/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

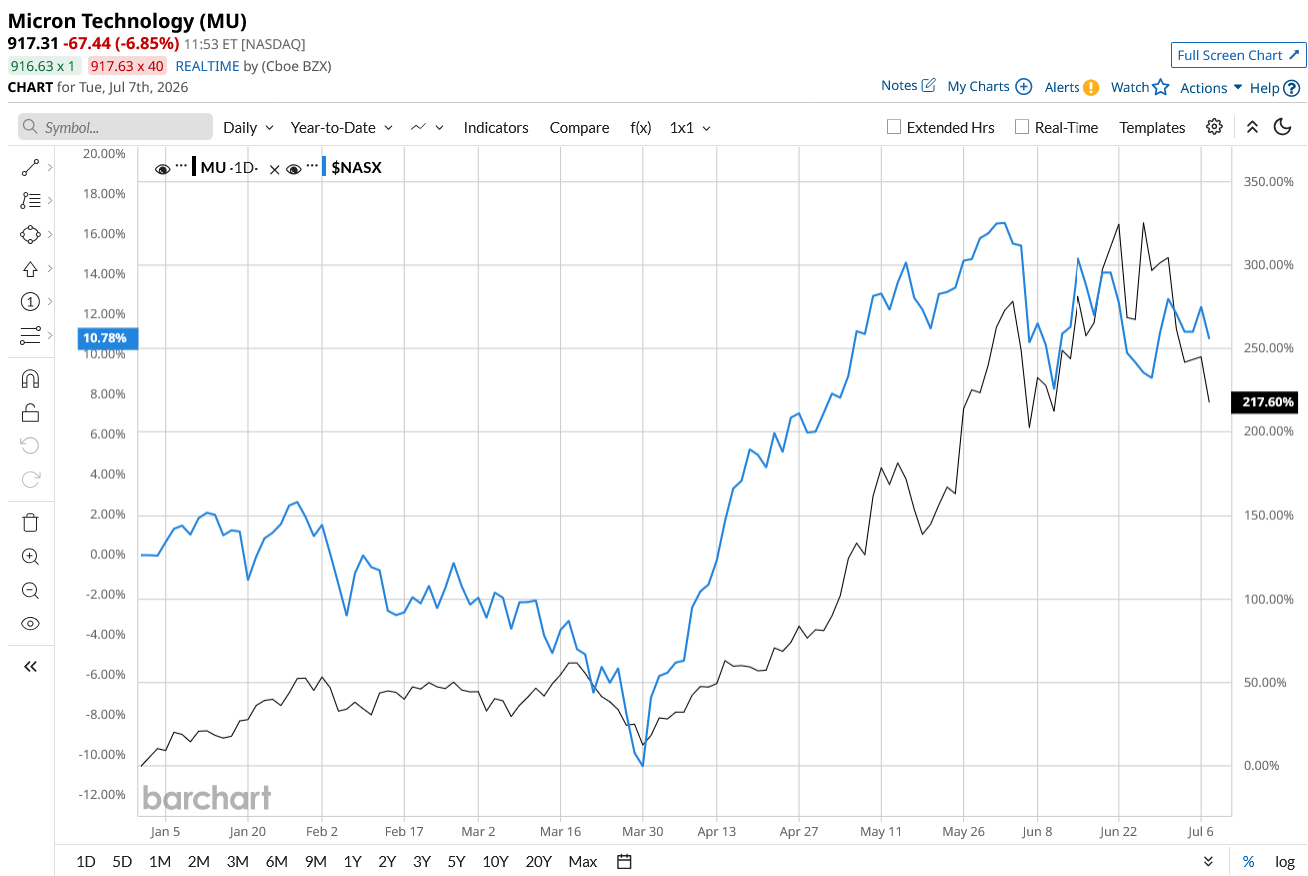

Despite an enormous gain of 220% so far this year, and some volatility today, Micron Technology (MU) stock's rally is far from over. Bulls argue that its AI-driven growth story is still in its early stages. Micron has received a new high price estimate on the Street. Melius Research analyst Ben Reitzes believes the stock can reach $2,200, which implies a potential upside of over 140%. This optimism comes after Micron posted a blockbuster quarter, showing that memory is no longer just a cyclical business.

AI Demand Has Made Memory More Than Cyclical

Micron is best known for designing and manufacturing memory and storage chips used in everything from AI servers and data centers to PCs, smartphones, cars, and industrial equipment. Its superior products, including DRAM, NAND flash memory, High Bandwidth Memory (HBM), and Solid-State Drives (SSDs), have made it a key supplier to the AI industry.

The global AI infrastructure buildout has become a major catalyst for memory demand. This led to a massive 346% year-over-year (YoY) surge in Micron’s revenue to $41.5 billion in fiscal third-quarter 2026. This single quarter's revenue outpaced Micron’s full-year fiscal 2025 revenue of $37.4 billion, revealing just how powerful the memory market has become. Micron’s bottom line grew just as dramatically as its top line. Adjusted diluted earnings per share (EPS) climbed 106% YoY to $25.11, significantly higher than fiscal 2025 adjusted EPS of $8.29. Adjusted gross margin also expanded to 85%, thanks to higher pricing, a better product mix, and increased contributions from premium AI memory products.

One of the biggest reasons analysts remain optimistic is Micron's leadership in HBM, which is a specialized type of DRAM designed to deliver the enormous bandwidth required by AI accelerators from companies such as Nvidia (NVDA) and AMD (AMD). HBM commands significantly higher selling prices, as the advanced AI processors now require ultra-fast memory to maximize performance. HBM is likely to remain one of the fastest-growing segments of the semiconductor industry for the next few years, giving Micron a significant edge. Overall DRAM revenue increased 343% YoY to $33.1 billion, accounting for 76% of total company revenue. Meanwhile, NAND revenue reached $13.8 billion, increasing 87% YoY. Essentially, one announcement made by management during the earnings call may have provided investors and analysts more reasons to believe Micron's long-term growth story.

Micron disclosed that it has signed 16 supply agreements (SCAs) with customers worldwide. These agreements collectively account for 200 terawatt-hours (TWh) of demand for memory products. They also carry three-year terms and include price renegotiation clauses every quarter, which gives Micron better revenue visibility. Importantly, 14 of the 16 signed agreements are expected to generate at least $100 billion in revenue at the minimum contract price over the remainder of the agreements. This level of committed business is highly unusual in the memory industry, which is considered cyclical. This proved to analysts and investors that AI demand will remain exceptionally strong and keep boosting the memory industry.

Why Analysts Believe the Rally Isn't Done Yet

Not just Melius Research, but many other analysts, boosted their target prices for MU stock, believing the business still has significant upside. For instance, Barclays analyst Tom O'Malley raised the price target to $2,000 from $1,175, while reiterating an “Overweight” rating. The analyst cited Micron's 16 long-term customer agreements as a significant driver of long-term revenue growth, while persistent supply-demand imbalances in the memory market could continue driving the stock higher.

Likewise, Cantor Fitzgerald analyst also raised the price target to $2,000 while maintaining an “Overweight” rating. The firm believes these long-term contracts signal a more durable memory upcycle than in previous cycles. This could lead to more stable profitability and less cyclical volatility for Micron than the memory industry has historically experienced.

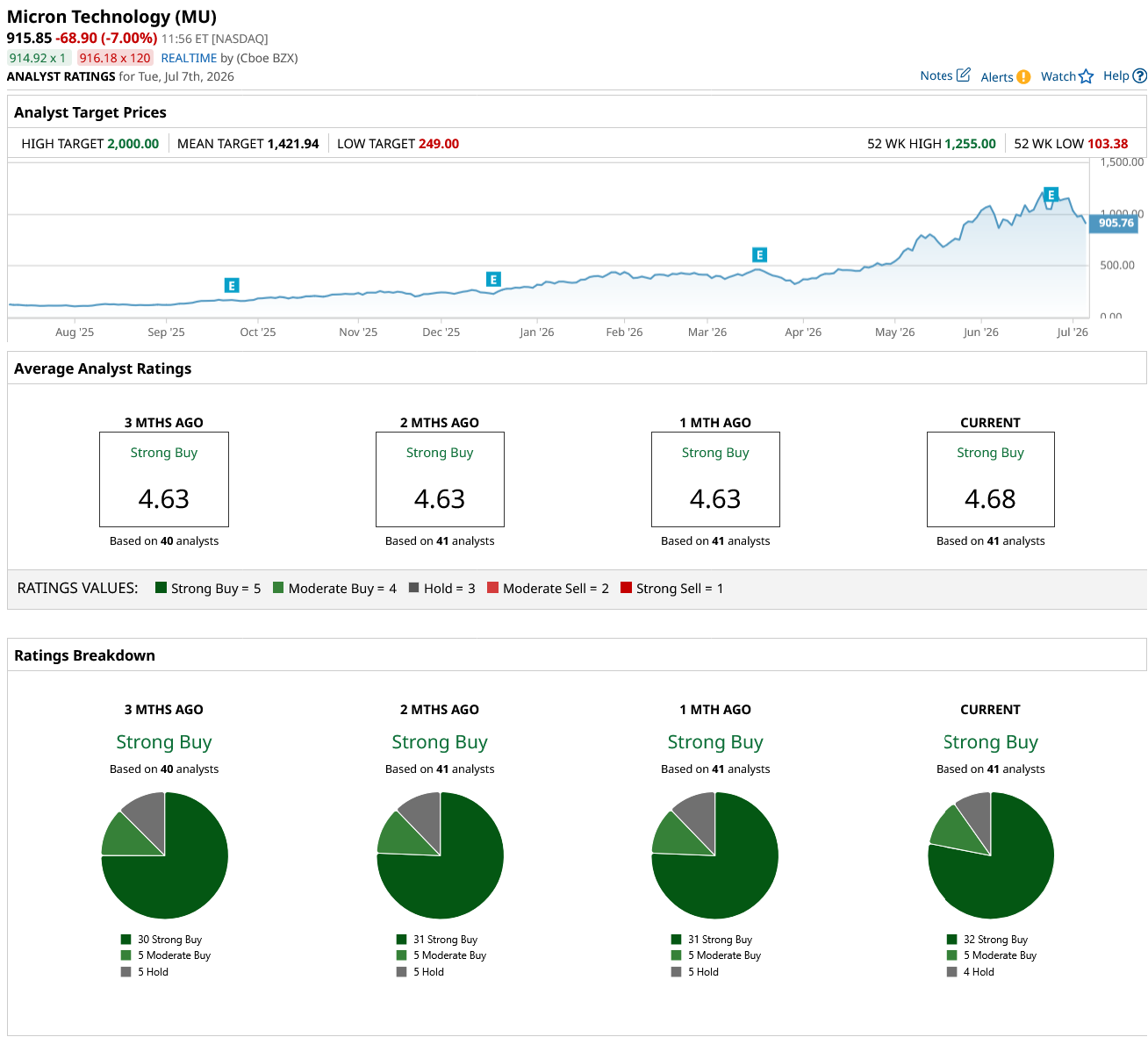

Similarly, Phillip Securities, DBS, Raymond James, Deutsche Bank, Morgan Stanley, and many others raised the target price for MU. The stock now holds an average target price of $1,421.94, which implies an upside potential of 55% from current levels. Overall, Wall Street holds a consensus “Strong Buy” rating for MU stock. Out of the 41 analysts covering MU, 32 rate it a “Strong Buy,” five rate it a “Moderate Buy,” and four recommend a “Hold.” It is important to note that Barchart's analyst page does not yet reflect the new $2,200 price target, so the average target price is certainly higher.

The reason for this bullishness is clear. First, AI infrastructure spending continues to accelerate globally as cloud providers race to build next-generation AI data centers. Second, Micron is enjoying the benefits of a supply-constrained market. Finally, these long-term agreements have reduced some of the earnings volatility associated earlier with memory stocks. Analysts now estimate Micron’s earnings to increase by 784.5% in fiscal 2026 to $73.32, before climbing another 104% to $149.64 per share in fiscal 2027.

Is the Bull Case of $2200 Realistic for MU Stock?

While the $2,200 bull case might seem unrealistic for any other average-performing AI company, it appears to be highly attainable for Micron stock. Its Q1 print revealed that the AI memory boom still appears to have significant room to run, and Micron has found a way to make memory less cyclical.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)