/F5%20Inc%20HQ%20logo-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

Seattle, Washington-based F5, Inc. (FFIV) offers multi-cloud application security and delivery solutions. Valued at $13 billion by market cap, the company offers software-based solutions and manages, controls, and optimizes internet traffic and content. F5 also offers solutions that automatically deliver internet content for service providers and e-businesses.

Shares of this multi-cloud application services and security company have underperformed the broader market over the past year. FFIV has declined 6.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 12.3%. In 2025, FFIV stock is down 10.9%, compared to the SPX’s 12.9% rise on a YTD basis.

Narrowing the focus, FFIV’s underperformance is also apparent compared to the Technology Select Sector SPDR Fund (XLK). The exchange-traded fund has gained about 21.5% over the past year. Moreover, the ETF’s 20.8% gains on a YTD basis outshine the stock’s losses over the same time frame.

FFIV underperformed after a cybersecurity breach exposed its BIG-IP product's source code and undisclosed security flaws, prompting a "significant cyber threat" warning from CISA and investor concerns, despite the company stating there was no material operational impact.

On Oct. 27, FFIV reported its Q4 results, and its shares closed down by 7.9% in the following trading session. Its adjusted EPS of $4.39 surpassed Wall Street expectations of $3.96. The company’s revenue was $810.1 million, topping Wall Street's $792.5 million forecast. FFIV expects full-year adjusted EPS in the range of $14.50 to $15.50.

For fiscal 2026, ending in September 2026, analysts expect FFIV’s EPS to decline 1.7% to $11.67 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

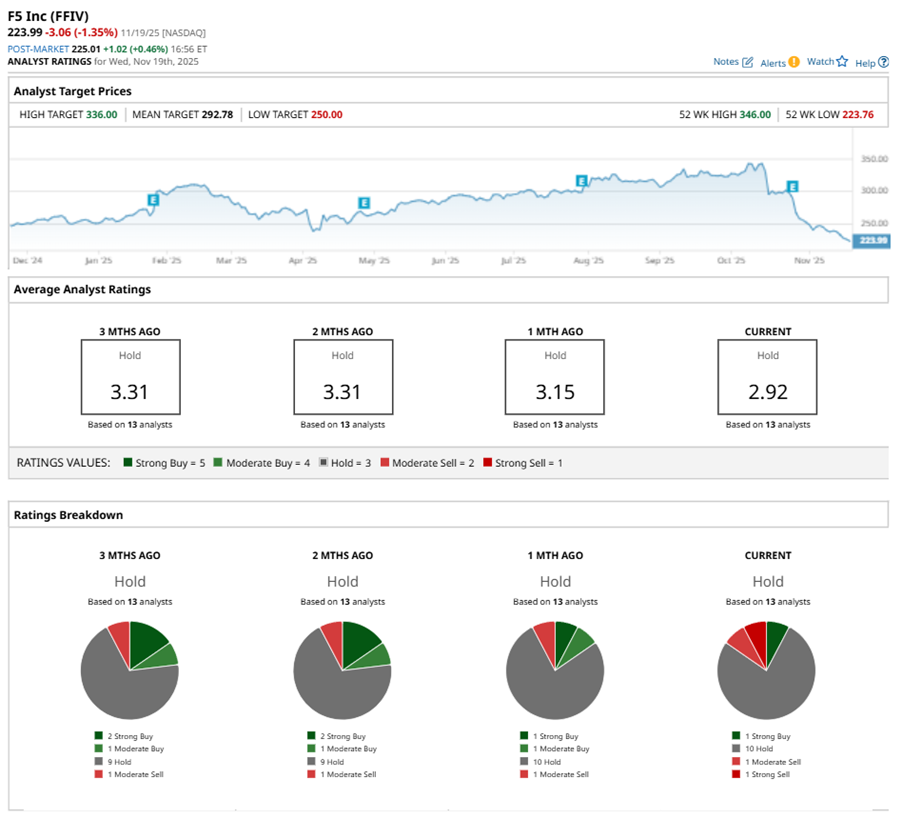

Among the 13 analysts covering FFIV stock, the consensus is a “Hold.” That’s based on one “Strong Buy” rating, 10 “Holds,” one “Moderate Sell,” and one “Strong Sell.”

This configuration is less bullish than a month ago, with one analyst suggesting a “Moderate Buy.”

On Oct. 28, Evercore ISI analyst Amit Daryanani kept an “In Line” rating on FFIV and lowered the price target to $280, implying a potential upside of 25% from current levels.

The mean price target of $292.78 represents a 30.7% premium to FFIV’s current price levels. The Street-high price target of $336 suggests a notable upside potential of 50%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Salesforce%20Inc%20HQ%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)