The Invesco S&P 500 Quality ETF (SPHQ), an ETF devoted to screening for high-quality stocks, is wilting under the pressure of an AI buildup that is now being challenged by gravity.

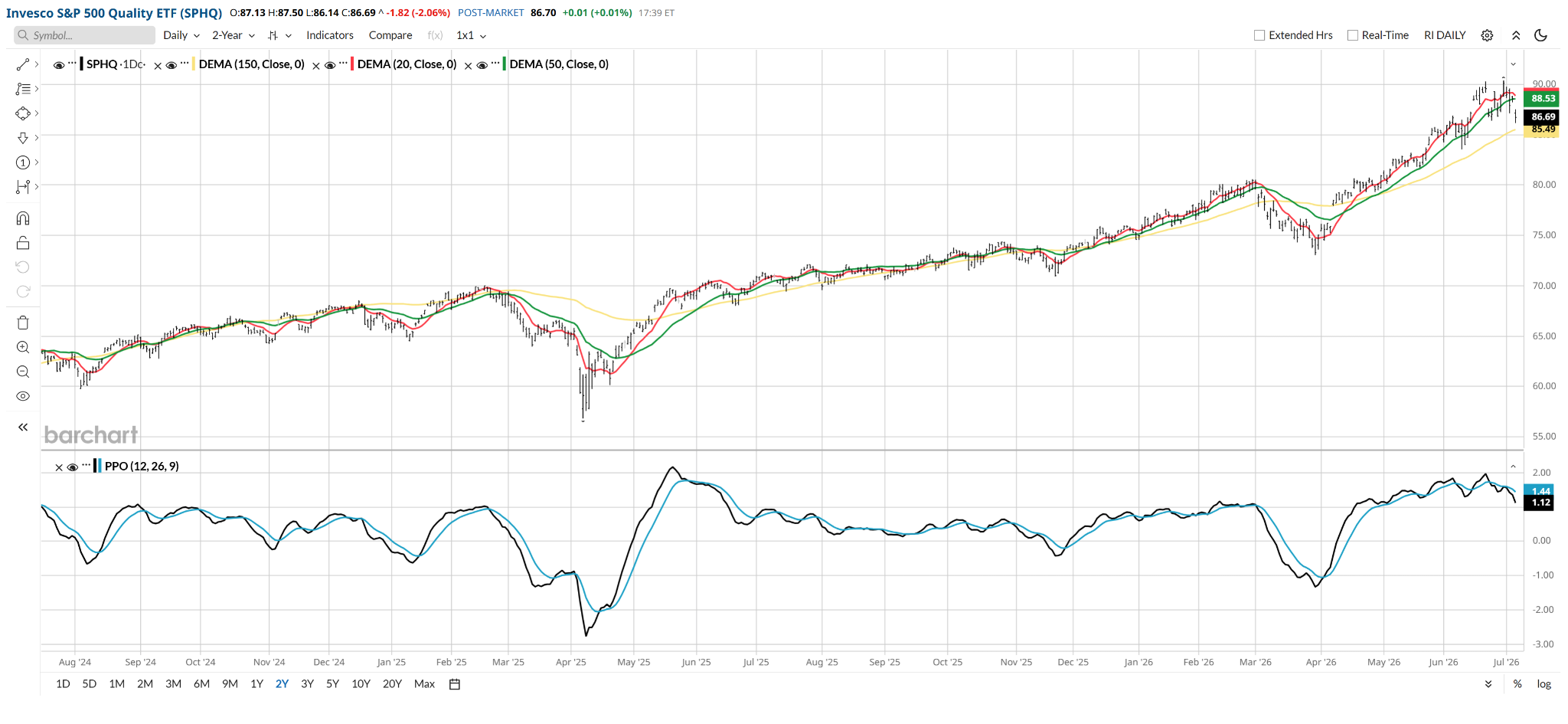

Here’s the daily chart. The percentage price oscillator (PPO) and 20-day moving average are what I’d call “setting up to fail.” That never means “will fail,” but it does prompt a yellow flag.

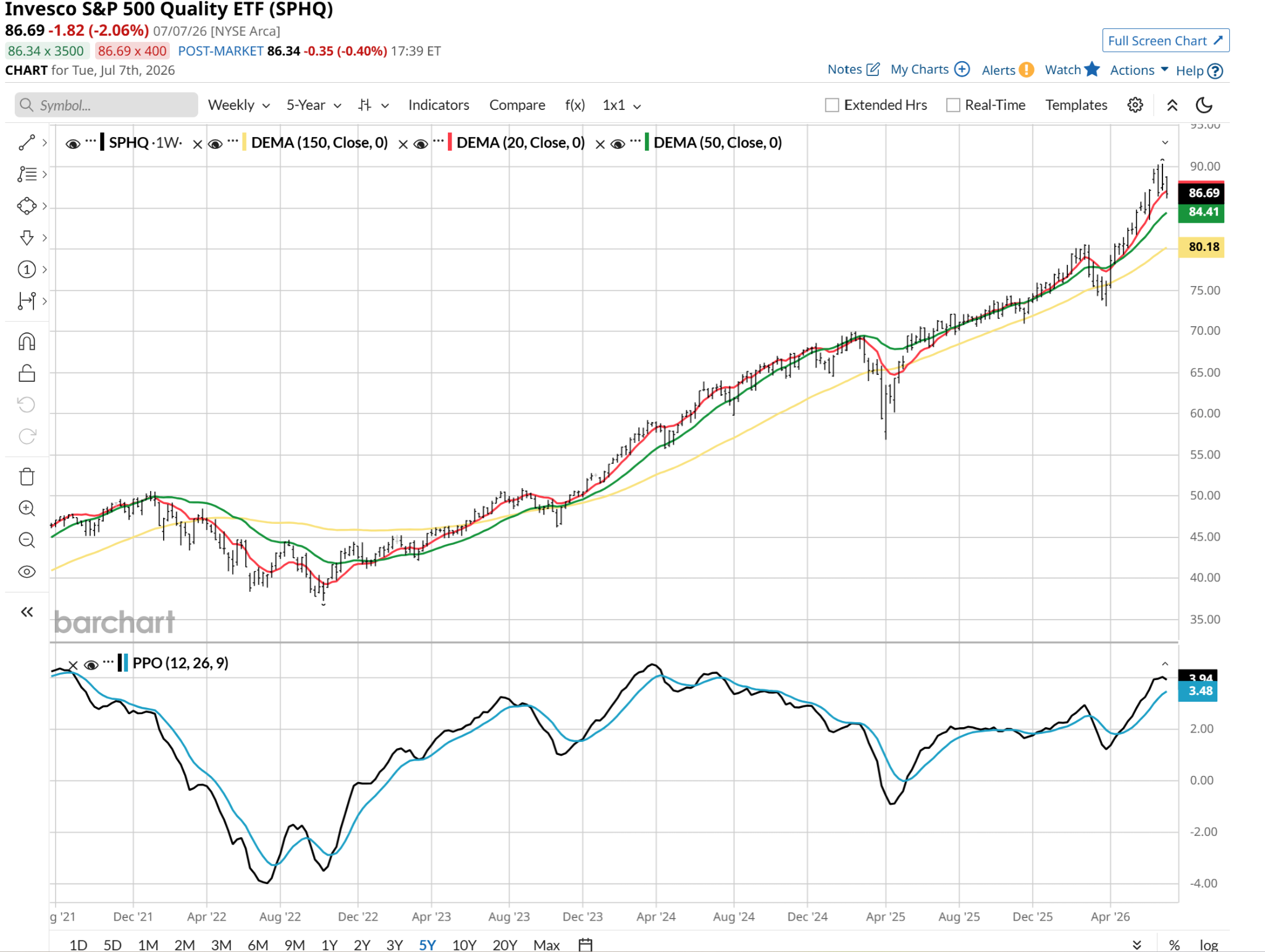

The weekly chart view is similar, just earlier in the price cycle. I could argue it is still in an uptrend. The PPO is elevated, but flattened at the top. This is a slower-moving pattern than a daily chart is.

Why is quality, and SPHQ ETF as a result, potentially in trouble here?

There is so much capital concentrated in a handful of AI’s biggest names, it has left the broader equity market intensely top-heavy. As mega-cap technology firms command sky-high, multitrillion dollar valuations, we traders and investors are forced to question everything.

That includes whether classic fundamental analysis has been permanently rendered obsolete.

In a speculative environment driven entirely by next-gen chip demand and capital expenditure hype, the traditional concept of “quality” investing has taken a back seat to raw momentum. And I don’t think that will change until the rest of the cycle plays out. For that to occur, we’ll need much lower stock prices. Even for companies that meet SPHQ’s quality criteria.

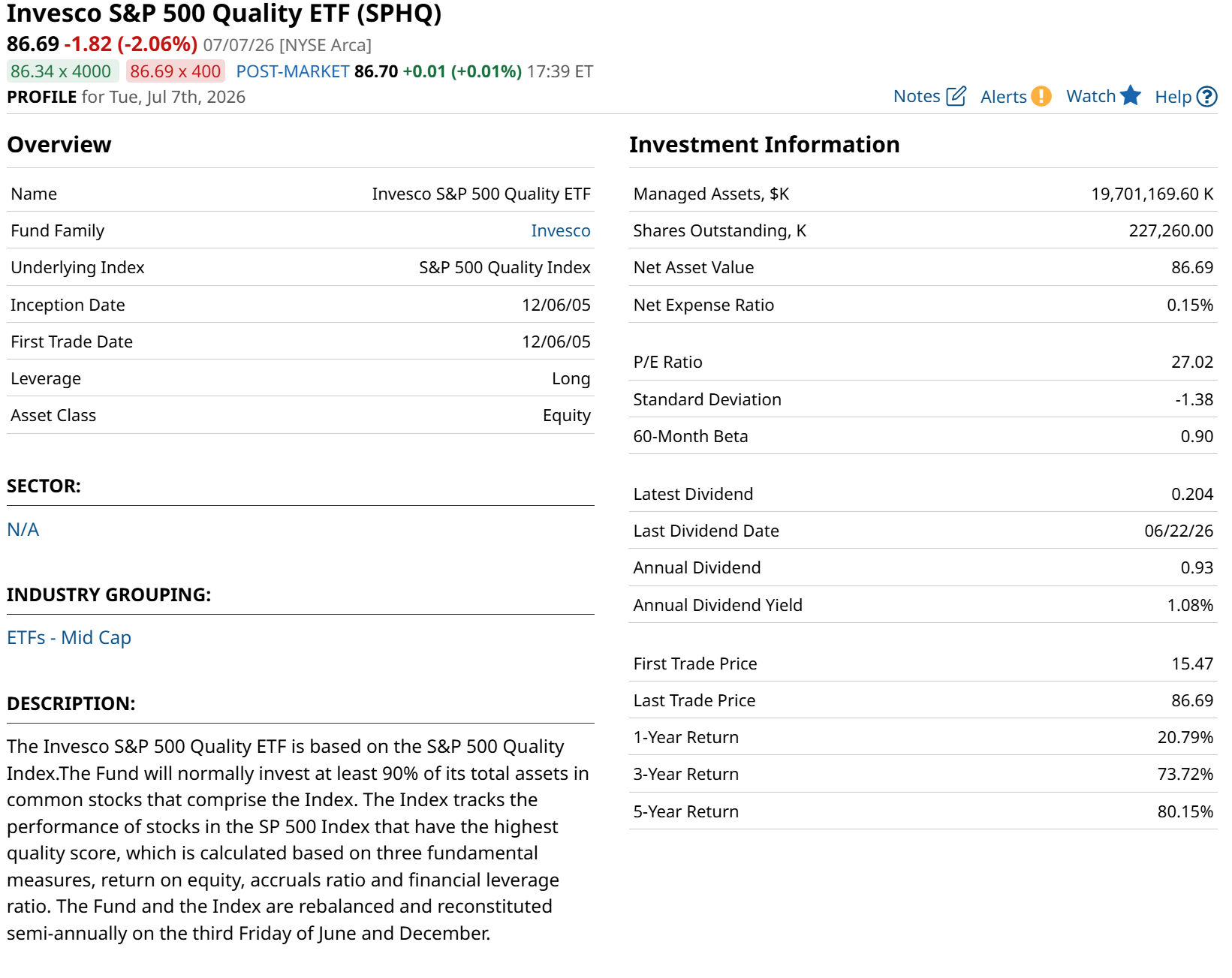

SPHQ screens the S&P 500 Index ($SPX) through a rigid, data-driven methodology, filtering for corporations that display the highest aggregate quality scores based on three distinct fundamental metrics: high return on equity, low balance-sheet financial leverage, and a low accruals ratio to ensure high-quality, cash-backed earnings conversion.

SPHQ is a nearly $20 billion ETF that is more than 20 years old. The portfolio trades at 27x trailing 12-month earnings, which means shareholders are paying way up for quality. Probably too much. That 80% 5-year return is modestly ahead of the SPDR S&P 500 ETF Trust (SPY), which makes sense given how growth-tilted the stock market has been over that time.

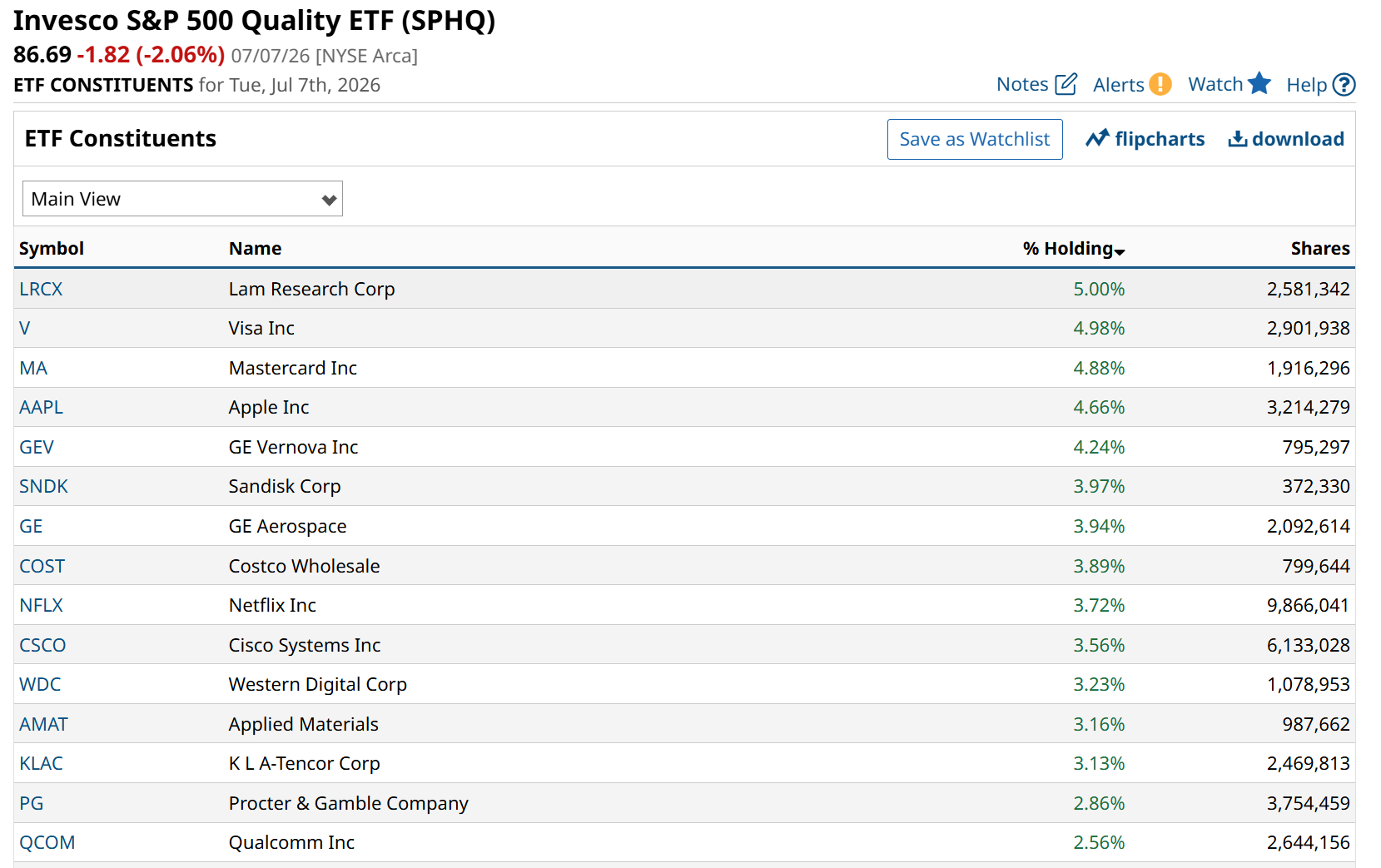

This is where the proverbial rubber meets the road. While SPHQ is a basket of solid businesses, and is more evenly distributed at the top weighting-wise, there’s a problem. The portfolio is more than 40% allocated to technology stocks, and another 18% to industrials. Those are two sectors that have become historically pricey.

SPHQ manages a portfolio of roughly 100 stocks, capping exposure to prevent single-stock distortions as we see in major indexes like SPY and the Invesco QQQ ETF (QQQ). The core question hanging over this strategy is whether these high-quality balance sheets actually offer an effective shield when an overextended tech sector begins to destabilize.

Historically, high return-on-equity and low-debt stocks have provided a built-in buffer during a correction. But this is not a normal market. There is an innate vulnerability that the consensus frequently overlooks.

Because SPHQ relies heavily on robust historical fundamentals, its algorithmic screening process naturally rotates into the tech sectors that have generated the most massive free cash flows over the trailing 12 months. As a result, the fund is at risk of owning yesterday’s momentum winners. That works quite well… until it doesn’t.

This deep tech exposure means that if a broad, systemic re-rating of the AI trade gets underway, a quality-screened portfolio will not be as immune to the gravity of the tape. Compounding that is my strong belief that many investors are not expecting that, nor are they prepared if and when it occurs. Quality is a friendly word, and promotes confidence. But SPHQ has a half-dozen declines of 20% on its long resume, including a 57% dent during the 2007-2009 global financial crisis. Never say never.

While SPHQ explicitly avoids highly leveraged, unprofitable software names, its reliance on premier tech mega-caps and high-multiple semiconductor equipment manufacturers means it remains bound to the broader tech ecosystem’s highs and lows. It is my judgement that in the past few years, even the most pristine balance sheets have seen their valuations pulled forward by passive index inflows.

Bottom line: Be careful of labels thrown around in an attempt to imply protection from major loss. Quality is one such word. Quality is a characteristic, not a defense by itself.

Rob Isbitts is a semi-retired CIO, former fiduciary investment advisor, and Barchart columnist. Check out his other work at ETFYourself.com (featuring the Fresh Charts weekly trading post), and ROAR.PiTrade.com, helping investors to better-manage their own portfolios.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)