/Delta%20Air%20Lines%2C%20Inc_%20passanger%20plane-by%20viper-zero%20via%20iStock.jpg)

Founded in 1924, Delta Air Lines, Inc. (DAL) has spent more than a century turning the skies into its playground. Today, it ranks among the world's largest airlines, carrying passengers and cargo across a sprawling domestic and international network. Commanding a market cap of nearly $57 billion, the carrier operates a fleet of more than 1,300 aircraft.

Alongside its airline operations, the Atlanta, Georgia-based giant pulls in revenue from aircraft maintenance, repair, and overhaul services for third parties, vacation package offerings, and refinery operations that help support its fuel supply requirements.

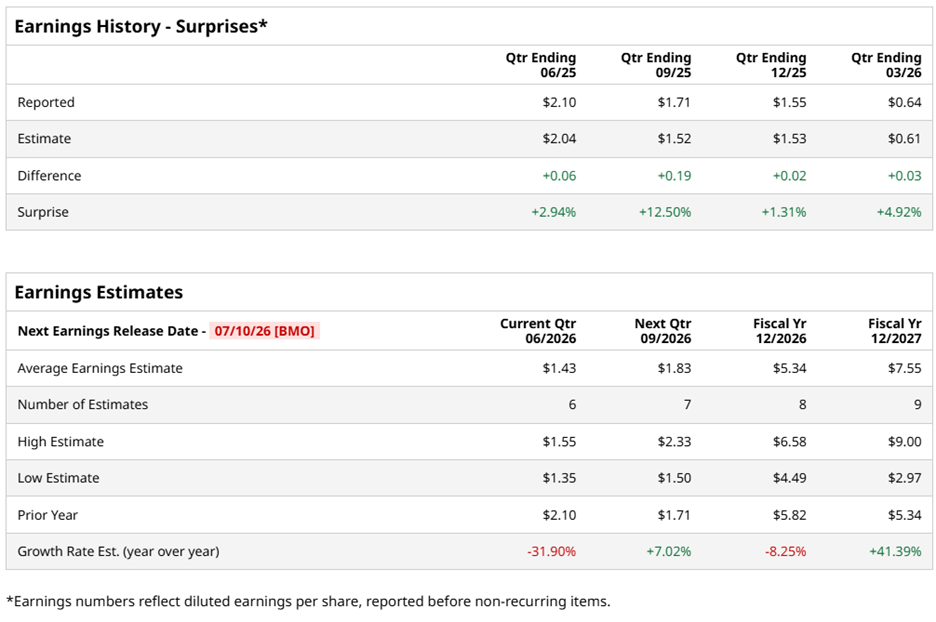

The airline is now approaching its fiscal 2026 second-quarter earnings report, scheduled for Friday, July 10, before the opening bell. Wall Street expects Delta to post diluted EPS of $1.43, representing a 31.9% drop from $2.10 in the same quarter last year. Still, Delta has developed a habit of clearing the bar when it counts. The company topped analysts’ EPS estimates in each of the last four quarters.

Further down the runway, analysts forecast full fiscal 2026 diluted EPS of $5.34, reflecting an 8.3% year-over-year decline. The outlook brightens considerably beyond that point. Full fiscal year 2027 diluted EPS is projected to climb to $7.55, which would mark a 41.4% increase from the prior year.

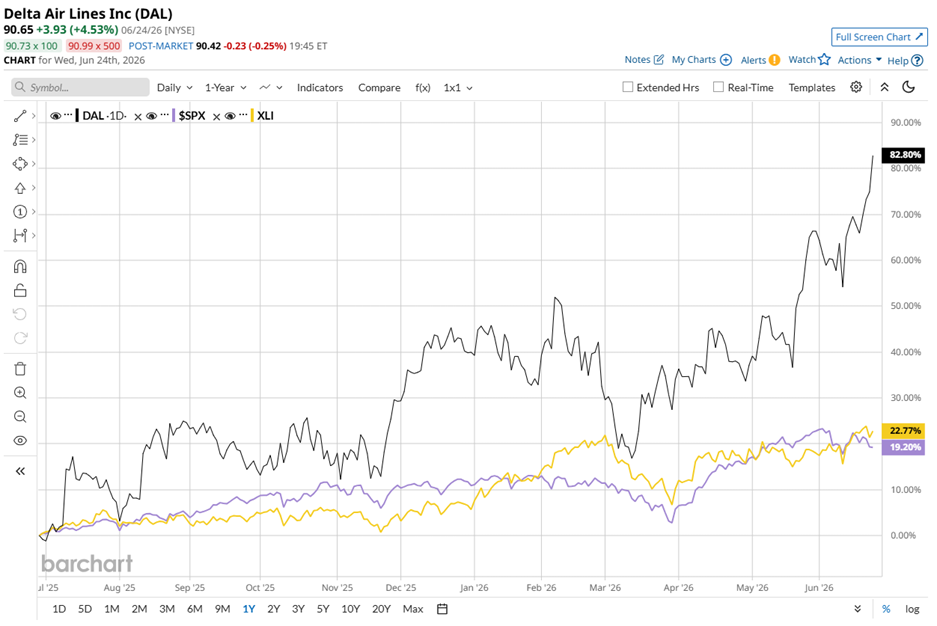

In the last 52 weeks, DAL stock has soared 82.9%, leaving the broader S&P 500 Index ($SPX), which gained 20.8%, far behind. The trend continues in 2026, as Delta Air Lines’ shares have advanced nearly 30.6% year-to-date, while the benchmark index has posted a more modest gain of 7.5%.

The same story plays out against sector peers. The State Street Industrial Select Sector SPDR ETF (XLI) has returned 24.2% over the past 52 weeks and gained 16.2% in 2026. The numbers certainly hold their own, yet they still fall short of Delta’s stronger performance.

Investors received another reason for optimism on Wednesday, June 24. Crude oil prices slipped to their lowest level since before the Iran war, taking some of the heat off concerns surrounding airline fuel costs. The development gave DAL stock a tailwind, pushing shares up about 4.5% during intraday trading.

Wall Street continues to back the airline’s prospects. DAL stock is currently carrying an overall rating of “Strong Buy.” Among 24 analysts covering the name, 22 recommend “Strong Buy,” one assigns a “Moderate Buy,” and one maintains a “Hold” rating.

DAL stock has already climbed above its average analyst price target of $84.93. Meanwhile, the Street-High target of $105 points to an additional 15.8% upside from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)