Valued at a market cap of $79.6 billion, Monster Beverage Corporation (MNST) is a leading global beverage company best known for its energy drinks, particularly under the flagship Monster Energy brand. Headquartered in California, the company has built a dominant position in the fast-growing energy drink market through strong branding, aggressive marketing, and a wide international distribution network.

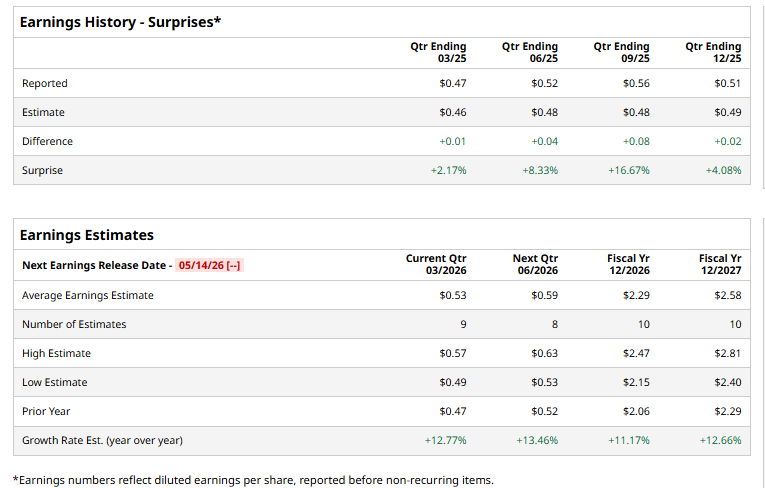

The beverage behemoth is expected to announce its fiscal 2026 Q1 earnings in the near future. Before this event, analysts expect this beverage company to report a profit of $0.53 per share, up 12.8% from $0.47 per share in the year-ago quarter. The company has surpassed Wall Street’s bottom-line estimates in each of the last four quarters.

For the current fiscal year, ending in December, analysts expect MNST to report a profit of $2.29 per share, up 11.2% from $2.06 per share in fiscal 2025. Its EPS is expected to further grow 12.7% year over year to $2.58 in fiscal 2027.

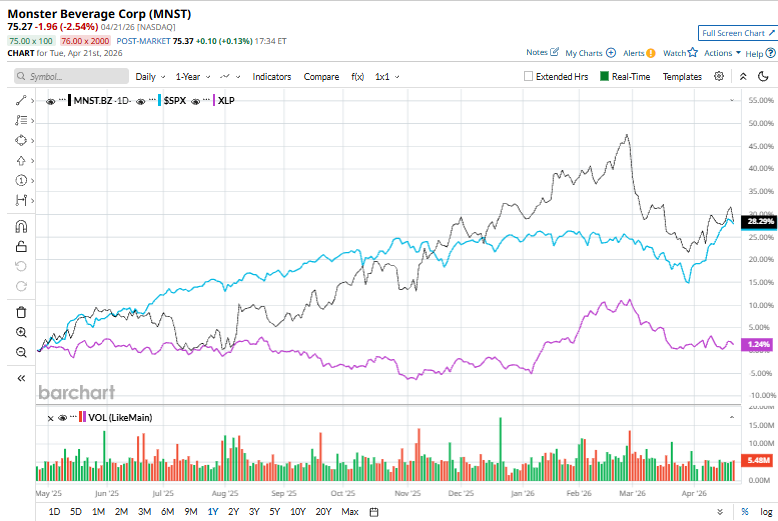

MNST has soared 29.8% over the past 52 weeks, underperforming both the S&P 500 Index's ($SPX) 33.6% return but outpacing the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) marginal uptick over the same time period.

The beverage titan has outpaced its broader sector over the past year primarily due to resilient demand for energy drinks, strong pricing power, and consistent volume growth across key international markets.

On Feb. 26, Monster Beverage reported stronger-than-expected fourth-quarter results, yet the stock slipped 1.6% in the subsequent trading session. The company posted net sales of $2.1 billion, reflecting a robust 17.6% year-over-year increase and exceeding consensus estimates by 3.9%, driven by solid global demand and continued momentum in its energy drink portfolio. Profitability was even more impressive, with adjusted EPS rising 30.8% to $0.51, ahead of analyst forecasts of $0.49, highlighting effective cost management and operating leverage.

Wall Street analysts are moderately optimistic about MNST’s stock, with an overall "Moderate Buy" rating. Among 23 analysts covering the stock, 12 recommend "Strong Buy," one suggests a "Moderate Buy,” and 10 indicate "Hold.” The mean price target of $87.27 represents a 15.9% premium from the current market prices.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)