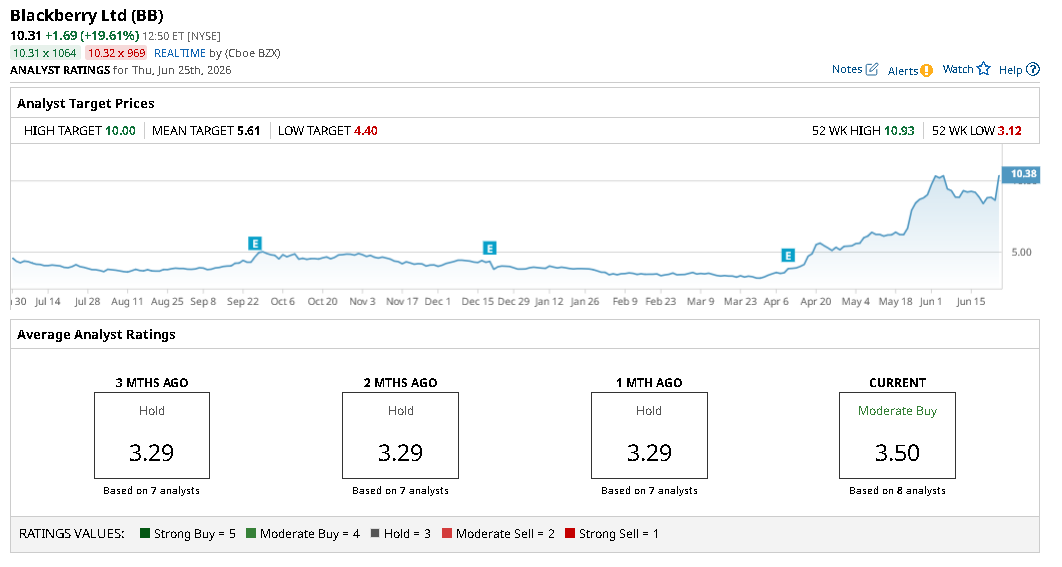

Blackberry (BB) received a new “Buy” rating from Stifel yesterday. Analysts initiated coverage with a $12 price target, indicating potential upside of nearly 35% from current levels.

The bullish call came just ahead of BB’s fiscal Q1 earnings release on June 25, which featured a 26% year-over-year increase in revenue to $153 million on a better-than-expected $0.04 per share of earnings.

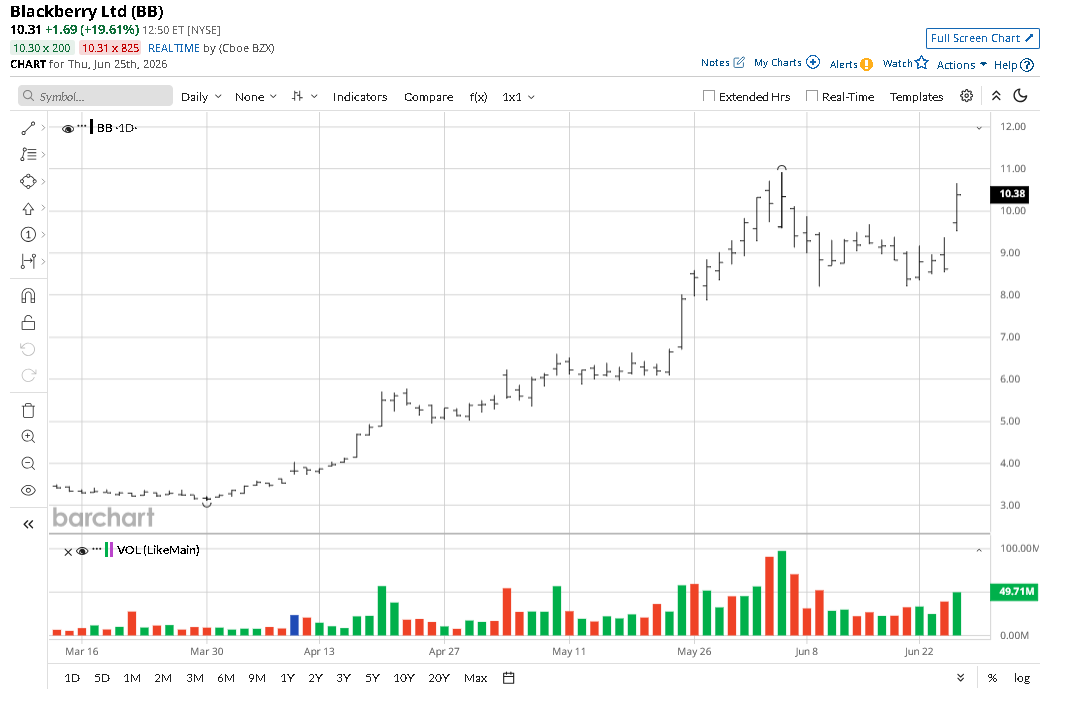

Note that Blackberry stock is already trading at about 2x its price in late March.

Stifel’s Bullish View on Blackberry Stock

Stifel’s thesis centers on the argument that the market continues to misdefine Blackberry, viewing it merely as an automotive software supplier, even though it has evolved into a mission-critical software layer powering physical AI applications across connected vehicles, robotics, industrial automation, and medical devices.

The brokerage highlighted BB's QNX operating system as a leading safety-certified platform integrated into more than 250 million vehicles globally and noted strategic partnerships with major semiconductor firms, including Nvidia (NVDA), Qualcomm (QCOM), and Advanced Micro Devices (AMD).

QNX revenue grew 26% in fiscal Q1, with management expecting similar year-on-year growth in the current quarter — supported by a royalty backlog that reached roughly $950 million.

Stifel sees significant expansion potential beyond automotive, noting that general embedded markets, including factories, robotics, and healthcare, already account for about 20% of QNX revenue.

The firm estimates that BB could ultimately address a revenue opportunity more than ten times larger than its current QNX business as physical AI adoption expands across industries.

Recent wins, such as an AI-enabled heart pump project for Johnson & Johnson (JNJ) and industrial automation deployments, underscore this diversification and make BB stock compelling for the remainder of 2026.

What Else Could Drive BB Shares Higher?

Beyond QNX, Stifel views the Secure Communications division as emerging from years of decline, with recent customer wins including the U.S. Internal Revenue Service and Germany’s Bundesbank.

Revenue in that segment went up 24% year-over-year to $73.6 million in the company’s first financial quarter. The brokerage also points to Blackberry IVY, a vehicle-data platform developed with Amazon, as creating opportunities for ongoing software-based revenue streams.

From a financial perspective, Stifel forecasts Blackberry’s revenue will rise nearly 10% in fiscal 2027 to about $602 million, with adjusted EBITDA increasing to $122 million from $107 million.

The shift toward higher-quality recurring royalty revenue is expected to support stronger margins and improved free cash flow generation, and drive Blackberry shares up further over time.

Blackberry’s CFO has stated that the company has transitioned from a cash-burning business into a profitable software company, with turnaround efforts largely complete and the focus now shifting from cost-cutting to revenue growth.

What’s the Consensus Rating on Blackberry

With a market cap hovering around $6 billion, Blackberry remains a relatively small-cap name in the software space, suggesting room for further re-rating if the company can deliver consistent growth and demonstrate the broader applicability of its platform beyond automotive.

Note that Stifel is not only the only Wall Street firm that’s bullish on BB shares for the next 12 months. According to Barchart, the consensus rating on Blackberry also currently sits at “Moderate Buy.”

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)