With a market cap of around $13 billion, Avery Dennison Corporation (AVY) is a global materials science and digital identification solutions company that provides pressure-sensitive materials, labeling technologies, and branding solutions across industries such as retail, apparel, logistics, and healthcare. It operates worldwide, offering products ranging from adhesive labels and RFID solutions to graphics and reflective materials under brands like Fasson, JAC, and Avery Dennison.

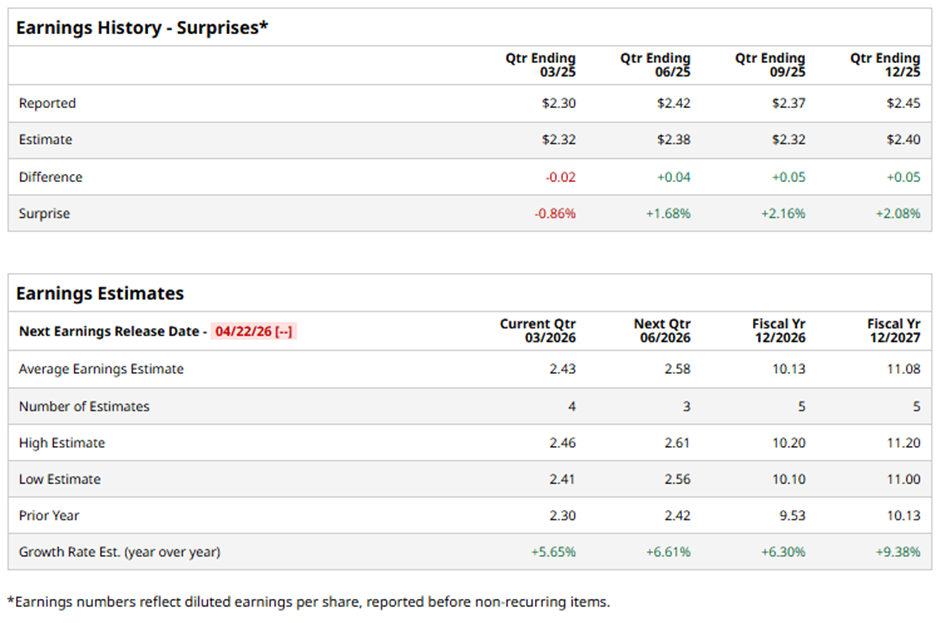

The Mentor, Ohio-based company is set to release its fiscal Q1 2026 results soon. Ahead of this event, analysts project AVY to report an adjusted EPS of $2.43, a rise of 5.7% from $2.30 in the year-ago quarter. It has exceeded Wall Street's earnings estimates in three of the last four quarters while missing on another occasion.

For fiscal 2026, analysts forecast the office products maker to report adjusted EPS of $10.13, up 6.3% from $9.53 in fiscal 2025. In addition, adjusted EPS is expected to grow 9.4% year-over-year to $11.08 in fiscal 2027.

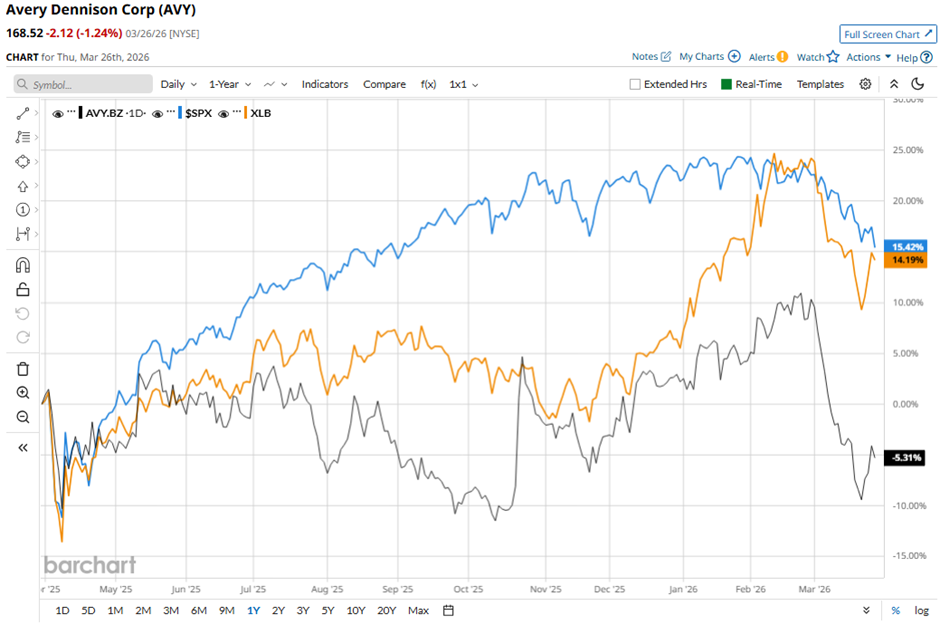

Over the past 52 weeks, Avery Dennison has declined 5.3%, underperforming the broader S&P 500 Index's ($SPX) 13.4% gain and the State Street Materials Select Sector SPDR ETF's (XLB) 13.3% return over the same time frame.

Shares of Avery Dennison rose 3.4% on Feb. 4 after the company reported stronger-than-expected Q4 2025 results, including adjusted EPS of $2.45 (up 3%) on revenue of $2.3 billion (up 4%). Investors were also encouraged by full-year adjusted EPS of $9.53, solid profitability with an adjusted EBITDA margin of 16.4%, and robust free cash flow exceeding $700 million.

The stock also gained on positive forward guidance, with Q1 2026 adjusted EPS projected at $2.40 - $2.46 and growth in high-value segments like intelligent labels and Vestcom.

Analysts' consensus view on AVY stock is cautiously optimistic, with a "Moderate Buy" rating overall. Among 13 analysts covering the stock, eight suggest a "Strong Buy," one gives a "Moderate Buy," and four recommend a "Hold." The average analyst price target of $209.50, indicating a 24.3% potential upside from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)