/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

SanDisk Corporation (SNDK) is a pure-play NAND flash memory and data storage company spun out of Western Digital (WDC) in February 2025 and headquartered in Milpitas, California. The company develops, manufactures, and sells a broad portfolio of storage solutions, including enterprise solid-state drives, embedded flash products, removable memory cards, and USB drives, serving data centers, cloud service providers, PC manufacturers, and consumer electronics makers.

As artificial intelligence infrastructure buildout accelerates globally, SanDisk's enterprise SSD and high-density NAND products have emerged as mission-critical components in hyperscaler data centers, positioning the company at the heart of one of the most powerful secular growth trends in the semiconductor industry.

SanDisk Stock Outperforms

SNDK shares were trading around $2,023 in early July 2026, having surged from a 52-week low of $40.10 to an all-time high of $2,354.39, representing one of the most extraordinary price appreciation stories in recent market history. The stock priced its spinoff from Western Digital at approximately $38.50 per share in February 2025, delivering a return of roughly 4,000% in approximately 16 months.

Compared to the S&P 500 Information Technology Index ($SRIT), which has posted strong but comparatively modest gains in 2026 on the back of broad AI-driven semiconductor enthusiasm, SNDK has been among the top gainers in the S&P 500 Index ($SPX) and Nasdaq 100 Index ($IUXX), alongside peers Western Digital and Seagate Technologies Holdings (STX), with shares soaring 622% year-to-date (YTD), dramatically outpacing its sector benchmark.

SanDisk Revises Strong Outlook

SanDisk's fiscal Q3 2026 results, reported on April 30, delivered revenue of $5.95 billion, up 97% sequentially and 251% year-over-year (YOY), well above the company's own guidance range and the consensus analyst forecast of $4.7 billion. Adjusted EPS came in at $23.41, crushing the analyst estimate of $14.36 by 63%, compared to a loss of $0.30 in the same quarter last year. The blowout quarter underscored the sheer scale of AI-driven demand reshaping the enterprise storage landscape.

SanDisk reported a non-GAAP gross margin of 78.4% and an operating margin of 70.9% for the quarter, with the data center segment surging 233% sequentially as AI infrastructure spending accelerated. The company generated nearly $3 billion in free cash flow in a single quarter, while retiring all long-term debt and authorizing a $6 billion share repurchase program. SanDisk has also secured approximately $42 billion in multi-year AI supply contracts, providing exceptional forward revenue visibility.

Looking ahead, management issued guidance that reset Wall Street expectations entirely. For Q4 FY2026, SanDisk guided revenue of $7.75 billion to $8.25 billion and adjusted EPS of $30 to $33 per share, significantly above the prior consensus of $6.49 billion in revenue, reflecting continued AI data center demand strength.

CEO David Goeckeler highlighted that enterprise SSD revenue grew sevenfold YOY, with the company's high-bandwidth flash technology targeting DRAM-like performance at a fraction of the cost, with product launches expected in late 2026 and 2027, reinforcing SanDisk's ambition to move further up the AI memory value chain.

SanDisk Price Hiked by BofA

SanDisk shares tumbled 10.62% on Wednesday, July 2, trading despite a bullish price target increase from Bank of America, which raised its target to $2,500 from $2,100 while reiterating its “Buy” rating, signaling an upside potential of 41.8% from current levels.

BofA analyst Wamsi Mohan cited a persistent supply-demand imbalance in the NAND market as the key structural tailwind, expecting strong pricing conditions to extend through mid-2027, albeit with moderating quarter-over-quarter growth rates. For the June quarter, Mohan modeled bit growth of 13% sequentially and ASP growth of 35% sequentially, noting that SanDisk's realized price increases will ultimately depend on product mix and the volume of new business model contracts signed in the period.

The sell-off appears to reflect broader profit-taking across AI memory stocks rather than any fundamental deterioration in SanDisk's outlook, which remains firmly underpinned by long-term AI infrastructure demand.

Is SNDK Still a Buy After the Sell-Off?

Despite Wednesday's sharp sell-off, Bank of America's upgraded $2,500 price target reinforces the structural bull case for SanDisk, with NAND supply-demand dynamics expected to remain favorable well into 2027.

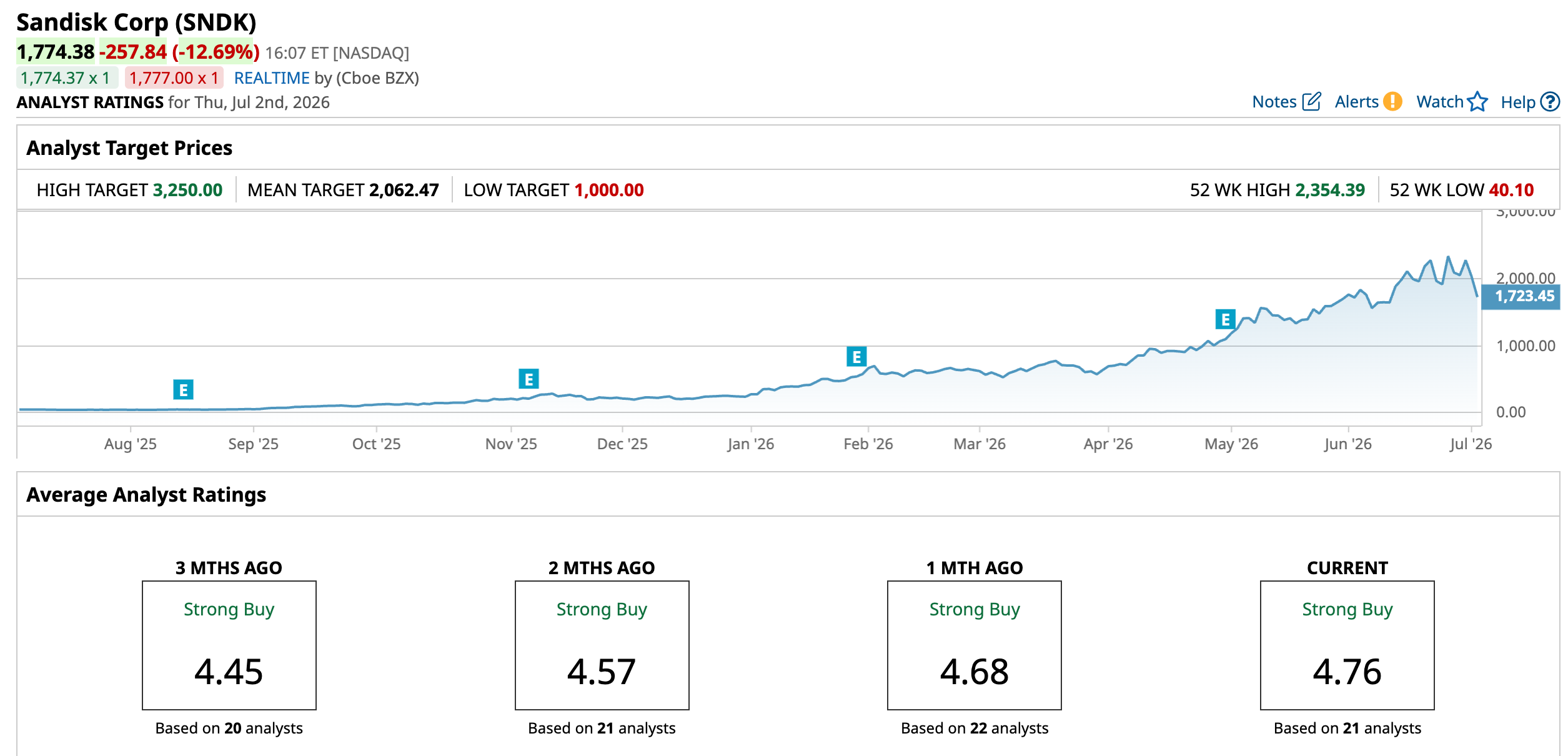

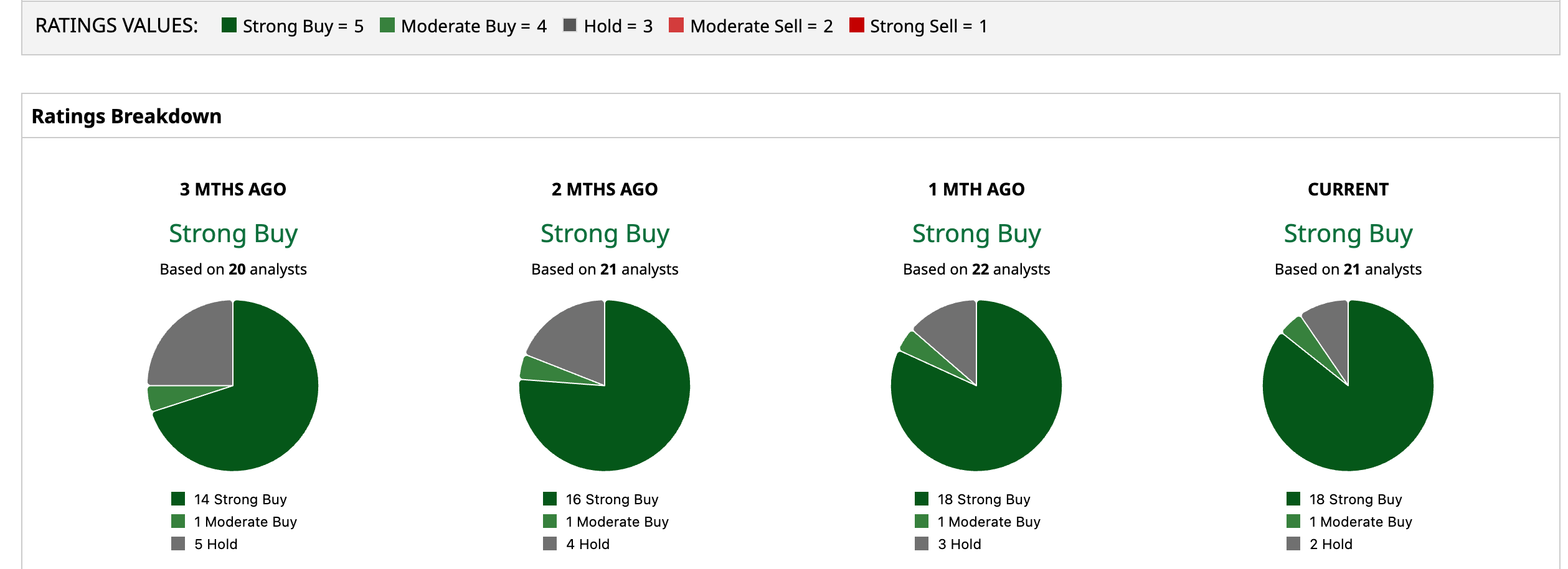

The broader analyst community is firmly in agreement with a consensus "Strong Buy" rating across 21 analyst ratings, including 18 “Strong Buy,” one “Moderate Buy,” and just two "Hold" recommendations. The mean price target of $2,062.47 shows potential of a 16.24% climb from here. And, the Street-high price target of $3,250 indicates a run of up to 83.16% over the next 12 months.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)