/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)

With a market cap of $103.1 billion, ServiceNow, Inc. (NOW) is the AI control tower for business reinvention, providing a unified AI Platform that integrates with any cloud, AI model, and data source to orchestrate enterprise workflows. By connecting legacy systems, cloud applications, departmental tools, and AI agents into a single platform, ServiceNow enables organizations to automate operations, improve efficiency, and drive measurable business outcomes.

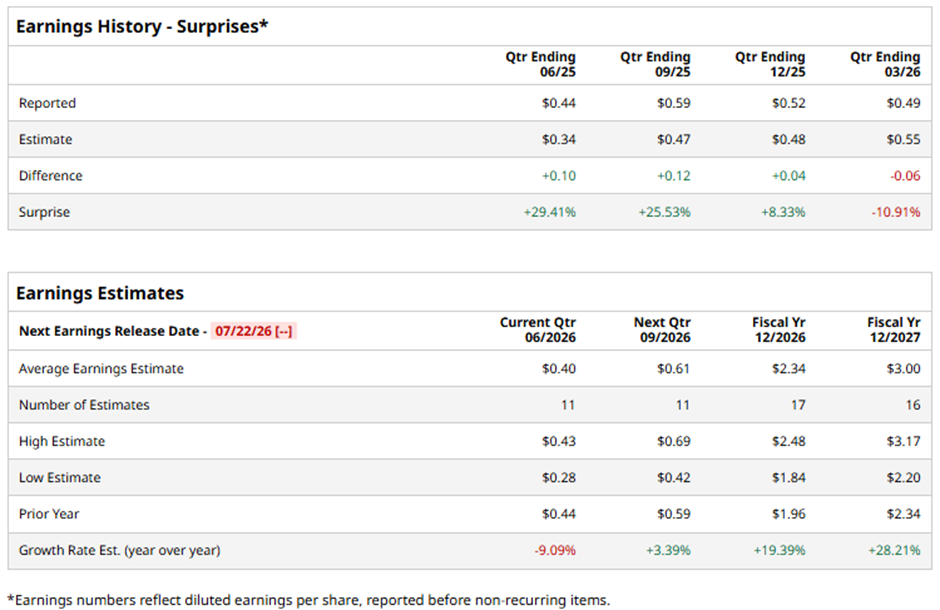

The Santa Clara, California-based company is slated to announce its fiscal Q2 2026 results soon. Ahead of the event, analysts expect NOW to report a profit of $0.40 per share, a 9.1% decline from $0.44 per share in the year-ago quarter. It has exceeded Wall Street's earnings expectations in three of the past four quarters while missing on another occasion.

For fiscal 2026, analysts expect the business software specialist to report EPS of $2.34, an increase of 19.4% from $1.96 in fiscal 2025. In addition, EPS is anticipated to grow 28.2% year-over-year to $3 in fiscal 2027.

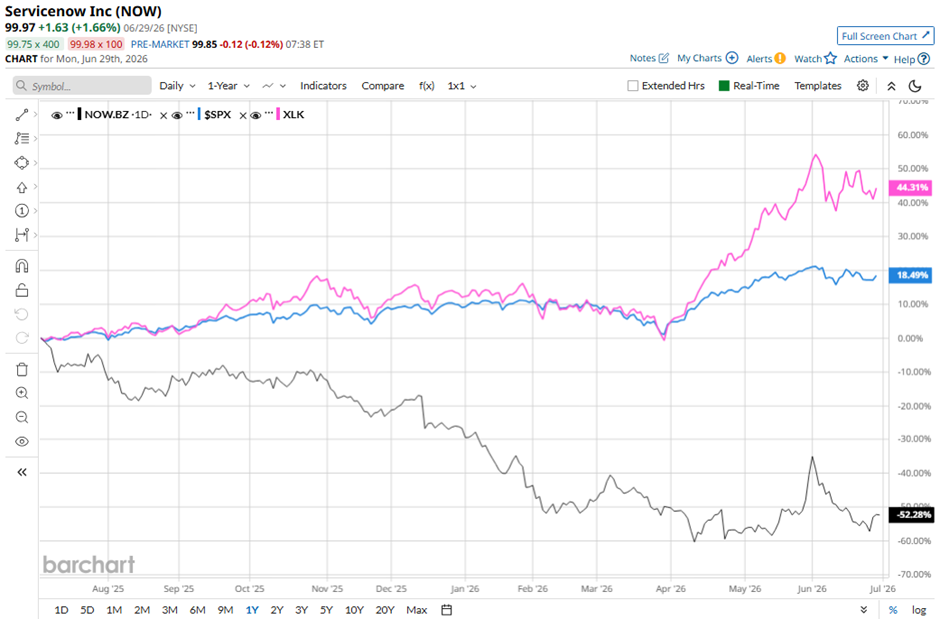

Shares of ServiceNow have decreased 51.1% over the past 52 weeks, lagging behind the broader S&P 500 Index's ($SPX) 19.9% gain and the State Street Technology Select Sector SPDR ETF's (XLK) 47.9% return over the same period.

Shares of ServiceNow tumbled 17.8% following its Q1 2026 results on Apr. 22 as the company projected a lower-than-expected full-year subscription adjusted gross margin of 81.5%, below analysts’ estimate, primarily due to the impact of recent acquisitions, including the Armis deal. Investors were also concerned that subscription revenue growth faced an approximately 75-basis-point headwind from delayed closings of several large on-premise deals in the Middle East caused by ongoing regional conflict.

Although Q1 revenue rose 22% year-over-year to $3.77 billion and the company raised its full-year subscription revenue forecast to $15.74 billion - $15.78 billion, the weaker margin outlook overshadowed the otherwise strong growth and guidance.

Analysts' consensus view on NOW stock remains bullish, with a "Strong Buy" rating overall. Out of 44 analysts covering the stock, 36 recommend a "Strong Buy," three "Moderate Buys," four give a "Hold" rating, and one "Strong Sell." This configuration is slightly more bullish than three months ago, with 35 analysts suggesting a "Strong Buy."

The average analyst price target of $143.93, suggesting a potential upside of nearly 44% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)