/Airbnb%20Inc%20logo%20with%20red%20background%20by-%20viewimage%20via%20Shutterstock.jpg)

Valued at a market cap of $85.1 billion, Airbnb, Inc. (ABNB) is a leading global marketplace that connects travelers with a vast network of hosts offering unique accommodations and experiences. The San Francisco, California-based company facilitates a diverse array of stays ranging from private rooms and entire homes to boutique hotels and unconventional properties like villas and treehouses across nearly every country.

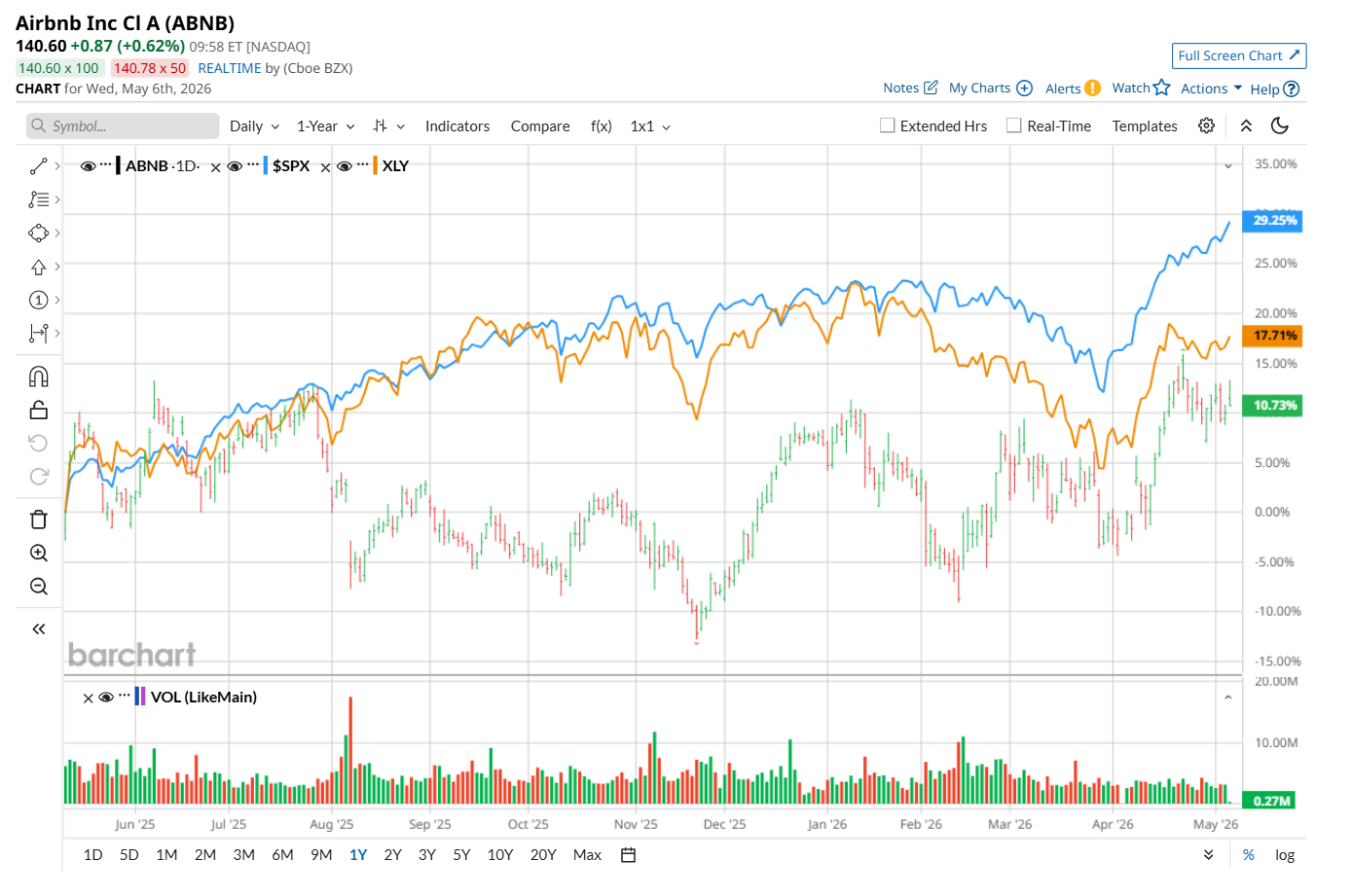

This travel services company has underperformed the broader market over the past 52 weeks. Shares of Airbnb have gained 16.6% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 28.5%. Moreover, on a YTD basis, the stock is up 4.5%, compared to SPX’s 6% rise.

Narrowing the focus, ABNB has also lagged the State Street Consumer Discretionary Select Sector SPDR ETF (XLY), which soared 20.5% over the past 52 weeks. Nonetheless, it has outpaced XLY’s marginal downtick on a YTD basis.

On Feb. 12, shares of ABNB fell 3% after the company reported mixed Q4 2025 results. Its revenue increased 12% year-over-year to $2.8 billion, exceeding Wall Street expectations, while adjusted EBITDA came in at $786 million, also ahead of estimates. However, adjusted EPS of $0.56 missed analysts’ forecasts due to elevated operating expenses and continued investments in new initiatives, weighing on investor sentiment.

For the current fiscal year, ending in December, analysts expect ABNB’s EPS to grow 22.8% year over year to $4.95. The company’s earnings surprise history is disappointing. It missed the consensus estimates in three of the last four quarters, while surpassing on another occasion.

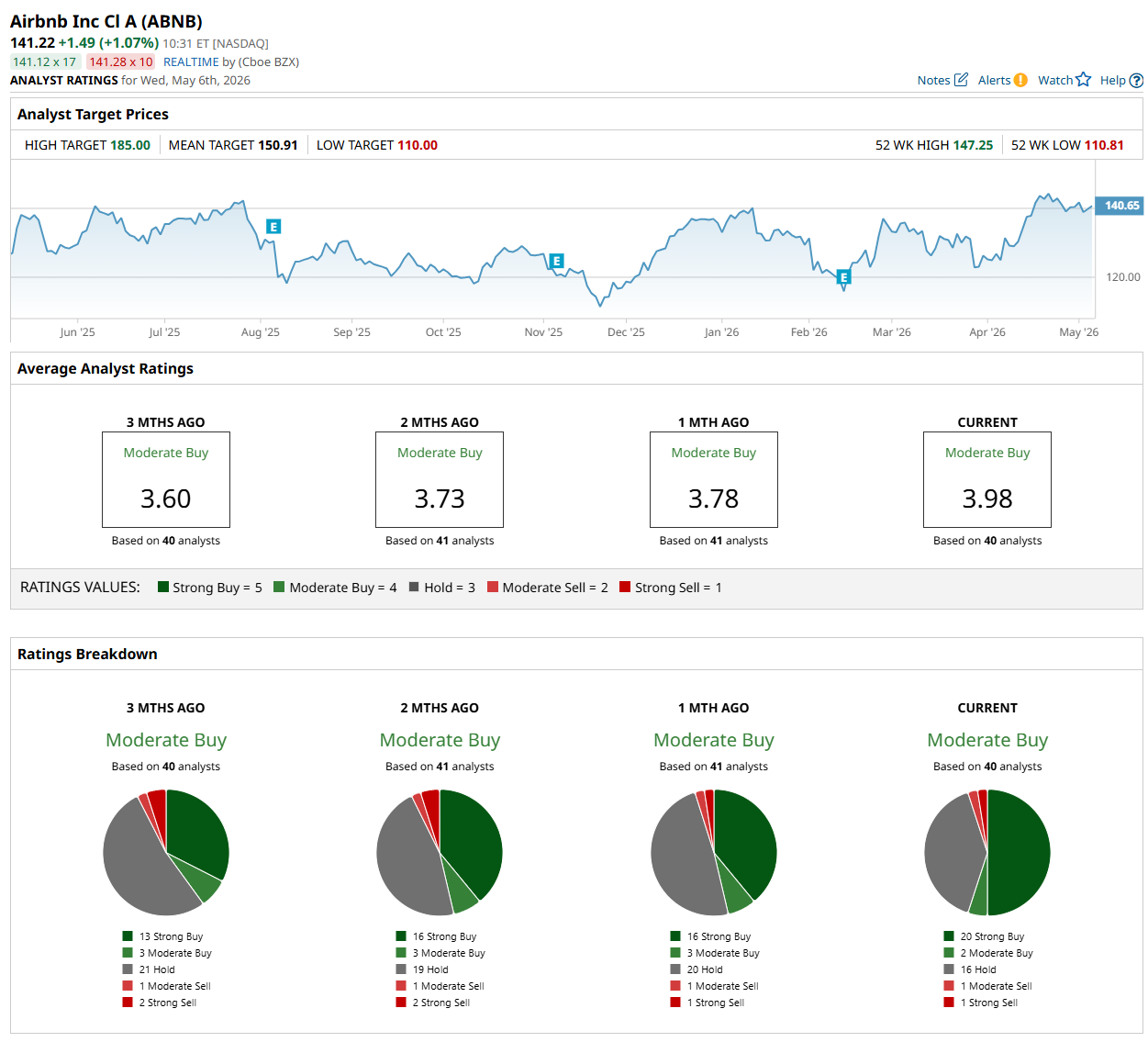

Among the 40 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on 20 “Strong Buy,” two “Moderate Buy,” 16 "Hold,” one “Moderate Sell,” and one “Strong Sell” rating.

The configuration is more bullish than a month ago, with 16 analysts suggesting a "Strong Buy” rating.

On May 4, Oppenheimer upgraded Airbnb to “Outperform” with an $180 price target, indicating a 27.5% potential upside from the current levels.

The mean price target of $150.91 suggests a 6.9% premium to its current levels, while its Street-high price target of $185 implies a 31% potential upside from the current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)