/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

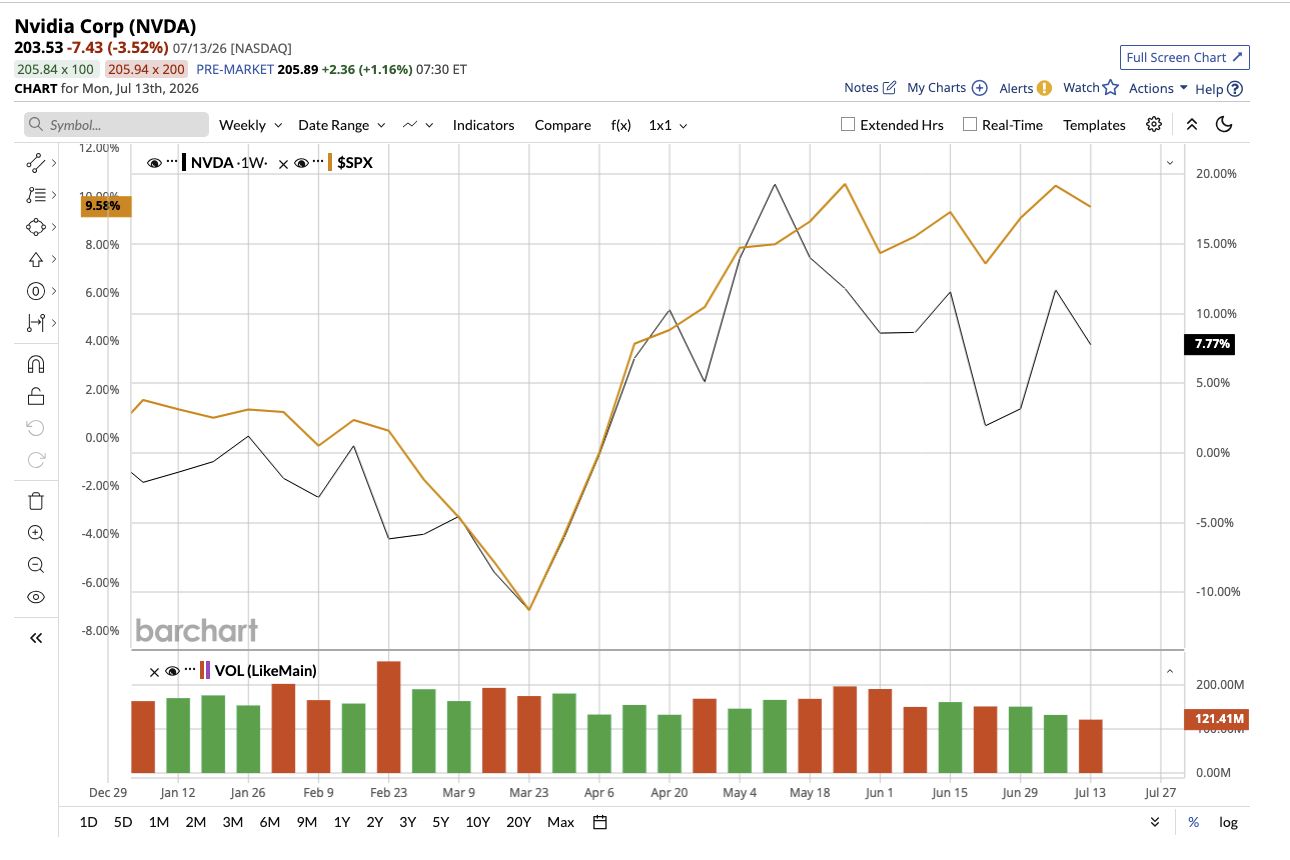

Ever since the artificial intelligence (AI) boom began, Nvidia (NVDA) has remained the undisputed king of semiconductors, delivering a jaw-dropping 980% return over the last five years. However, memory stocks seem to have overshadowed the AI chip giant this year, with AI infrastructure stocks stealing the spotlight. NVDA stock has gained just 11% year-to-date (YTD), trailing the explosive rallies in companies like Micron (MU) and Sandisk (SNDK). But don’t mistake the slow rally in Nvidia for slower business momentum.

If anything, Nvidia’s booming AI business is one of the key reasons why memory makers have been outperforming this year. Wall Street believes Nvidia's biggest growth story is still unfolding, with one bullish analyst projecting that NVDA stock could climb all the way to $500 per share. That's roughly 140% potential upside from current levels.

Nvidia’s AI Leadership Remains Unshaken

Ironically, Nvidia’s Hopper and Blackwell AI GPUs require massive amounts of high-bandwidth memory (HBM). Nvidia uses HBM memory from both SK Hynix (SKHYV) and Micron. In particular, South Korean memory giant SK Hynix — which made its U.S. stock market debut last week — is Nvidia’s key supplier.

According to Nvidia, the next-generation Rubin will deliver up to 35 times more inference throughput than Blackwell, which will require even more advanced memory systems. Nvidia’s GPU business is expanding at such an extraordinary pace that it is pulling the entire HBM industry along with it. In the first quarter of fiscal 2027, Nvidia's Data Center revenue surged 92% year-over-year (YOY) to $75 billion, fueled by strong Blackwell demand as customers deployed hundreds of thousands of GPUs in what became the fastest product rollout in the company's history.

Nvidia’s total revenue increased 85% YOY to $82 billion in Q1, marking its 14th-straight quarter of sequential revenue growth. Adjusted gross margin reached 75%, remaining remarkably stable despite the rapid production ramp of Blackwell systems.

Nvidia Is Opening Massive New Markets Beyond GPUs

It’s not just GPUs that strengthen Nvidia’s bull case. Management believes that its latest CPU roadmap has the potential to create an altogether new revenue stream.

Recently, Nvidia introduced Vera, a custom Arm-based CPU designed specifically for agentic AI. When combined with Rubin GPUs and NVLink technology, Vera is predicted to give up to “1.5x faster performance per core, 2x performance per watt, and 4x density per rack.” The company plans to begin production shipment of Vera Rubin in Q3 of this calendar year. Nvidia estimates that Vera will open an entirely new $200 billion total addressable market (TAM), and believes that it will generate nearly $20 billion of CPU revenue this year, positioning itself to become a major player in the server CPU market.

Aside from data centers, Nvidia's Edge Computing platform generated $6.4 billion in revenue, a 29% YOY increase led by robust Blackwell workstation demand. At the same time, sovereign AI revenue climbed more than 80% YOY. The company now claims that its AI infrastructure is “deployed across nearly 40 countries, representing $50 trillion in GDP.”

Meanwhile, Nvidia's physical AI business has generated more than $9 billion in revenue over the past 12 months. Additionally, its partnership with Uber (UBER) is expected to help power robotaxi fleets across nearly 30 cities on four continents by 2028. Besides Uber, many other robotic companies spanning industrial automation, surgical systems, and humanoid robots — such as Intuitive Surgical (ISRG), Siemens (SIEGY), and Agility Robotics — continue to use Nvidia's technology.

Finally, Nvidia pointed to the remarkable business momentum of hyperscalers like OpenAI, Anthropic, SpaceX's (SPCX) xAI, Meta Platforms (META), Alphabet (GOOGL), Microsoft (MSFT), and Oracle (ORCL). Analysts now expect these companies to collectively spend over $1 trillion in capital expenditures in 2027. Every new model these firms train and deploy will require more AI chips, more servers, more networking equipment, and larger data centers, while Nvidia supplies much of this infrastructure through its Blackwell GPUs and networking products. Nvidia even believes that annual AI infrastructure spending could eventually reach between $3 trillion and $4 trillion by the end of the decade.

What Does Wall Street Think of Nvidia Stock?

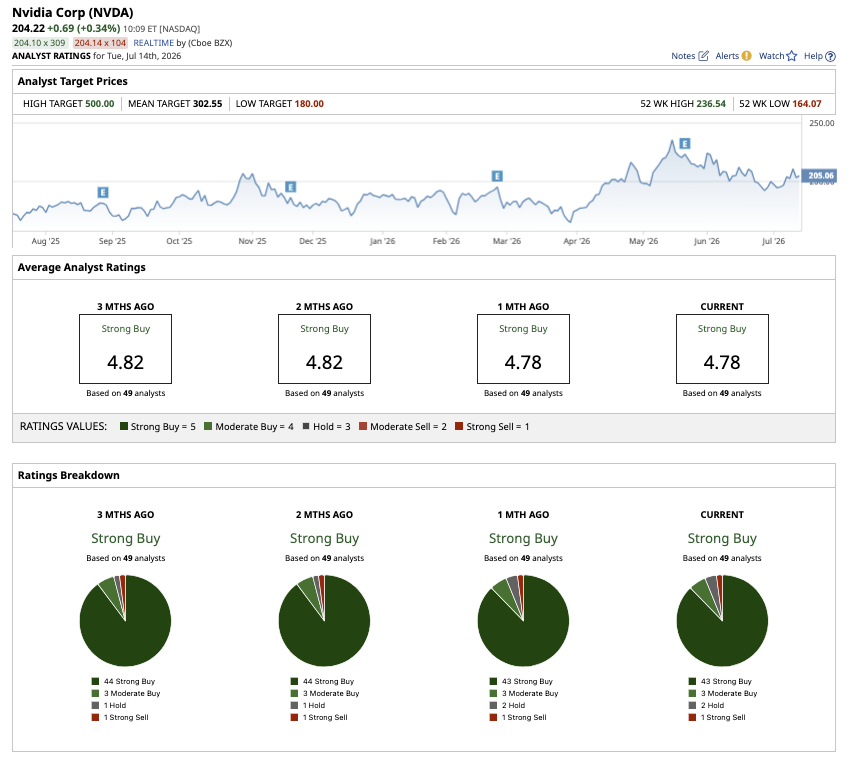

Rising hyperscale capex means more business for Nvidia — and explains why Wall Street believes Nvidia's growth can continue for many years, not just the next few quarters. Despite Nvidia's trillion-dollar AI opportunity, NVDA stock isn't expensive because analysts expect profits to grow almost as fast as revenue. Notably, analysts predict earnings to increase by 92% in fiscal 2027 and 36% in the following fiscal year. Currently, NVDA stock is valued at 23 times forward earnings. This is one of the main reasons why Baird holds the Street's most bullish estimate of $500 for Nvidia stock with an “Outperform” rating. If projections materialize, Nvidia's growth runaway could be exceptionally long.

Overall, on Wall Street, Nvidia stock holds a consensus “Strong Buy” rating. Of the 49 analysts covering the stock, 43 have a “Strong Buy” rating, three analysts have a “Moderate Buy,” two recommend a “Hold” rating, and one analyst suggests a “Strong Sell.”

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)