/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

Intel (INTC) is once again back in the Wall Street headlines. This happened when Nancy Pelosi’s latest filing showed 200 Intel call options with a $50 strike price and a March 19, 2027, expiration date, valued between $1.5 million and $6 million. That is the kind of move that makes traders lean in. But Intel is still a real business story, not a political trading story.

The company makes server chips, client chips, and foundry services, and the stock still lives or dies on execution. The key question is simple. Has Intel improved enough to deserve fresh money, or has the rally already done the work for you?

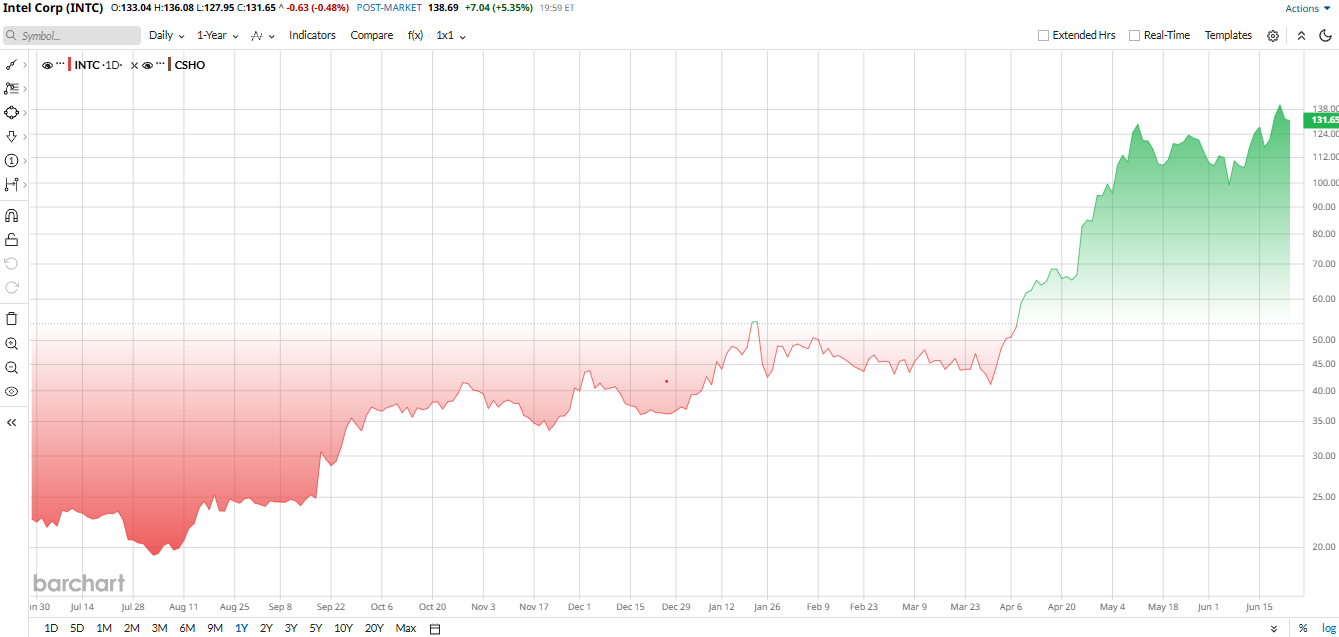

Intel Stock Has Already Run Far

Intel has been one of the hottest names in chips this year. Barchart says the stock is up 253% year-to-date (YTD) and more than 485% over the past 12 months. That kind of move did not come from one filing. It came from a long list of catalysts. AI demand helped. So did the U.S. government stake, SoftBank’s (SFTBY) backing, Nvidia’s (NVDA) support, and the market’s growing belief that Intel can still matter in CPUs and manufacturing. More recently, the Apple (AAPL) chatter and BofA’s “Buy” upgrade with a $135 target kept the momentum alive.

This is where the story gets tricky. INTC stock trades at about 6 times forward sales, which looks cheaper than Lam Research (LRCX) at 11.8 times and Applied Materials (AMAT) at 9.1 times. But on earnings, Intel is still rich. One recent comparison put Intel’s forward P/E at over 95, far above healthy chip peers. That tells you the stock is not a clean bargain. It is a turnaround bet. Investors are paying for a future that has not fully shown up in profits yet.

Pelosi Matters Less Than the Price Action

Pelosi’s disclosure is interesting, but the market already had bigger things to chew on. INTC stock jumped 10.6% on June 18 after Trump said Apple had agreed to work with Intel on U.S. chip design and manufacturing. Before that, BofA’s upgrade pushed the stock higher too.

That is the real message here. Intel is trading on turnaround headlines, not on one politician’s trade. If the Apple link becomes real, it could help Intel’s foundry pitch. If it stays a rumor, the stock still needs the business to keep improving on its own.

The Latest Quarter Still Shows Real Progress

Intel’s first quarter of 2026 was much better than many expected. Revenue came in at $13.58 billion, up 7% year-over-year (YoY). The Data Center and AI unit brought in $5.1 billion, and foundry revenue was $5.4 billion. Adjusted EPS was 29 cents, up 123% from a year earlier.

On the other side of the ledger, Intel still posted a net loss of $3.7 billion, wider than the $800 million loss a year ago, mainly because of restructuring and impairment charges. Cash from operations was $1.1 billion. CEO Lip-Bu Tan said the company is seeing demand from customers and called it real, not wishful thinking. Intel guided second-quarter revenue to $13.8 billion to $14.8 billion and adjusted EPS to 20 cents, both above Wall Street’s view.

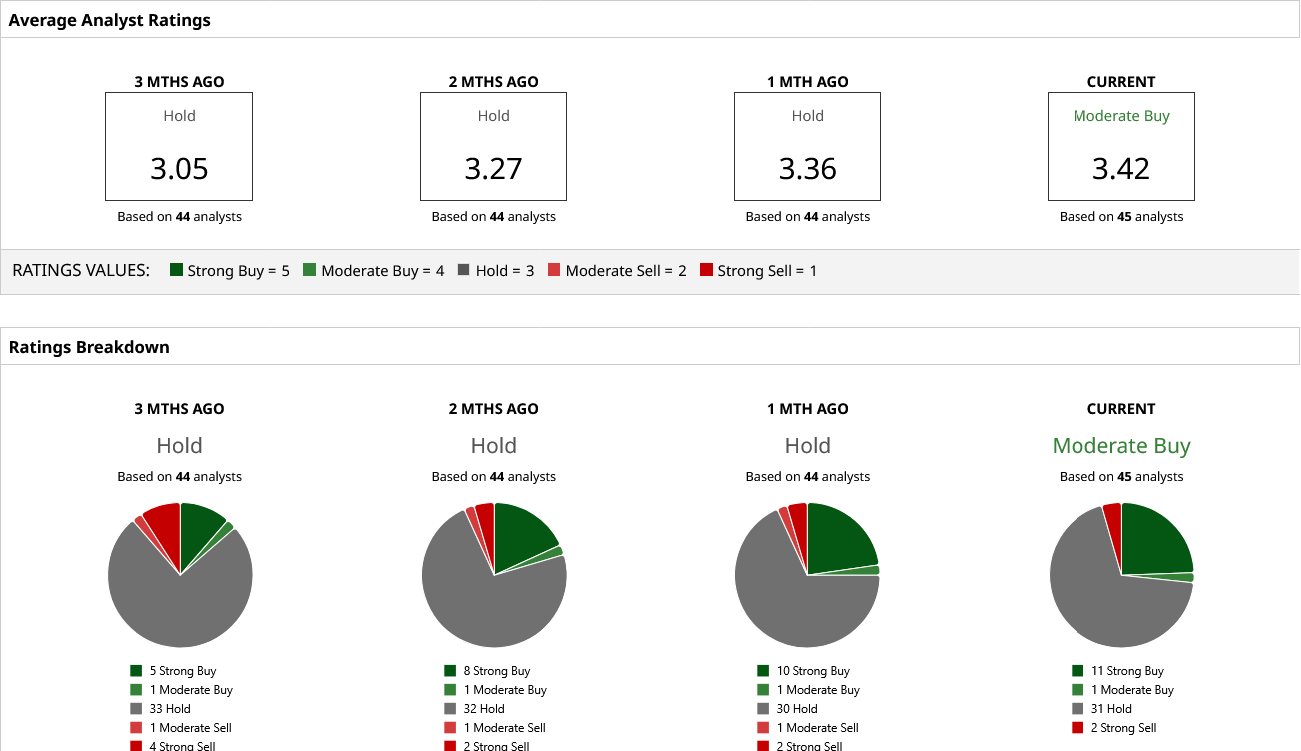

Analysts Still End on a Cautious Note

Wall Street is more mixed than the stock chart suggests. BofA is the boldest bull right now, with a “Buy” rating and a $135 target. Morgan Stanley raised its target to $56 but kept “Equal Weight,” saying stronger server demand helps, yet the roadmap still needs work. J.P. Morgan sits much lower at $35 with an “Underweight” call. Deutsche Bank lifted its target to $45, while RBC stayed more cautious.

The analyst consensus from the 45 analysts tracked by Barchart is currently at a very tepid “Moderate Buy,” with a lot of “Holds” (31). And the average target sits around $95 below the current price of about $131, which suggests 27% downside risk. So we can say that it is not a crowd running after the stock. That is a crowd still waiting for Intel to prove it.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.