/AI%20(artificial%20intelligence)/3D%20Graphics%20Concept%20Big%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Can investors really defend the massive capital expenditure of technology heavyweights? Or will the AI trade collapse as the market senses the return on investment (ROI) will be lighter in impact and take longer to arrive?

The core argument presented is that while the market currently hates the massive, multibillion-dollar spending cycle on artificial intelligence infrastructure, investors will absolutely love it a year or two from now when the automated returns start hitting the ledger.

That narrative harkens back to the early buildout of Amazon Web Services (AWS), reminding everyone that public markets initially penalized heavy cloud infrastructure investments before aggressively rewarding the realized cash flows later.

However, looking strictly at the data from a capital preservation perspective reveals a massive, structural headwind that bulls could very well be glossing over. Specifically, a permanent, multi-year dilution in corporate profitability margins from the stocks that essentially rule the roost within the S&P 500 ($SPX) and Nasdaq-100 ($IUXX) indexes.

They take up so much room at the top, if the market rethinks their outlook, it is akin to turning tail on the AI-led bull market.

The fans of the massive AI spend are accurately describing what even an everyday market skeptic like me can see is fundamental economic regime change. AI is the single largest transfer of corporate investment dollars we’ve ever seen, in the technology industry or otherwise.

But let’s look at where those dollars are actually moving:

Traditional software and internet businesses, tracked by ETFs like the iShares Expanded Tech-Software Sector ETF (IGV) and the SPDR S&P Software & Services ETF (XSW), historically operate at an exceptional 90% incremental margin baseline level. However, capital is now being aggressively diverted away from those high-margin arenas and forced into physical AI infrastructure, which operates at a significantly lower 50% incremental margin baseline. This means a remarkable 40% profit market gap is being extracted directly out of highly efficient software companies and handed over to capital-intensive hardware and data center builders.

While a firm like Amazon (AMZN) can consistently generate a 29% cash return on capital right now by borrowing at mid-single-digit percentage rates, the broader market’s earnings power is gravitating to a less profitable, hyper-competitive infrastructure layer. In other words, we’ve moved on from a tide that lifts all boats to a sharper distinction between winners and losers.

Frankly, I’ve been citing seeing it in the charts I pour through every day. That’s why I love technicals, and using Barchart.com to get an edge. As I say, the market tells us a story, we just have to listen!

Battle for the bytes

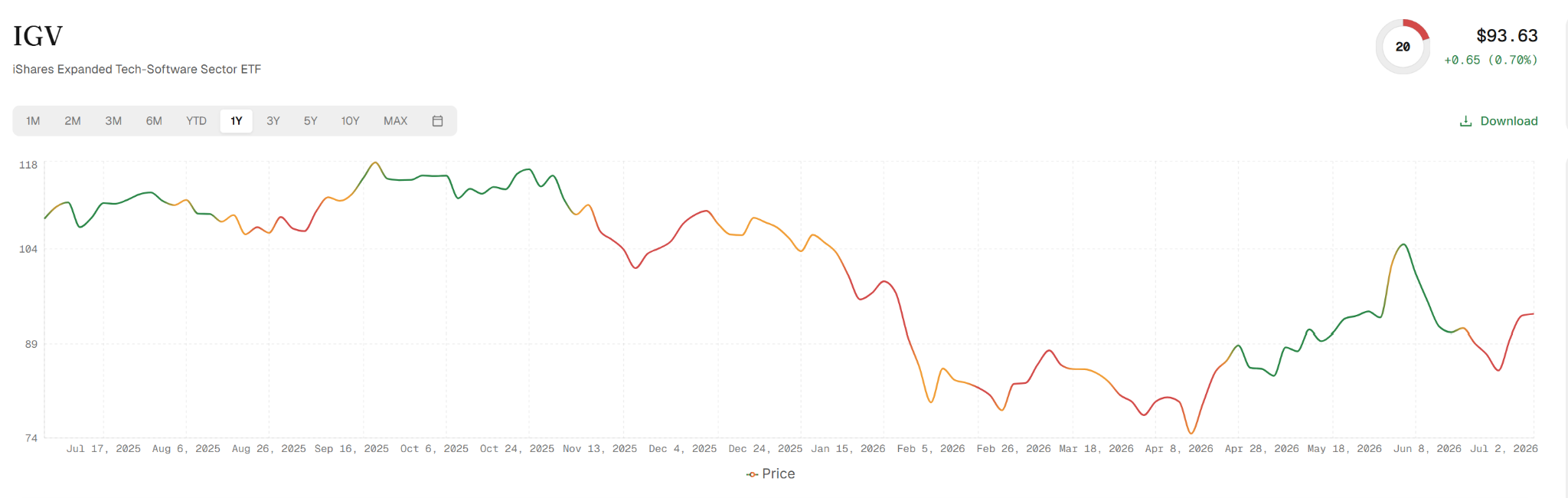

If it’s a comeback candidate you’re looking for, the first place to hunt is IGV. This is one of the interesting charts I see right now, in that it can go either way in the intermediate term. A $95 ETF price, paired with the trading range assumptions I’ve made here of $108 and $77, would point to a standoff. No clear signal yet.

However, what I see above is that we also have a much shorter-term range and an attempt by IGV to create a short-term bottom. It is not what I’d call a strong signal, and it has already bounced 10% from its most recent dive, the latest in a series of plunges since last October’s top, about 25% north of here ($118). The bottom line for me with IGV is that it is a higher-risk trade, but a decent setup nonetheless.

My ROAR Score analysis confirms that. A score of 20 implies much higher than average risk. But given that ROAR’s main function is to select securities within a portfolio or watchlist, a score of 20 will translate to a much more bullish outlook if it starts ticking higher to, say 40. So that’s what I’ll be watching for here.

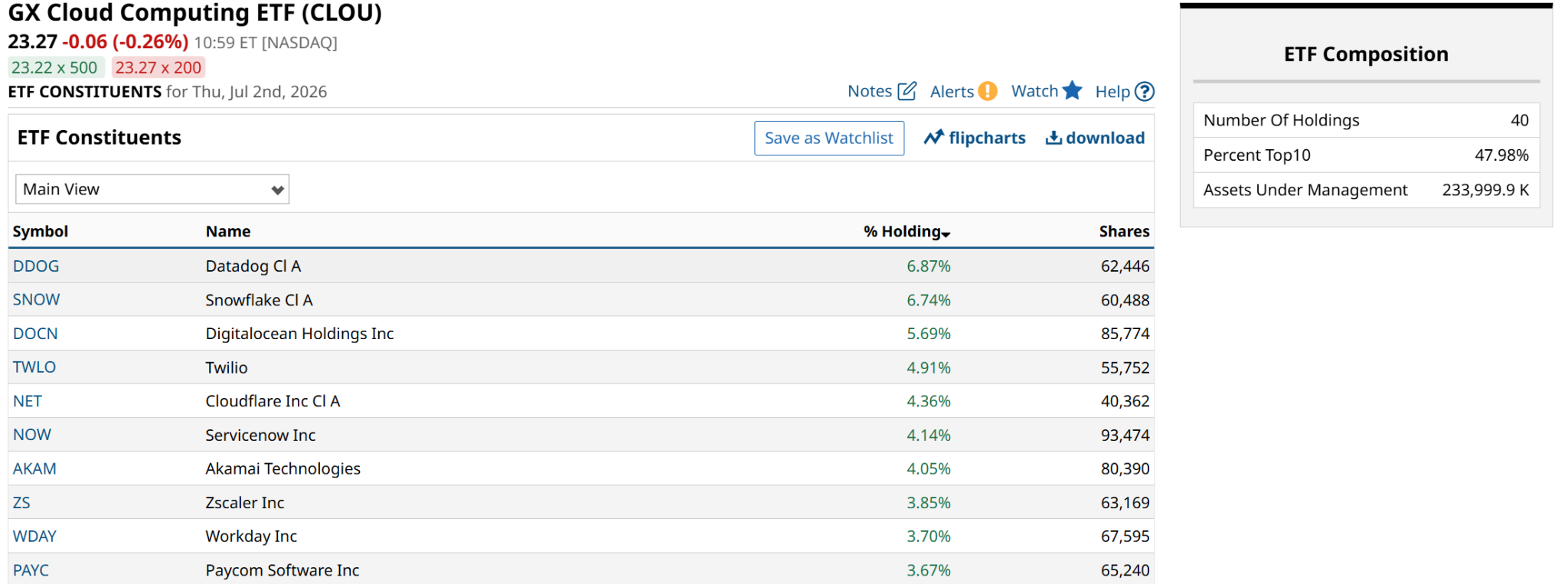

Another one I’m watching in this regard is the Global X Cloud Computing ETF (CLOU). Its top 10 holdings make up nearly half of this $230 million-plus ETF. And the bullish thesis argues that cloud stocks are the ultimate beneficiaries of increased data workloads from the AI-adoption era. The argument is that efficiency improvements and open-source models will drive down query costs, sparking an explosion in data consumption.

Then, there’s the other side of this situation. The memory stocks that have launched like a SpaceX (SPCX) rocket. But are now showing clear signs of exhaustion, or worse. The Roundhill Memory ETF (DRAM) has only been listed for three months, but that’s enough time for me to look bearishly here.

I think this is the stock market’s latest chapter in a long-running series of “haves and have nots.” But don’t be surprised if the recent winners and losers swap sides soon.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)