The semiconductor sector now makes up about 14% of the S&P 500 Index ($SPX), which is more than Energy, Materials, and Utilities combined. That growth is being driven by heavy spending on AI infrastructure, a trend Wall Street expects to continue well beyond 2028.

Chip stocks have been moving higher in recent sessions, with Applied Materials (AMAT) and Lam Research (LRCX) gaining on stronger expectations for NAND demand and higher spending on advanced tech. At the same time, forecasts suggest semiconductor equipment growth could exceed 30% in 2026, supported by massive AI spending and ongoing data center expansion.

Teradyne (TER) is right in the middle of this trend, benefiting as more complex AI chips require advanced testing solutions. The stock has surged 37.3% over the past three months and was recently added to the Nasdaq-100 Index ($IUXX), highlighting its rising importance in the space.

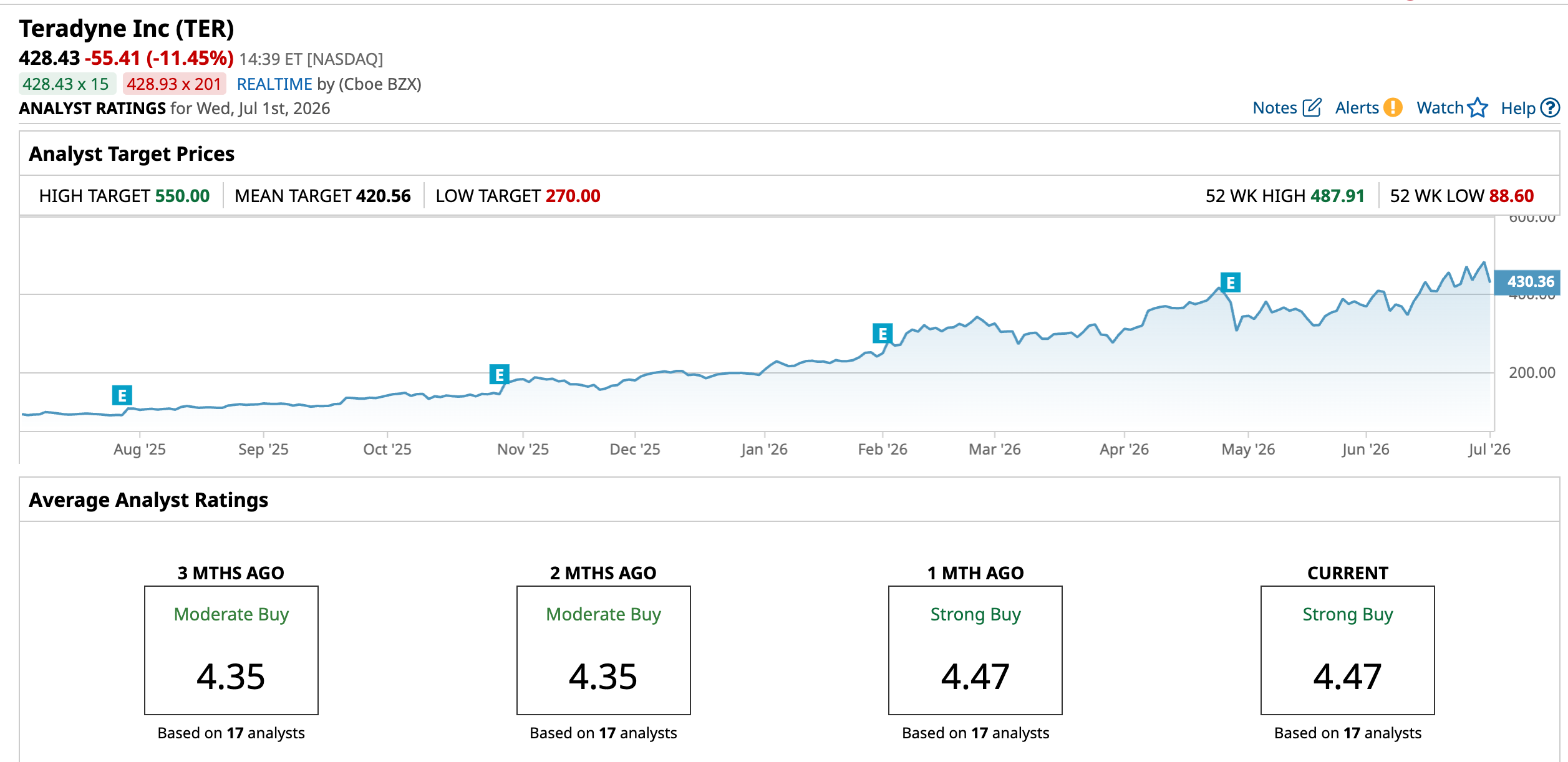

Susquehanna Financial has raised its price target on Teradyne to a new Street-high of $550 from $415, pointing to stronger expectations for semiconductor equipment spending.

With analysts already bullish and earnings momentum holding up, how much additional upside remains for Teradyne as AI infrastructure spending accelerates?

Inside the Latest Financials

Teradyne makes automated test equipment used by chipmakers, and it also has a growing robotics and industrial automation business. The stock has been on a huge run, climbing 366.35% over the past 52 weeks and 121.47% so far this year.

But that kind of move has made the stock expensive. Teradyne is trading at a forward price-to-earnings ratio of 64.31 times, well above the sector average of 24.52 times.

Also, TER pays a quarterly dividend. Its most recent payout was $0.13 per share on May 21, 2026. That gives the stock a dividend yield of 0.11%, with a low forward payout ratio of 8.43%. The company has only one year of dividend growth, and its yield is still far below the technology sector average of 1.37%.

In Q1 CY2026, revenue came in at $1.28 billion, ahead of the $1.21 billion analysts were expecting, and up 87% from a year earlier. Adjusted EPS was $2.56, beating estimates by 21.1%. Operating income reached $494.9 million, with a 38.6% margin, also comfortably ahead of forecasts.

Operating margin improved to 36.9% from 17.6% a year ago, while free cash flow margin rose to 15.6% from 14.2%. Looking ahead, Teradyne expects Q2 revenue of about $1.2 billion and adjusted EPS of $2.01, both above consensus. The company said about 70% of its revenue is now tied to AI-related demand.

Drivers Behind Teradyne’s Growth

Teradyne recently acquired TestInsight, a company that makes software for developing semiconductor tests. This gives Teradyne better tools for converting patterns, validating chips, and running virtual tests. The idea is to prepare test programs ready faster, reduce debugging time, and improve coverage so that complex AI and data center chips can hit the market sooner. It also pulls Teradyne deeper into the earlier stages of design-to-test, keeping customers more closely tied to its platform.

On the hardware side, the firm is working with Tokyo Electron (TOELY) on a combined test cell for screening known good devices. It pairs Teradyne's UltraFLEXplus system with Tokyo Electron's Prexa SDP to handle testing needs in advanced packaging. This puts Teradyne in the middle of a bigger production chain that includes fabless designers, foundries, and OSATs, allowing chips to be screened at multiple points as AI semiconductors get more complex.

Outside of chips, Teradyne is growing its robotics business through a bigger partnership with Flextronics Intl Ltd (FLEX). Flex makes key parts for Universal Robots and Mobile Industrial Robots, and it also uses those robots in its own factories around the world. That setup gives Teradyne real-world feedback on how the robots perform, helping it validate and roll out automation solutions faster.

Street Backs Stronger Upside

Teradyne will report earnings next on August 4. For the quarter ending in June, analysts expect EPS of $2.04, a sharp jump from $0.57 a year ago, which would mark a 257.9% increase. For the full 2026 fiscal year, the consensus stands at $7.20 per share, up 81.82% from $3.96 in the prior year.

Analysts are largely staying with the stock. Morgan Stanley kept an “Equal Weight” rating but lifted its price target to $387 in late April, signaling that chip testing demand looks durable even if the firm is not ready to get more aggressive.

At Bank of America, analyst Vivek Arya stayed at “Buy” and raised his target to $525 from $365, pointing to a multi-year cycle where AI computing and more complex memory testing needs keep driving business higher.

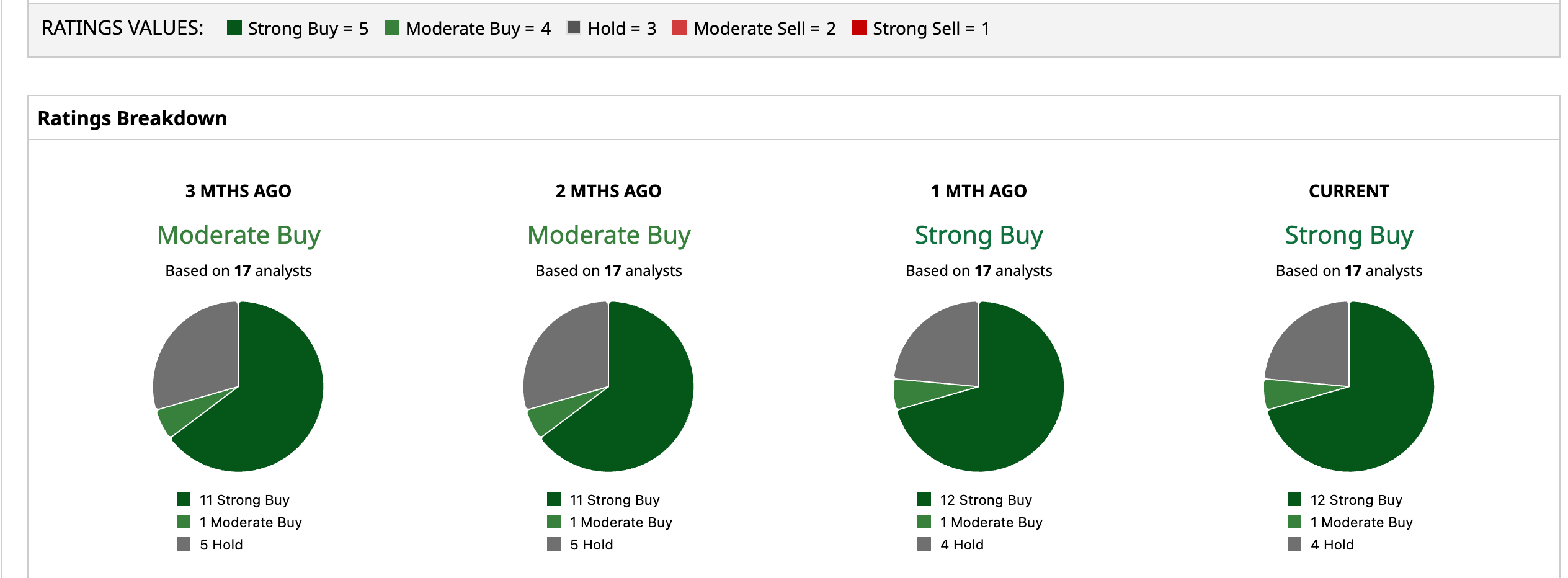

Clearly, the Street is behind the name. Of 17 analysts covering Teradyne, a consensus rates it a “Strong Buy”. A consensus price target of $420.56 represents a 1.84% downside from here. However, the Street-high price target of $550 implies a potential 28.4% gain over the next 12 months.

Conclusion

Teradyne still looks tilted to the upside, but the path from here is less straightforward than the past year’s rally suggests. The company is clearly executing well, with AI-driven demand, strong earnings growth, and expanding capabilities supporting the broader bull case that firms like Susquehanna are leaning into with that $550 target. Nevertheless, with the stock already trading above consensus targets and at a premium valuation, further gains will likely depend on continued earnings beats and sustained AI capex momentum. From here, shares most likely grind higher, but with more volatility as expectations catch up with reality.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)