/Gears%20and%20cogs%20in%20a%20%20by%20machine%20by%20MustangJoe%20via%20Pixabay.jpg)

ASML Holding NY (ASML) is a Dutch multinational corporation and a foundational pillar of the global semiconductor industry. ASML is the world's sole provider of extreme ultraviolet (EUV) lithography machines, which are essential for etching the microscopic circuits found in the most advanced AI and high-performance chips. By utilizing complex laser-plasma light sources and precision optics, ASML enables chipmakers like TSMC (TSM), Intel (INTC), and Samsung to push the boundaries of Moore’s Law.

Headquartered in Veldhoven, Netherlands, the company was founded in 1984.

ASML Stock Surges

ASML stock reflects a massive 94% surge over the past year. The stock has benefited from a significant re-rating as investor sentiment toward AI infrastructure remains robust. With a market capitalization exceeding $526 billion, ASML has recovered sharply from its 2024 lows, recently hitting a 52-week high of $1,547.22, despite a relatively minor 7% pullback in the last 30 days due to broader market consolidation.

In comparison to the Nasdaq 100 ($IUXX), ASML has substantially outperformed the index over the last twelve months. While the Nasdaq 100 has seen strong gains driven by the broader "Magnificent Seven" rally, ASML’s specialized position in the semiconductor supply chain allowed it to nearly double the index's percentage returns.

ASML Posted Record Results

ASML concluded a record-breaking fiscal year 2025, reporting Q4 net sales of €9.7 billion, significantly exceeding market expectations. This performance contributed to a full-year revenue of €32.7 billion, a 16% increase compared to 2024. Net income for the quarter reached €2.8 billion, with a healthy gross margin of 52.2%. A standout metric was the record quarterly net bookings of €13.2 billion, of which €7.4 billion was specifically for EUV systems, resulting in a total order backlog of €38.8 billion by year-end.

Looking ahead, management has issued a confident outlook for 2026, projecting total net sales between €34 billion and €39 billion. This growth is expected to be driven by a transition from 4-nanometer to 3-nanometer nodes among AI accelerator clients and a continued ramp-up of 2-nanometer production.

To support this scaling, ASML announced a new €12 billion share buyback program through 2028 and increased its total 2025 dividend by 17% to €7.50 per share. Despite geopolitical export controls affecting certain shipments to China, the "notably positive" assessment from customers regarding AI-related demand suggests that ASML is entering 2026 with its strongest momentum in company history.

Analyst Bullish on ASML

TD Cowen analyst Krish Sankar maintains a "Buy" rating on ASML with a price target of €1,500 ($1,735), representing a valuation of 48 times projected 2027 earnings, and is about 25% higher than its current price level. This bullish outlook comes as ASML’s U.S.-listed shares have retreated 7% over the past month, creating what analysts describe as a "very attractive" entry point.

The stock's premium over peers like Applied Materials (AMAT) and Lam Research has compressed from 120% in 2022 to just 20% today, largely due to a market rotation away from AI-exposed semiconductor stocks and concerns over lighter EUV tool usage.

However, Sankar argues the market is underappreciating the necessity of EUV layers in future DRAM memory roadmaps and the inevitable adoption of High-NA machines. While some customers, like TSMC, have been publicly cautious about upgrading, improving reliability is expected to drive a shift toward newer 3800E and 4000F models. TD Cowen models a significant increase in system deliveries, reaching 68 tools by 2027.

For long-term investors, this valuation "delta" provides a rare chance to acquire a monopolistic leader in chip-making machinery at a significant relative discount before the next phase of logic and memory scaling begins.

Should You Buy ASML Stock?

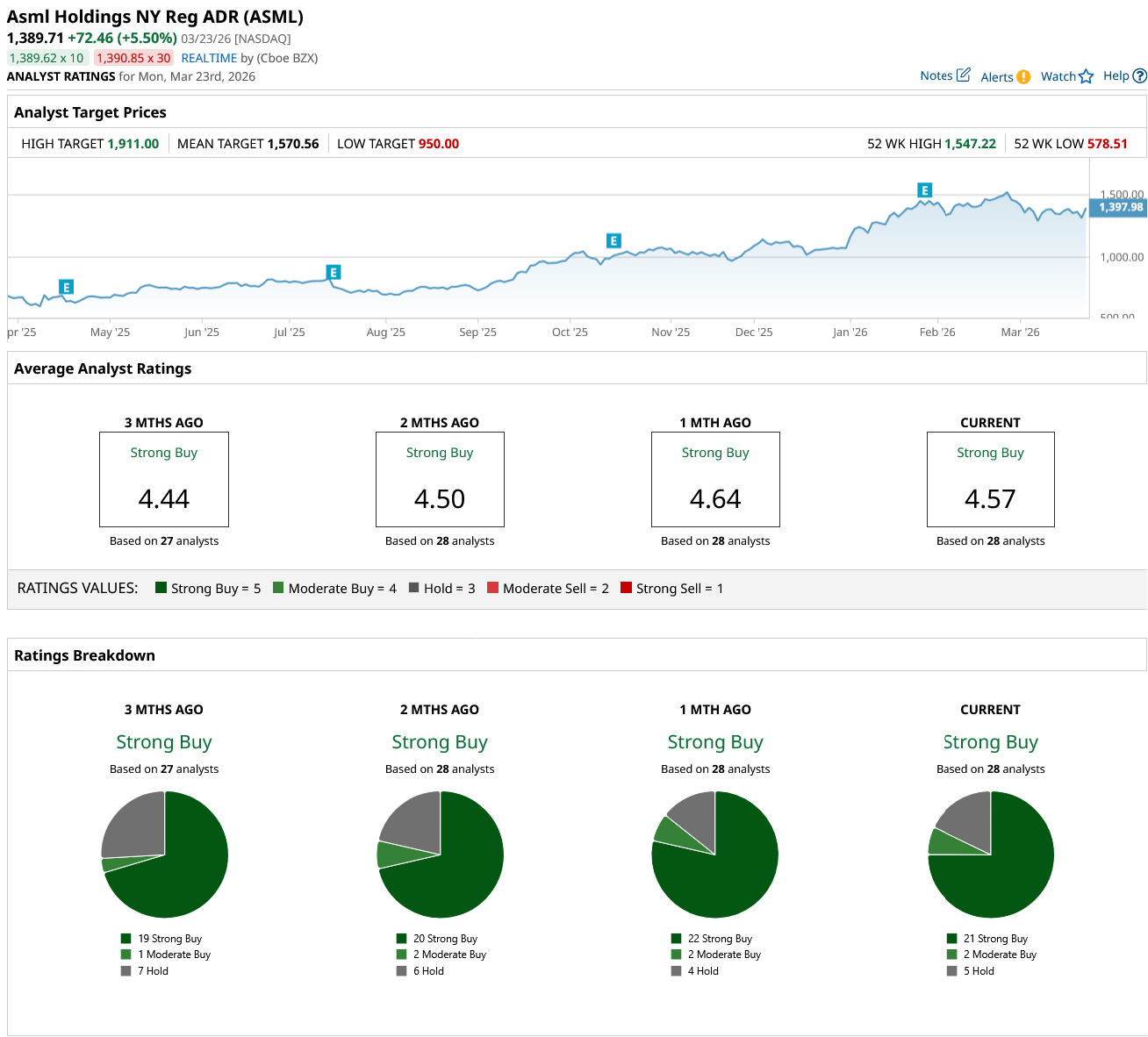

ASML remains a cornerstone of the semiconductor industry, bolstered by a "Strong Buy" consensus from 28 analysts. With 21 "Strong Buy" and TWO "Moderate Buy" ratings, the professional sentiment is overwhelmingly positive. The mean price target of $1,570.56 suggests a significant 13% upside potential from current market levels, driven by the company’s monopoly on EUV lithography tools, which are essential for the AI revolution.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)