/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

Investors are piling into semiconductor company Advanced Micro Devices (AMD)'s 24-day out call options today. That could mean they are bullish on AMD stock ahead of earnings in early August. Based on analysts' revenue forecasts and its strong free cash flow (FCF), these AMD call options might end up with good intrinsic value.

AMD is up over 7% in midday trading today at $577.79. Since its last quarterly report on May 5 ($355.26), AMD is up over 62%. That could be why investors are so enamoured with AMD call options today.

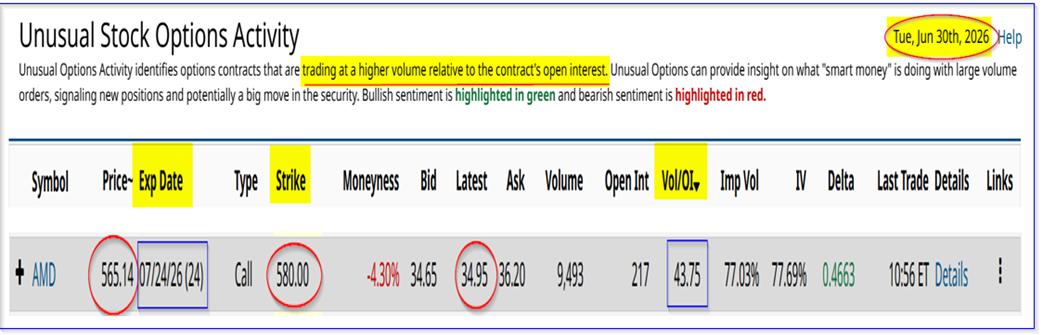

This huge, unusual trading volume in AMD calls is evident in today's Barchart Unusual Stock Options Activity Report. That report shows that the call volume is over 43 times the prior number of contracts outstanding for the $580.00 strike price expiring July 24.

The July 24 expiry is just 24 days from now, and the $580 strike price is only slightly higher than today's price (i.e., +0.38%). So, for all intents and purposes, this call option is “at-the-market,” providing huge leverage to these call option buyers.

As a result, investors buying these calls can earn a huge upside if AMD stock moves significantly higher over the next month.

For example, as the premium paid is $34.95, the breakeven point for call option buyers is $614.95. That's roughly 6.4% higher than today's price, as of the writing of this article.

It could also be a play by investors who expect AMD stock to float higher ahead of earnings due out a week after the call options expiry period (Aug. 4).

Let's look at what AMD stock could be worth, especially if its strong FCF and FCF margins persist.

AMD's Strong Free Cash Flow (FCF) Prospects

Advanced Micro Devices is in the middle of the massive chip-related spending by AI hyperscalers. As a result, analysts are projecting massive increases in revenue over the next year, along with significant accompanying gains in its FCF and FCF margins.

For example, Seeking Alpha reports that 47 analysts forecast 2027 revenue of $78.87 billion, up 55.5% from $49.45 billion in 2026. (2026 forecasts are also up 34% from $34.64 in 2025, but that doesn't matter as investors only care about the future.)

Moreover, last quarter, AMD generated $2.566 billion in free cash flow (FCF) on $10.253 billion in revenue, resulting in a 25.03% FCF margin, according to Stock Analysis. The margin over the last 12 months ending Q1 was $5.619 billion, with a 15% FCF margin.

So, if AMD generates strong FCF in Q2, along with a similar 25% FCF margin, analysts are likely to forecast this over the next 12 months and next year. Here is what that could imply:

$78.87 b 27 revenue x 0.25 = $19.67 billion FCF

That could lead to a significantly higher stock price.

Fair Market Value for AMD Stock

Today, AMD's market cap is $943.39 billion, according to Yahoo! Finance's calculations. That means that if AMD were to pay out 100% of its last 12 months' FCF as a dividend, the yield would be:

$5.619b / $943.39b = 0.0059 = 0.60% FCF yield

However, using a run-rate FCF, i.e., assuming its Q1 FCF stays flat for the next 4 quarters, its FCF yield would be higher:

$2.566b x 4 = $10.264b run rate FCF

$10.264b / $943.39 = 0.0109 = 1.09% FCF yield

So, let's use a 1.09% FCF yield to estimate AMD's fair market value (FMV) going forward:

$19.67b 2027 FCF est / 0.0109 = $1,767.9 billion FMV (i.e., $1.768 trillion)

That is 87.4% higher than today's market cap of $943.39 billion. In other words, the price target (PT)over the next 12 months for 2027 is:

$577.79 x 1.874 = $1,082.78 PT

Average Price Targets (PTs) for AMD Stock

Moreover, just to be conservative, let's assume that the FCF margin is only 20% for 2027. That leads to a forecast of $15.77 billion in FCF, and an FMV of $1,447 billion:

$15.77b / 0.0109 = $1,447 billion FMV

That is 53.4% higher than today's price, implying a PT of $886:

$577.79 x 1.534 = $886.33 PT

The bottom line is that AMD stock is between 53.4% and 87.4% undervalued, or +70% too cheap, with an average PT of $984.55 per share.

That could be one reason why there is so much at-the-market call option buying today in AMD stock.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)