/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)

ServiceNow (NOW) has endured a difficult first half of the year, with its stock declining about 31% year-to-date (YTD) and falling nearly 50% from its 52-week high.

Much of the decline reflects a broader shift in investor sentiment toward enterprise software companies. As artificial intelligence (AI) rapidly reshapes the software industry, investors have become increasingly concerned that AI-powered agents could eventually disrupt traditional software vendors. Those fears have fueled widespread selling across the sector, with ServiceNow among the hardest hit.

The pressure intensified following the company's first-quarter earnings report. On the surface, the results were strong, with healthy revenue growth and solid operating execution. However, investors focused on management's comments that subscription deals in the Middle East were being delayed amid geopolitical uncertainty.

Adding to those concerns, the company's acquisition of Armis is expected to pressure margins in the near term, weighing on profitability.

ServiceNow’s Business Continues to Perform

While both issues sparked a negative market reaction, they appear to be temporary headwinds. In fact, the bigger picture remains encouraging. ServiceNow's subscription business continues to deliver healthy growth, supported by strong enterprise demand. More importantly, there is little evidence that AI is reducing demand for the company's platform. Instead, ServiceNow is embedding AI throughout its workflow software, positioning itself to benefit from the technology.

Even with delayed contract closures in the Middle East, management raised its full-year guidance, signaling confidence that overall customer demand remains robust.

Customer retention also remains one of ServiceNow's greatest competitive strengths. The company maintained an impressive 97% renewal rate. The high renewal rate provides a stable foundation for recurring revenue growth.

Meanwhile, the company's enterprise footprint continues to expand. ServiceNow now serves 630 customers, generating more than $5 million in annual contract value (ACV), while several new large enterprise agreements were signed during the quarter, reflecting customers' willingness to deepen their long-term commitments.

One of the most encouraging trends was the sharp increase in customer spending. Customers with over $1 million in annual spending on the platform surged 130% year-over-year (YoY), reflecting deeper adoption. Meanwhile, Moveworks, which it recently acquired, is already exceeding expectations following its integration into ServiceNow's employee experience business, contributing seven-figure deals and expanding rapidly within existing customer accounts.

Customers are increasingly adopting multiple products across the company's platform, with most of its largest deals now spanning several solutions rather than a single offering. This expanding platform strategy strengthens customer relationships and also increases revenue opportunities over time.

AI Is Becoming a Growth Driver, Not a Threat

Ironically, one of the biggest reasons behind ServiceNow's stock decline could ultimately become one of its strongest growth catalysts.

Rather than being disrupted by AI, the company is embedding AI capabilities throughout its platform. Demand for its AI portfolio continues to accelerate, with the Now Assist suite gaining widespread adoption and remaining on track to become a significant contributor to future revenue.

New products such as AI Control Tower and Raptor DB Pro are also gaining traction among enterprise customers. These solutions are helping ServiceNow secure larger contracts while encouraging broader adoption across its platform.

As enterprises increasingly seek to automate workflows and improve productivity with AI, ServiceNow appears well-positioned to benefit from this trend.

ServiceNow Sees Solid Growth Ahead

ServiceNow sees strong growth ahead. Management provided a solid long-term growth outlook at its recent Financial Analyst Day. ServiceNow expects subscription revenue to exceed $30 billion by 2030, more than doubling from the $12.9 billion generated in 2025. For 2026, ServiceNow has guided to approximately $15.8 billion in subscription revenue at the midpoint of its outlook.

Achieving its 2030 target would require the company to sustain robust double-digit growth for several years, suggesting management remains confident in both customer demand and its competitive positioning despite rapid advances in AI.

NOW Stock Is a Buy

While concerns about AI disruption, temporary delay in the closure of large deals, and acquisition-related margin pressure have driven the stock sharply lower, the company's long-term growth trajectory remains intact, providing an attractive buying opportunity.

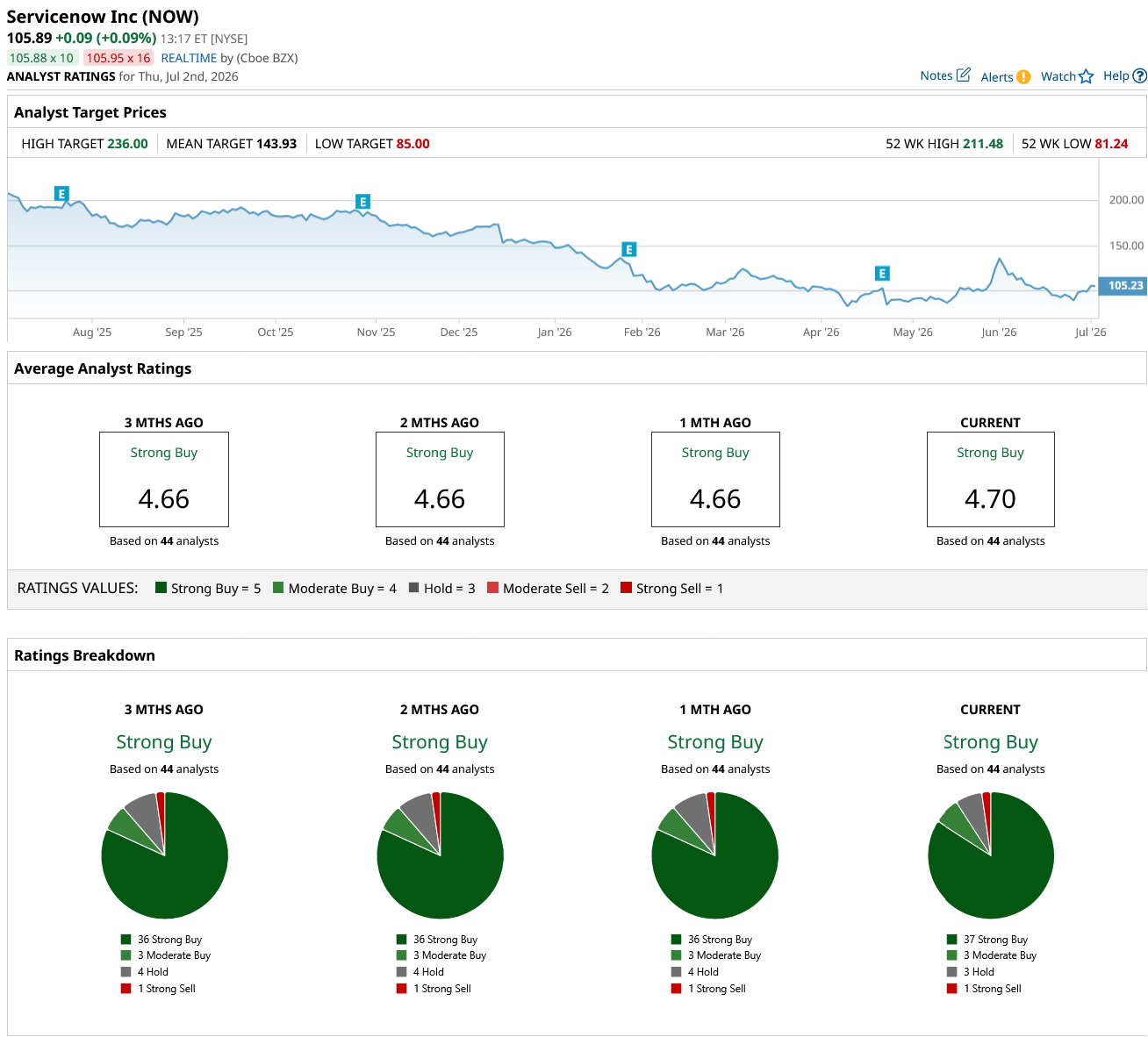

Analysts are also bullish about NOW stock and maintain a “Strong Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)