/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

The tech sector is seeing strong momentum from artificial intelligence, especially in data centers and AI hardware. Recent developments point to fast growth across the space, including Nvidia's (NVDA) push into AI PCs and progress from Intel Corporation (INTC) with its SuperClaw AI tool. Dell Technologies (DELL) has been one of the biggest winners here, with its AI server business posting huge gains, including 757% year-over-year (YOY) growth last quarter and a surge in orders.

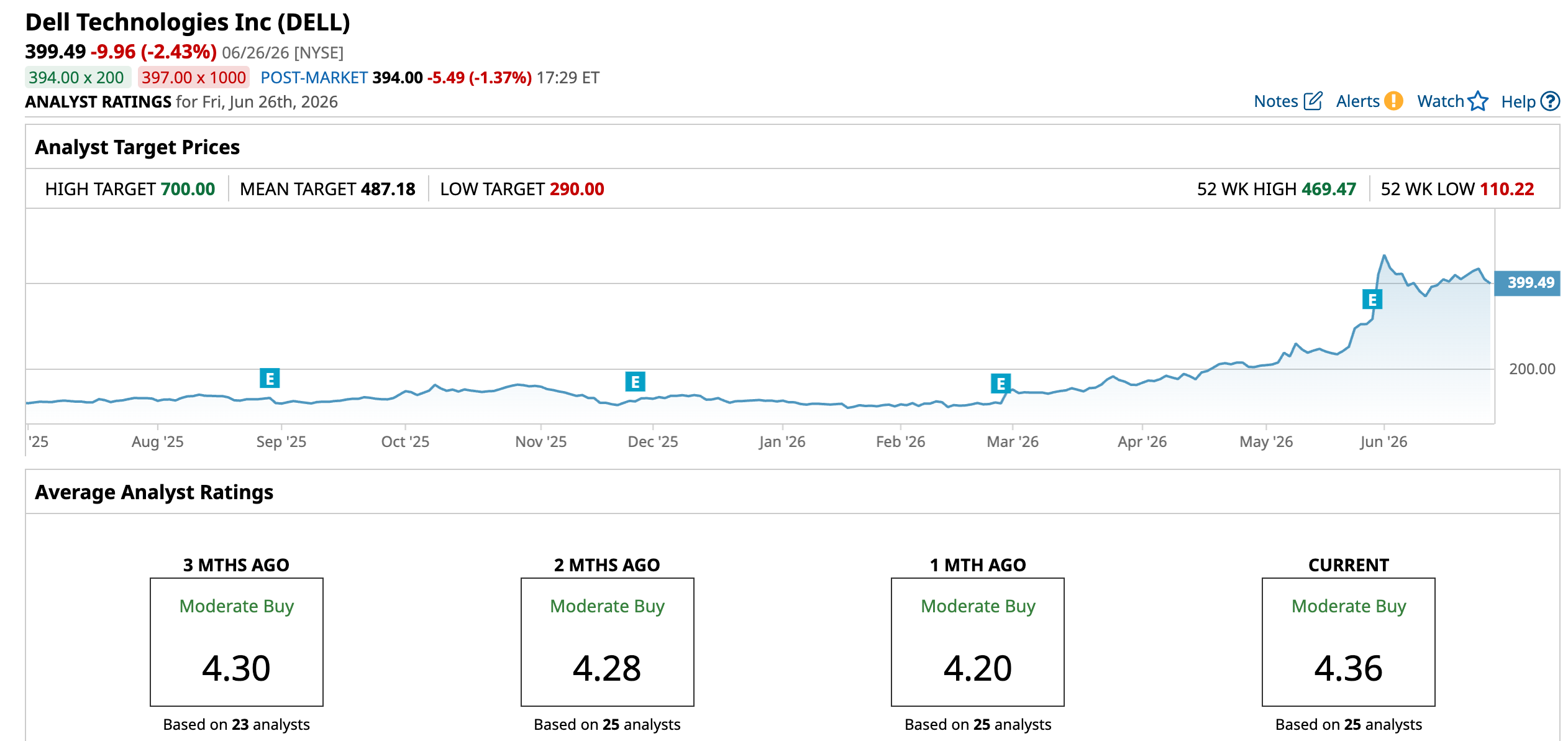

That strength sent Dell Technologies stock sharply higher after its fiscal fourth-quarter earnings in late February 2026. Shares jumped more than 200%, with year-to-date (YTD) gains nearing 240% and 52-week gains above 260%, well ahead of the broader tech sector. But the rally hit some pressure on June 25 after GF Securities downgraded the stock, pushing shares down over 9% and placing it among the S&P 500 Index's ($SPX) biggest losers that day.

With Dell’s transformation into a leading AI infrastructure player now under fresh scrutiny from Wall Street, is the nearly 200% post-earnings run finally losing steam?

Breaking Down the Latest Numbers

Dell Technologies operates a diversified model spanning personal computers, enterprise infrastructure, and increasingly, AI-optimized data center solutions, positioning it at the intersection of traditional IT and next-generation computing demand.

The stock has been on a massive run, up 217.11% over the past 52 weeks and 217.36% YTD.

Even after that surge, Dell Technologies trades at a forward price-to-earnings of 24.33 times versus the sector’s 23.72 times, not far off peers.

It also returns some cash to shareholders, with a 0.54% dividend yield and a $0.63 payout last made on April 21, 2026. The forward payout ratio is 17.11%, backed by four straight years of dividend increases and quarterly payments.

First-quarter fiscal 2027 revenue came in at a record $43.8 billion, up 88% YOY. Diluted EPS rose 282% to $5.24, while non-GAAP EPS reached $4.86, up 214%. Cash flow from operations was $4.1 billion, helping fund $2.1 billion in shareholder returns. Most of the growth came from the Infrastructure Solutions Group, where revenue jumped 181% to $29.0 billion, driven by AI servers, which alone brought in $16.1 billion, up 757%. The Client Solutions Group was more steady, with revenue up 17% to $14.6 billion as the PC market stabilized. Looking ahead, Dell Technologies expects full-year revenue of about $167 billion, with AI server revenue projected to reach $60 billion.

What’s Still Driving Dell

Dell Technologies is leaning heavily on its “Dell AI Factory with Nvidia,” and it is starting to show in real deployments. Its new PowerEdge XE8812 server, built on Nvidia's Vera Rubin NVL4 platform, can scale up to 144 GPUs per rack, targeting heavy AI and high-performance computing workloads. It runs on the PowerRack 9100 system, built to open standards, and puts Dell Technologies right in the middle of data center upgrades tied to AI demand.

That push is backed by large, steady contracts. Dell Technologies recently secured a $9.7 billion, five-year deal with the U.S. Department of Defense to provide software, including Microsoft Corporation (MSFT) products like Microsoft 365 and cloud subscriptions. The deal simplifies the way the Pentagon buys software and strengthens Dell’s long-standing relationship with Microsoft, keeping it tied to critical government systems.

At the same time, Dell Technologies is bringing AI closer to where work happens. Its Deskside Agentic AI setup lets companies run AI tools locally instead of relying fully on the cloud, helping cut costs, reduce delays, and manage data more easily. With Nvidia OpenShell now supported across its AI systems, Dell is linking everything from deskside setups to full data center servers into one connected environment.

Analysts Reassess the Upside

Dell Technologies is set to report earnings again on August 27, and expectations are still strong. For the current quarter ending July 2026, analysts see EPS at $4.63, up 120.48% from $2.10 a year ago. For the full year, fiscal 2027 EPS is projected at $17.74 compared to $9.25 last year, a 91.78% jump.

Not all analysts are turning cautious. Piper Sandler kept an “Overweight” rating and a $497 price target just before the downgrade, pointing to Dell Technologies’s strong position in AI infrastructure.

Mizuho also stayed positive in May, maintaining an “Outperform” rating while raising its target from $260 to $300, driven by growing demand for AI server workloads. Citi took a similar stance, lifting its target from $180 to $235 and keeping a “Buy” rating, backed by strong order visibility and better storage performance.

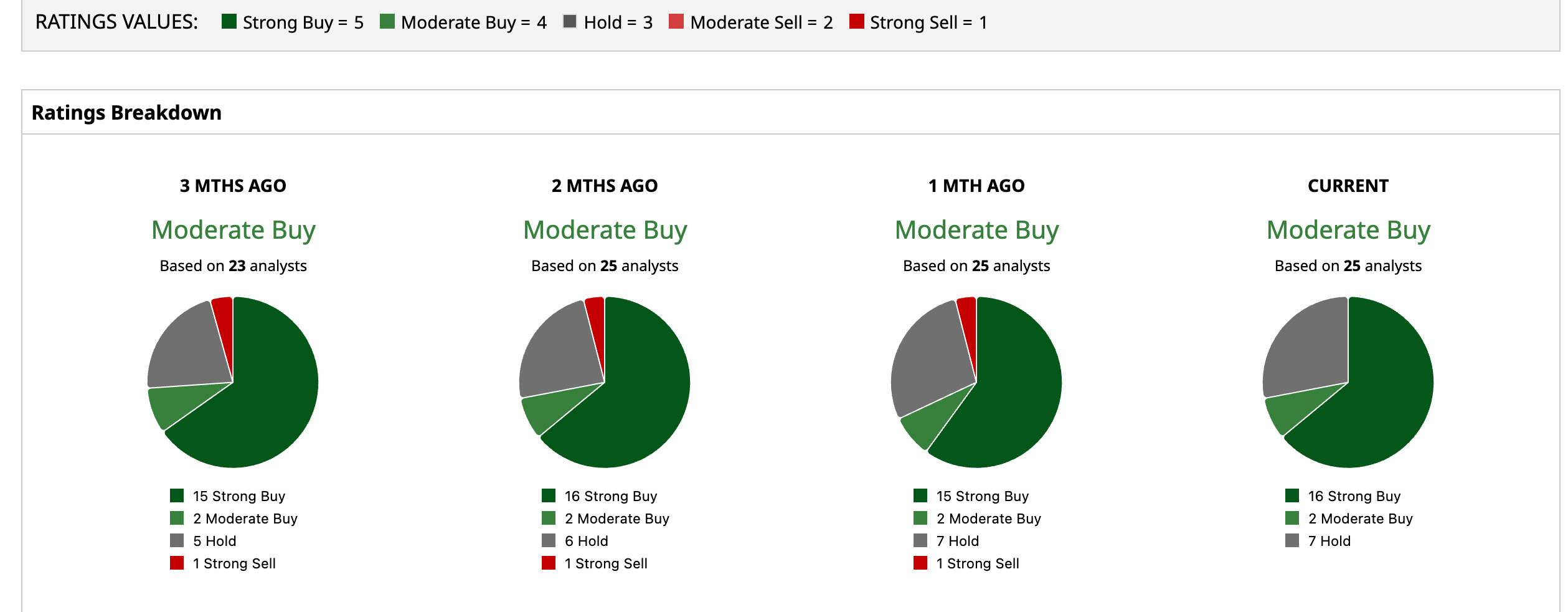

Overall, sentiment is still solid. All 25 analysts covering Dell Technologies rate it a consensus “Moderate Buy,” with an average price target of $487.18. That suggests about 22% upside from current levels. The Street-high target of $700 suggests that DELL could climb 75.2% higher over the next 12 months.

Conclusion

Dell’s rally does not look finished, but it is clearly entering a more selective phase. The downgrade highlights valuation concerns after an extraordinary run, yet the core story remains intact with AI-driven earnings growth still accelerating and estimates continuing to move higher. With consensus still pointing to upside and demand for AI infrastructure showing no signs of slowing, the trend likely favors further gains, though at a more measured pace. Near term, shares could consolidate or pull back on valuation pressure, but the broader direction still leans upward as long as execution and AI demand hold.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)