/Republic%20Services%2C%20Inc_%20HQ%20photo-by%20JHVEPhoto%20via%20Shutterstock.jpg)

Phoenix-based Republic Services, Inc. (RSG) offers environmental services in the U.S. and Canada. With a market cap of $69 billion, Republic Services operates as the second largest provider of non-hazardous solid waste collection, transfer, disposal, recycling, and energy services in the U.S.

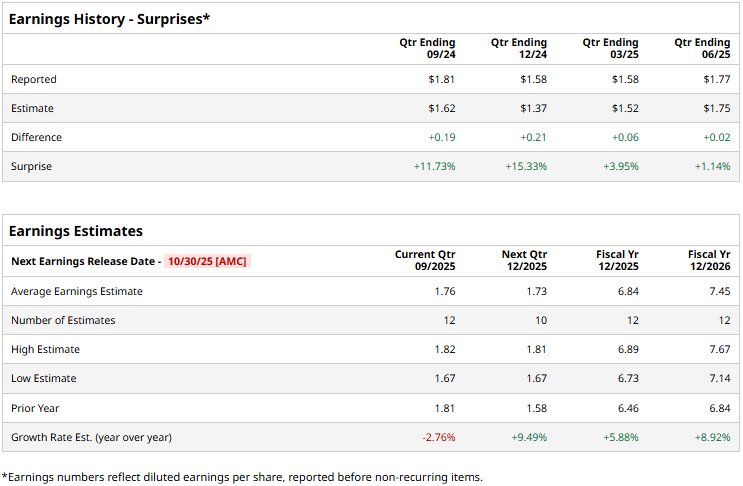

The waste management giant is set to unveil its third-quarter results after the market closes on Thursday, Oct. 30. Ahead of the event, analysts expect Republic Services to report an adjusted profit of $1.76 per share, down 2.8% from $1.81 per share reported in the year-ago quarter. On a positive note, the company has a robust earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters.

For the full fiscal 2025, analysts expect Republic Services to report an adjusted EPS of $6.84, up 5.9% from $6.46 in fiscal 2024. In fiscal 2026, its adjusted earnings are expected to grow 8.9% year-over-year to $7.45 per share.

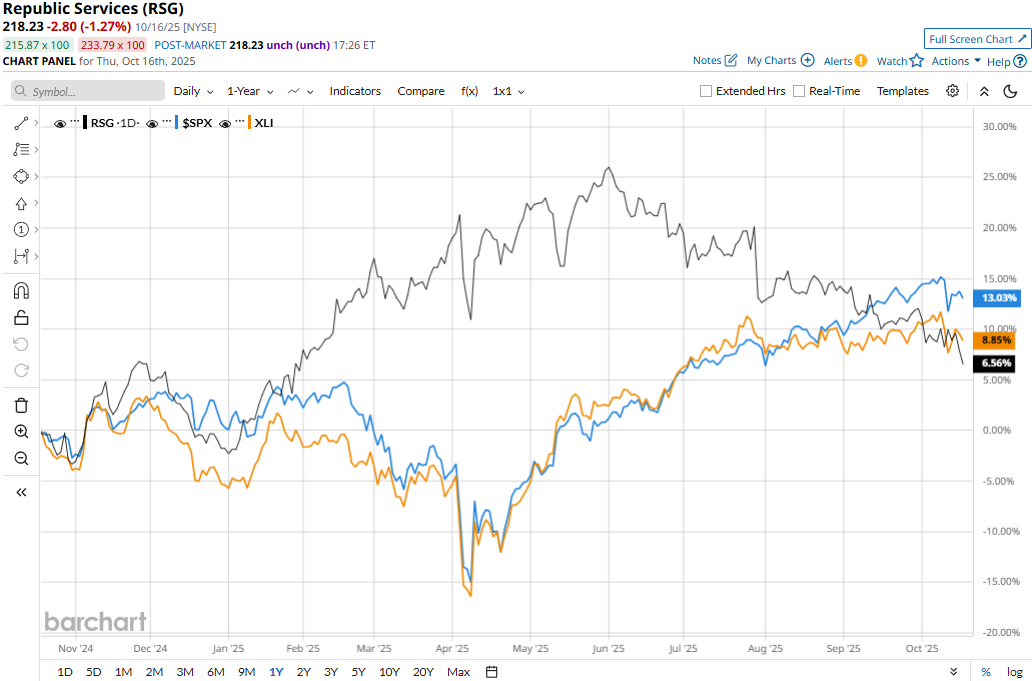

RSG stock prices have inched up 6.2% over the past 52 weeks, notably lagging behind the Industrial Select Sector SPDR Fund’s (XLI) 8.9% gains and the S&P 500 Index’s ($SPX) 13.5% returns during the same time frame.

Republic Services’ stock prices declined 5.8% in the trading session following the release of its mixed Q2 results on Jul. 29. Driven by 3.1% growth in organic revenues and 1.5% growth in acquisition-led revenues, the company’s overall topline for the quarter grew 4.6% year-over-year to $4.2 billion. However, this configuration missed the Street expectations by 75 bps. Meanwhile, its adjusted EPS for the quarter surged 9.9% year-over-year to $1.77, exceeding the consensus estimates by 1.1%. On an even more positive note, Republic Services’ operating cash flows for the quarter increased 11.7% year-over-year to $2.1 billion.

Analysts remain optimistic about the stock’s prospects. Republic Services has a consensus “Moderate Buy” rating overall. Of the 24 analysts covering the stock, opinions include 12 “Strong Buys,” two “Moderate Buys,” and 10 “Holds.” RSG’s mean price target of $262 suggests a 20.1% upside potential from current price levels.

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)