/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)

Artificial intelligence (AI) is driving one of the largest infrastructure investment cycles the tech industry has ever seen. Goldman Sachs believes this massive “capex supercycle” will force AI-related capital expenditures to surge to $757 billion in 2026, up 84% year-over-year (YoY), before climbing to $920 billion in 2027. As Big Tech pours hundreds of billions into chips, servers, networking, and data centers, the investment bank says a few tech stocks stand to capture the biggest share of this spending wave.

Here are the three stocks Goldman believes could be among the biggest winners of AI's next growth phase.

Stock #1: Applied Materials (AMAT): Powering the Factories That Build AI Chips

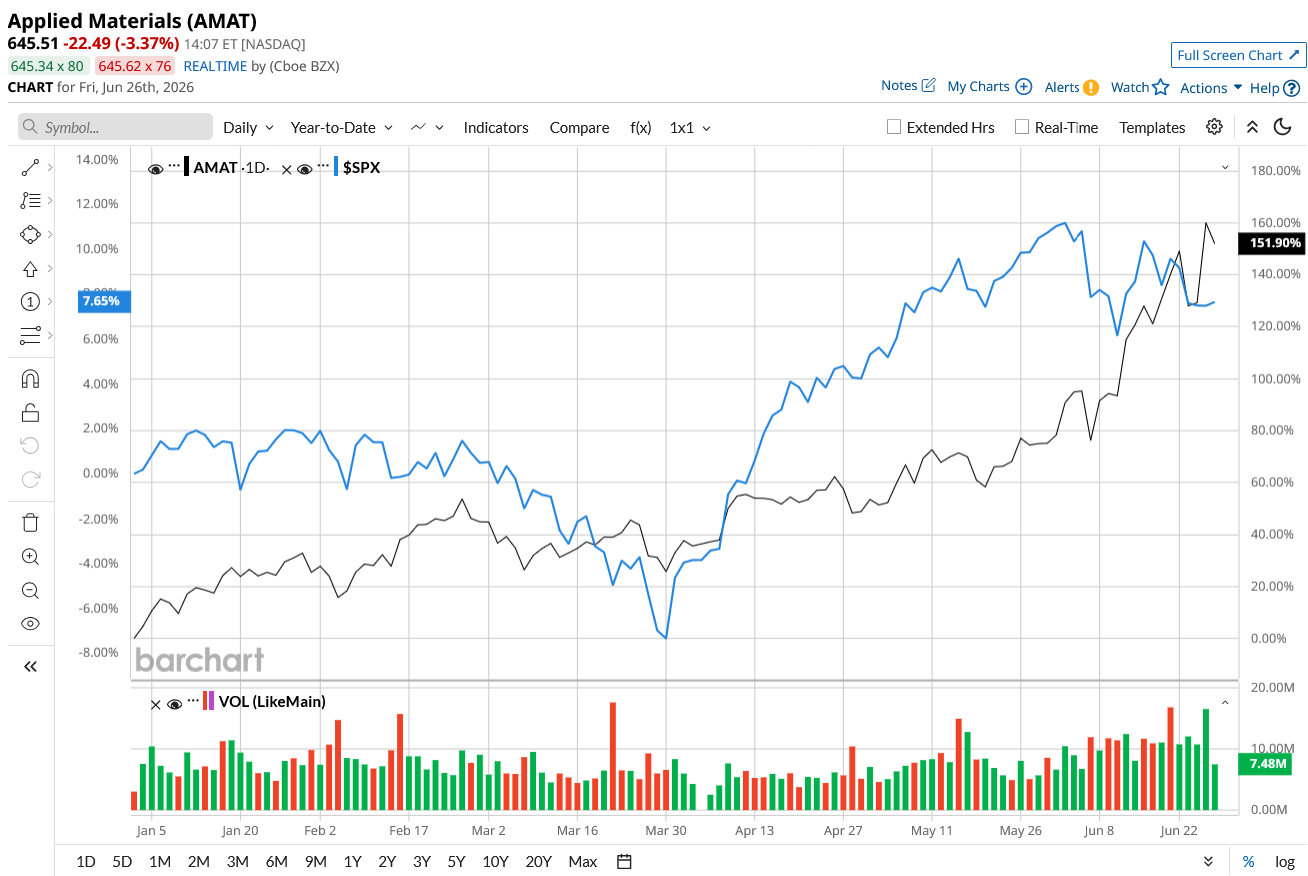

Applied Materials (AMAT) hasn’t been in the headlines, but investors have started to recognize its potential, as AMAT stock has soared 155% so far this year. Every advanced AI processor begins its journey in a semiconductor fabrication plant, where Applied Materials uses its deposition, etching, inspection, and materials engineering tools to work its magic.

In the second quarter of fiscal 2026, Applied Materials reported revenue growth of 11% YoY to $7.91 billion, while adjusted earnings per share climbed 20% to $2.86, supported by expanding margins and strong customer demand. The semiconductor equipment business is now expected to expand over 30% in 2026, driven by rapid AI infrastructure deployment across leading-edge foundries, memory manufacturers, and advanced packaging facilities. The company is also expanding partnerships through its EPIC Center with industry leaders including Taiwan Semiconductor (TSM), Samsung Electronics (SMSN.L.EB), Micron Technology (MU), and SK Hynix to accelerate next-generation semiconductor technologies.

Finally, Applied Materials operates in the areas expected to receive the bulk of AI infrastructure capex spending over the next several years. As AI demand grows, foundries such as TSMC, Samsung, Intel, Micron, and SK Hynix must expand production capacity. Suppliers like Applied Materials are poised to win. This is why it has made it to Goldman Sachs’ list of the biggest winners of AI's next growth phase.

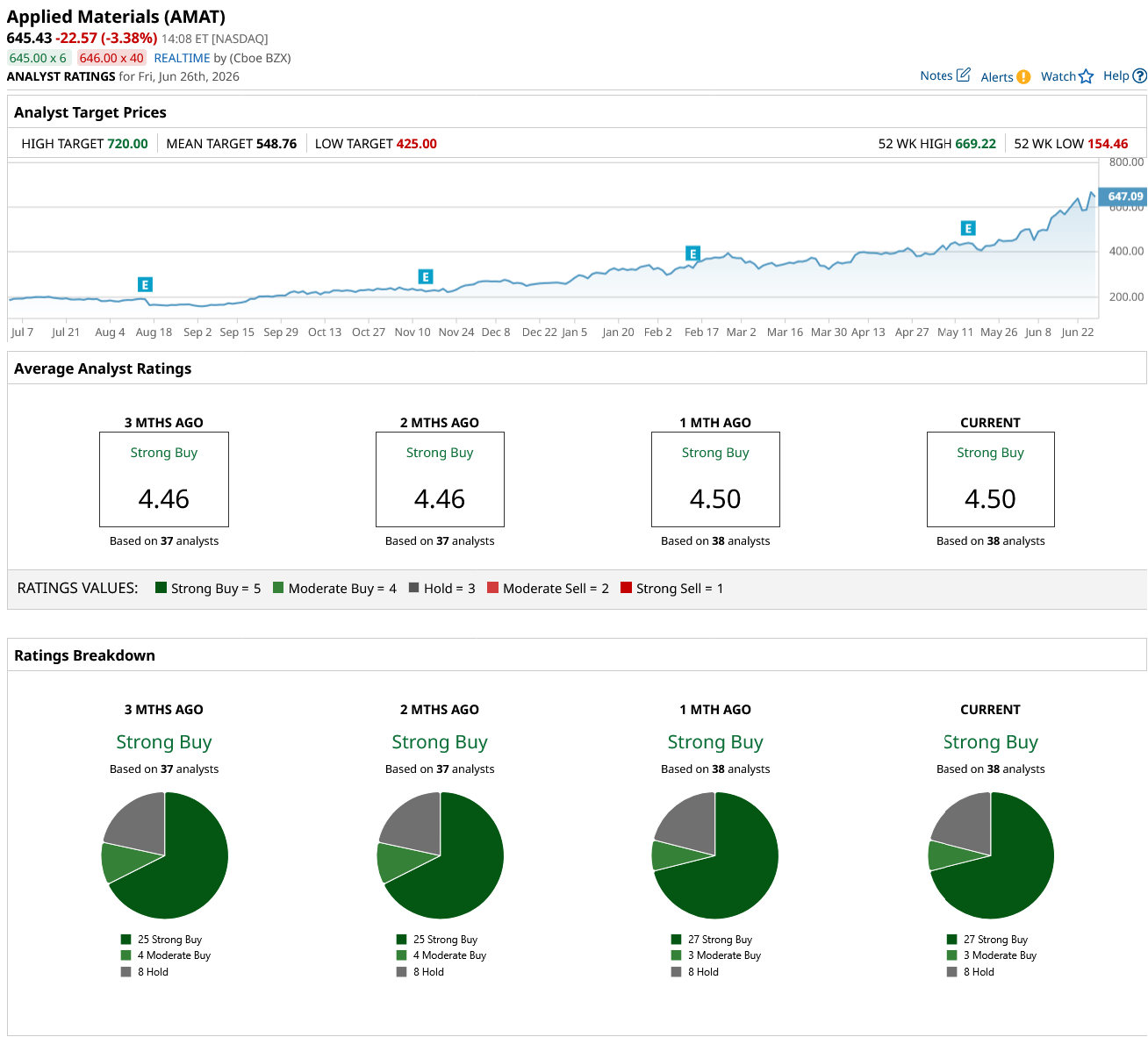

Overall, the stock has a consensus “Strong Buy” rating. Out of 38 analysts with coverage, 27 rate AMAT stock as a “Strong Buy,” three have a "Moderate Buy" rating, and eight analysts offer a "Hold" rating. AMAT stock has crossed its average price target of $548.76, also surpassing the overall market’s gain. However, the high target price of $720 implies a potential upside of 12% over the next 12 months.

Stock #2: Broadcom (AVGO): Riding the AI Networking and Custom Chip Wave

Broadcom (AVGO) designs the custom AI chips and high-speed networking hardware that enable thousands of AI processors to work together inside the world's largest data centers. Despite a strong second quarter with solid AI semiconductor sales and a massive AI backlog, Broadcom seems to have been overlooked. AVGO stock has gained just 8% year-to-date (YTD), just in line with the overall market gain.

Broadcom manufactures and supplies the AI networking chips, which help thousands of GPUs communicate with each other at extremely high speeds. As AI models continue growing, networking has become as important as computing power, making Broadcom a critical supplier. In the second quarter, Broadcom’s AI semiconductor revenue skyrocketed 143% YoY to $10.8 billion, fueled by soaring demand for custom AI chips and high-speed networking solutions used in hyperscale data centers.

Overall, the Semiconductor Solutions segment, which accounted for more than two-thirds of total revenue, increased 79% to $15 billion. Total revenue rose 48% to $22.2 billion. The company even recorded more than $30 billion in AI semiconductor bookings in the quarter. On the software side, the company’s Infrastructure Software segment, fueled by VMware, security, and enterprise management software, grew 9% YoY to $7.2 billion.

Broadcom remains committed to attaining its $100 billion AI semiconductor revenue target by fiscal 2027. While this is an impressive goal, investors anticipated a much higher target, which is why the stock hasn’t received much love so far. However, its diverse AI exposure to two of the fastest-growing parts of AI infrastructure is precisely why Goldman Sachs believes it will profit from the massive hyperscaler spending.

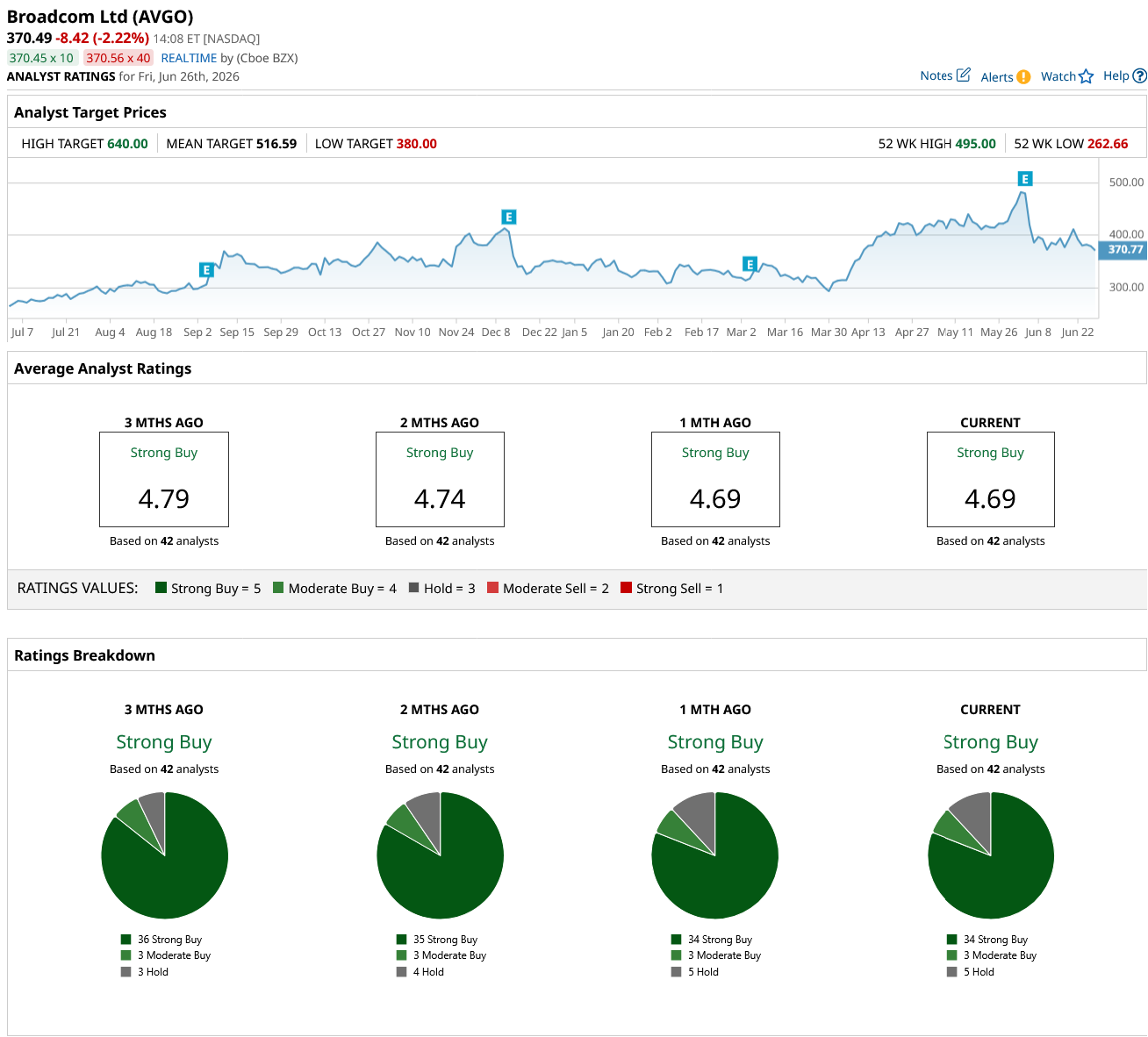

Overall, AVGO stock holds a consensus "Strong Buy" rating on Wall Street. Of the 42 analysts with coverage, 34 analysts have a “Strong Buy,” three have a “Moderate Buy” rating, and five recommend a “Hold.” Based on the average target price of $516.59, the stock has potential upside of 39% from current levels. Plus, the high price target of $630 suggests shares could climb by 70% over the next 12 months.

Stock #3: NXP Semiconductors (NXPI): Bringing AI Beyond the Data Center

NXP Semiconductors (NXPI) designs chips for automobiles, industrial equipment, IoT devices, mobile devices, communications infrastructure, and secure identification systems. Unlike Applied Materials and Broadcom, NXP's business doesn’t focus on AI data centers. Rather, its biggest AI opportunity lies outside traditional cloud infrastructure. In fact, it is in bringing AI into automobiles, factories, industrial equipment, and connected devices. NXP stock has climbed 29% YTD, outperforming the broader market gain of 7.3%.

In the first quarter, NXP’s revenue climbed 12% YoY to $3.18 billion, while adjusted earnings per share increased 16% to $3.05 per share. The automotive sector remains its biggest growth engine, which generated $1.78 billion in revenue, an increase of 6% YoY, fueled by software-defined vehicle programs, electrification, automotive radar, and connectivity solutions. The company highlighted strong design-win momentum for its S32N and S32K5 automotive processors, along with new imaging radar and automotive Ethernet wins. These products are expected to boost its semiconductor content per vehicle over multiple years.

AI also drove growth across its Industrial & IoT business, which surged 24% to $628 million. Furthermore, while edge AI isn’t receiving as much attention as data centers now, it remains a long-term growth opportunity for NXP. The rise of physical AI and robotics is creating significant opportunities for its processing, connectivity, and security products. Its leadership and experience in automotive and industrial chips will benefit it as intelligence gets embedded across billions of connected devices over the next decade.

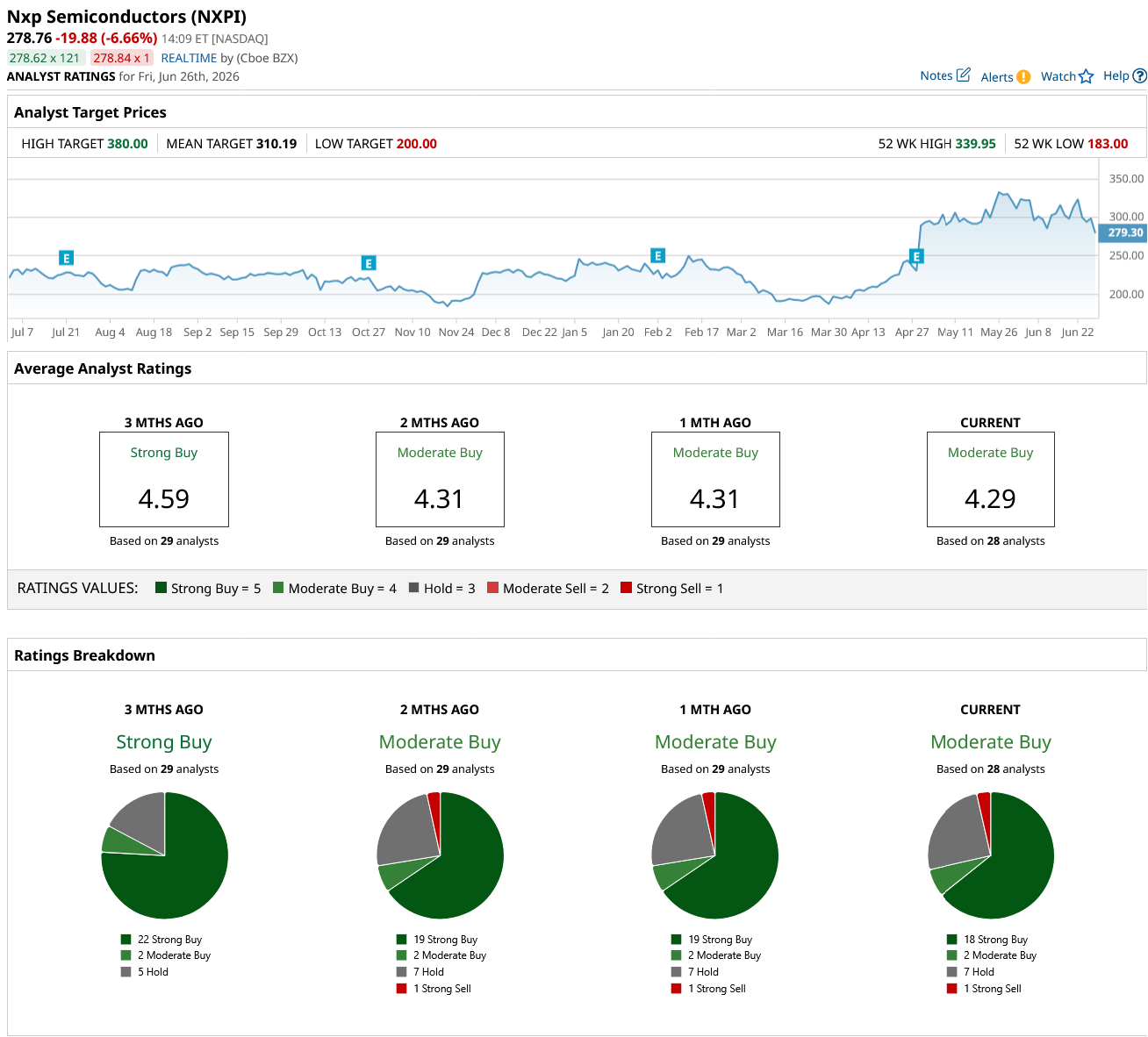

Overall, NXPI stock is a “Moderate Buy” on Wall Street. Of the 28 analysts covering the stock, 18 rate it a “Strong Buy,” two say it is a “Moderate Buy,” seven rate it a “Hold,” and one says it is a “Strong Sell.” The average target price for the stock is $310.19, implying a 12% gain from the current trading price. However, the high price estimate sits at $380, which implies the stock can climb by 37% from current levels.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Delta%20Air%20Lines%2C%20Inc_%20passanger%20plane-by%20viper-zero%20via%20iStock.jpg)