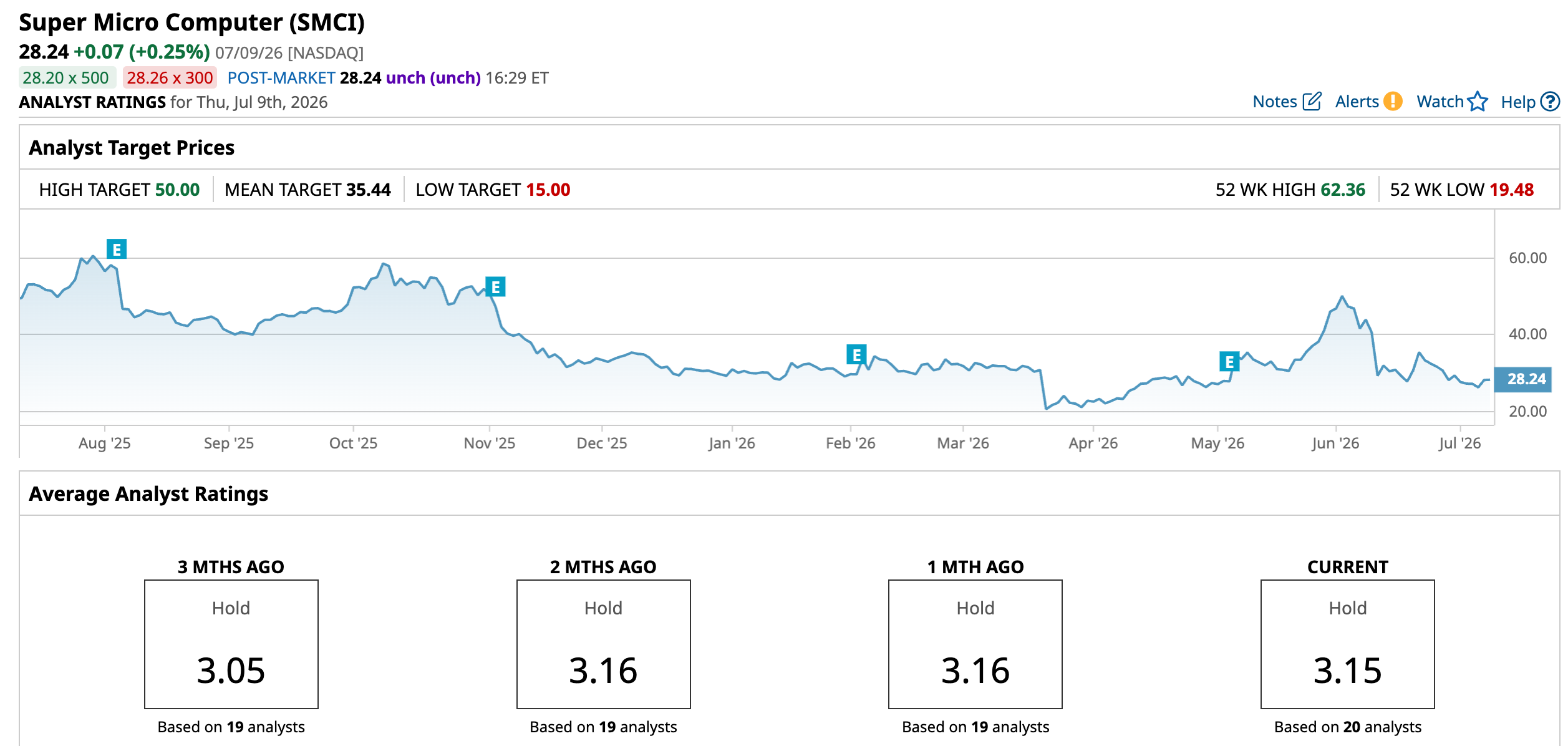

What Do Analysts Say About SMCI Stock?

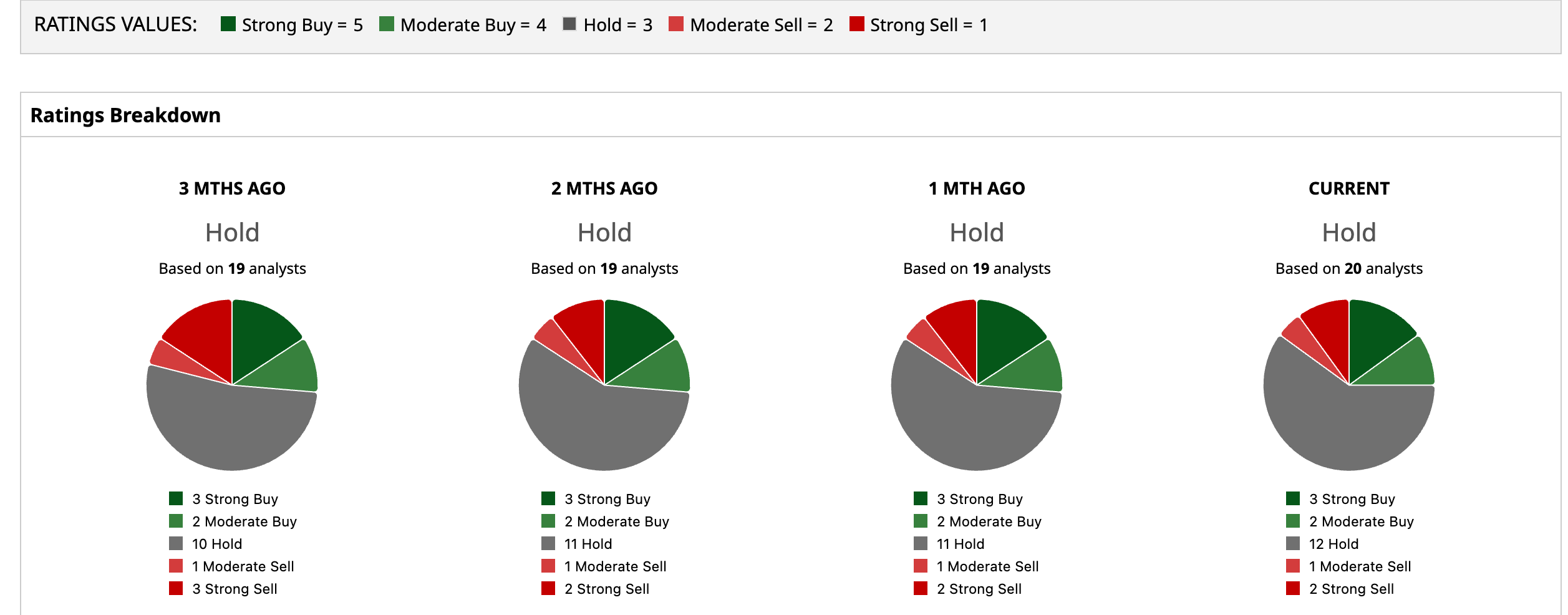

Based on 20 analysts with coverage, SMCI stock has a consensus “Hold” rating. While three analysts have a “Strong Buy” rating for the stock, two have a “Moderate Buy,” 12 have a “Hold,” one has a “Moderate Sell,” and two analysts have a “Strong Sell” rating.

The mean price target of $35.44 represents an upside potential of 25.5% from current levels. Further, the most bullish price target of $50 suggests that SMCI stock could climb as much as 77.1% from here.

Concluding Views

From a valuation perspective, SMCI stock trades at a forward price-to-earnings ratio of 9.44 times. Considering earnings growth estimates of 23.84% and 30.52% for FY26 and FY27, respectively, the stock seems attractively valued.

Notably, SMCI has proposed to raise $7 billion in June 2026 to fund AI orders. The fund raising includes a $1.25 billion offering of common stock, $3.75 billion of depositary shares, and up to $2 billion in at-the-market offering. The fund raise is likely to support growth acceleration and offset the impact of equity dilution.

In June 2026, GF Securities upgraded the stock to “Buy” with a price target of $48 after discounting the dilution factor. GF Securities believes that SpaceX (SPCX) into neocloud space is likely to be beneficial for Super Micro. Overall, SMCI stock is worth considering after a meaningful correction in the last 52-weeks.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)