/Insulet%20Corporation%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

With a market cap of $10.7 billion, Insulet Corporation (PODD) is a top medical device company specializing in tubeless insulin delivery systems for people with diabetes. Headquartered in Acton, Massachusetts, the company is best known for its flagship Omnipod platform, a wearable, automated insulin delivery system designed to simplify diabetes management for patients with Type 1 and Type 2 diabetes.

Shares of PODD have significantly trailed the broader market over the past 52 weeks. PODD stock has plunged 51.8% over this period, while the broader S&P 500 Index ($SPX) has gained 27.9%. Moreover, shares of PODD are down 45.5% on a YTD basis, compared to SPX’s 9.2% rise.

Zooming in further, Insulet has also underperformed the iShares U.S. Medical Devices ETF’s (IHI) 16.9% rise over the past year and 18.6% return in 2026.

On May 6, Insulet reported Q1 FY2026 results, with revenue rising 33.9% year over year to $761.70 million, driven by continued momentum in Omnipod 5 adoption and robust international growth. The company also posted significant profitability improvement, as adjusted net income climbed 35.4% to $99.8 million, while adjusted EPS increased 39.7% year over year to $1.42. Insulet further raised its full-year 2026 revenue growth guidance to 21%–23% following the strong quarter.

Despite the solid operational performance, the stock fell 9.7% immediately after the earnings release, likely due to elevated investor expectations and concerns around valuation after the company’s strong prior run-up. However, sentiment quickly recovered, with shares rebounding sharply in the following trading session and gaining 6% as investors refocused on Insulet’s accelerating growth, expanding margins, and strong long-term outlook in the diabetes technology market.

For the current fiscal year 2026, ending in December, analysts expect PODD's adjusted EPS to increase 29.4% year-over-year to $6.43. The company has a robust earnings surprise history. It beat the Street's bottom-line estimates in each of the past four quarters.

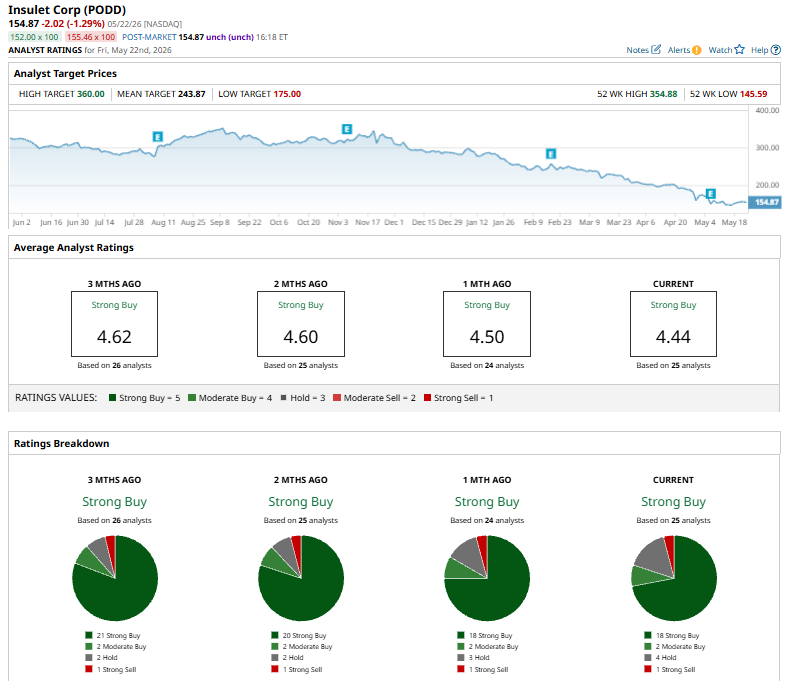

Among the 25 analysts covering PODD stock, the consensus rating is a “Strong Buy.” That’s based on 18 “Strong Buy” ratings, two “Moderate Buys,” four “Holds,” and one “Strong Sell.”

The current configuration is bearish than two months ago when 20 analysts had suggested a “Strong Buy” rating for the stock.

On May 20, William Blair analyst Steve Lichtman initiated an “Outperform” rating on Insulet Corporation, reflecting continued confidence in the company’s growth trajectory within the diabetes technology market. Moreover, on May 12, Benchmark initiated coverage on the stock with a "Buy" rating and a $250 price target.

Insulet’s mean price target of $243.87 implies a modest 57.5% premium to its current price. The Street-high target of $360 indicates the stock could soar by 132.5% from current market prices.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/The%20logo%20for%20ASML%20on%20a%20corporate%20office%20by%20Skorzewiak%20via%20Shutterstock.jpg)