/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Round Rock, Texas-based Dell Technologies Inc. (DELL) designs, develops, manufactures, markets, sells, and supports various comprehensive and integrated solutions, products, and services. Valued at $277.2 billion by market cap, the company offers laptops, desktops, tablets, workstations, servers, monitors, printers, gateways, software, storage, and networking products.

Companies worth $200 billion or more are generally described as “mega-cap stocks,” and DELL definitely fits that description, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance within the computer hardware industry. DELL holds top-three market share in PCs, displays, mainstream servers, and external storage. Its brand is tied to quality and reliability, building a loyal customer base.

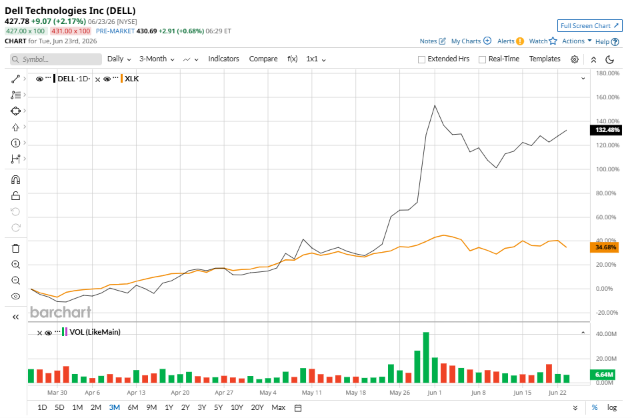

Despite its notable strength, DELL slipped 8.9% from its 52-week high of $469.47, achieved on Jun. 1. Over the past three months, DELL stock has gained 159.9%, considerably outperforming theState Street Technology Select Sector SPDR ETF’s (XLK) 34.5% gains during the same time frame.

Shares of DELL rose 239.8% on a YTD basis and climbed 262.5% over the past 52 weeks, significantly outperforming XLK’s YTD gains of 27.9% and 51.7% returns over the last year.

To confirm the bullish trend, DELL has been trading above its 50-day moving average since late February. The stock is trading above its 200-day moving average over the past year, with some fluctuations.

Dell posted one of its strongest quarters as AI infrastructure demand outpaces supply across all regions. The AI pipeline is several times the backlog, with broad demand from hyperscalers, cloud providers, sovereigns, and enterprises. Its traditional servers also grew about 92% year over year on refresh cycles and rising compute needs, plus added demand from AI inference. With a record AI server backlog and improved outlook, Dell is set for robust earnings growth.

On May 28, DELL reported its Q1 results, and its shares skyrocketed 43.5% in the subsequent two trading sessions. Its adjusted EPS of $4.86 topped Wall Street expectations of $3.04. The company’s revenue was $43.8 billion, topping Wall Street forecasts of $35.5 billion. DELL expects full-year adjusted EPS to be $17.90, and revenue ranging from $165 billion to $169 billion.

In the competitive arena of computer hardware, Lenovo Group Limited (LNVGY) has lagged behind DELL, with a 141.3% uptick on a YTD basis and 146.7% gains over the past 52 weeks.

Wall Street analysts are moderately bullish on DELL’s prospects. The stock has a consensus “Moderate Buy” rating from the 25 analysts covering it, and the mean price target of $485.95 suggests a potential upside of 13.6% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.