Cincinnati, Ohio-based The Procter & Gamble Company (PG) manufactures and markets consumer products. With a market cap of $338.2 billion, the company’s product portfolio includes conditioners, shampoos, blades and razors, toothbrushes, toothpastes, dishwashing liquids, detergents, surface cleaners, air fresheners, and more. The leading multinational consumer goods company is expected to announce its fiscal second-quarter earnings for 2026 before the market opens on Thursday, Jan. 22, 2026.

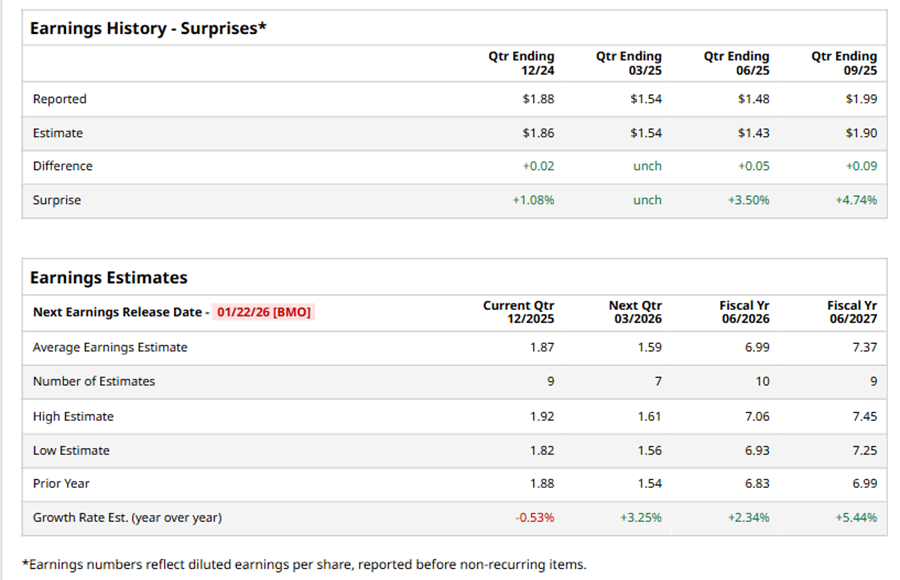

Ahead of the event, analysts expect PG to report a profit of $1.87 per share on a diluted basis, down marginally from $1.88 per share in the year-ago quarter. The company beat or matched the consensus estimates in each of the last four quarters.

For the full year, analysts expect PG to report EPS of $6.99, up 2.3% from $6.83 in fiscal 2025. Its EPS is expected to rise 5.4% year over year to $7.37 in fiscal 2027.

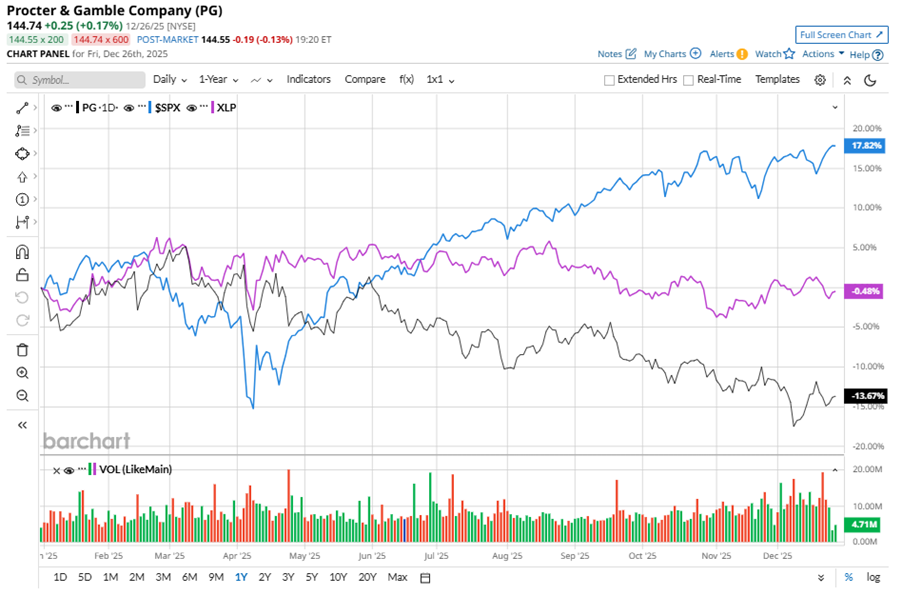

PG stock has considerably underperformed the S&P 500 Index’s ($SPX) 14.8% gains over the past 52 weeks, with shares down 14.9% during this period. Similarly, it underperformed the Consumer Staples Select Sector SPDR Fund’s (XLP) 1.8% losses over the same time frame.

Procter & Gamble is underperforming due to sector-wide challenges, higher tariffs, soft consumer spending, and competition from lower-priced brands. Despite this, fundamentals remain resilient. PG's muted sales growth and margin pressures from investments and tariffs are weighing on the stock.

On Oct. 24, PG shares closed up marginally after reporting its Q1 results. Its adjusted EPS of $1.99 exceeded Wall Street expectations of $1.90. The company’s revenue was $22.4 billion, topping Wall Street forecasts of $22.2 billion. PG expects full-year adjusted EPS to be $6.83 to $7.09.

Analysts’ consensus opinion on PG stock is moderately bullish, with a “Moderate Buy” rating overall. Out of 24 analysts covering the stock, 11 advise a “Strong Buy” rating, three suggest a “Moderate Buy,” and 10 give a “Hold.” PG’s average analyst price target is $169.68, indicating a potential upside of 17.2% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)