/Semiconductor%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Infrastructure spending related to artificial intelligence (AI) has emerged as one of the key drivers of the semiconductor industry, but investors have become increasingly skeptical as to whether the surge in investments can be sustainable for a relatively long time horizon. However, the conversation changed earlier this month when Applied Materials (AMAT) CEO Gary Dickerson shared his view on the matter. Dickerson noted that customers are now supporting forecasts of equipment demand for several years ahead.

These remarks helped boost semiconductor equipment stocks, with AMAT stock rising alongside shares of Lam Research (LRCX) and ASML (ASML). Moreover, the remarks came amid industry projections predicting extraordinary growth. According to World Semiconductor Trade Statistics, the total semiconductor market is expected to cross $1.5 trillion in 2026 and reach $1.9 trillion in 2027, which will mostly be driven by explosive demand for AI infrastructure, high-bandwidth memory (HBM), and advanced computing platforms.

About Applied Materials Stock

Applied Materials is a leading provider of semiconductor manufacturing equipment. The company offers deposition, etch, inspection, metrology, and advanced packaging products used by chip manufacturers like Taiwan Semiconductor (TSM), Samsung, Intel (INTC), Micron (MU), and SK Hynix. Based in Santa Clara, California, Applied Materials has a market capitalization of $473 billion and is one of the most critical players for almost all major transitions in semiconductor manufacturing technology.

AMAT stock has been one of the best performers among semiconductor equipment stocks over the past year. Shares have gained roughly 260% from the 52-week low despite still being roughly 30% away from the 52-week high of $739.67. Although AMAT has consolidated after an outstanding rise, the stock continues to outperform the broader market as investors realize that Applied Materials is one of the main beneficiaries of the AI infrastructure cycle.

In terms of valuation, AMAT stock trades at 47.4 times forward earnings and 16.1 times sales. These multiples look expensive in comparison with the historical averages for semiconductor equipment companies. At the same time, they already take into account the prospect of continued above-cycle growth.

In contrast to previous semiconductor cycles, which were mostly driven by consumer electronics, the current spending wave is supported by AI data centers, advanced logic manufacturing, HBM, and advanced packaging — areas where Applied Materials has leading technology positions. If management's expectations concerning a prolonged investment cycle turn out to be correct, AMAT stock's current valuation will start to make sense.

Applied Materials Beats on Earnings

Applied Materials delivered another record performance for the second quarter of fiscal 2026. Revenue jumped 11% year-over-year (YOY) to a record $7.91 billion, while GAAP EPS grew 33% YOY to $3.51. Non-GAAP EPS reached $2.86, up 20% YOY, due to continued operating leverage amid accelerating AI demand across multiple products.

However, perhaps the most important update had to do with expectations. Gary Dickerson said that the company expects its semiconductor equipment division to grow by more than 30% in calendar-year 2026 due to acceleration of investments in leading edge logic, DRAM manufacturing, and advanced packaging. Furthermore, the company highlighted that revenue from advanced packaging equipment is expected to increase by 50% this year since AI chips require more complex manufacturing processes.

The CEO's recent comments to Nikkei Asia seem to confirm the above outlook. Dickerson noted that the company's largest customers provide the forecast for equipment demand for at least eight quarters ahead, and directional forecasts for roughly three years into the future. At the same time, management has also pointed out that fast-growing infrastructure for AI computing is only in its initial stages.

Applied Materials also continues investing beyond manufacturing capacity. In Q2, the company announced new partnerships via the EPIC Center aimed at commercialization of next-generation semiconductor technology, while simultaneously increasing its inventory, production planning, and logistics capacity in order to support customer growth.

What Do Analysts Expect for Applied Materials Stock?

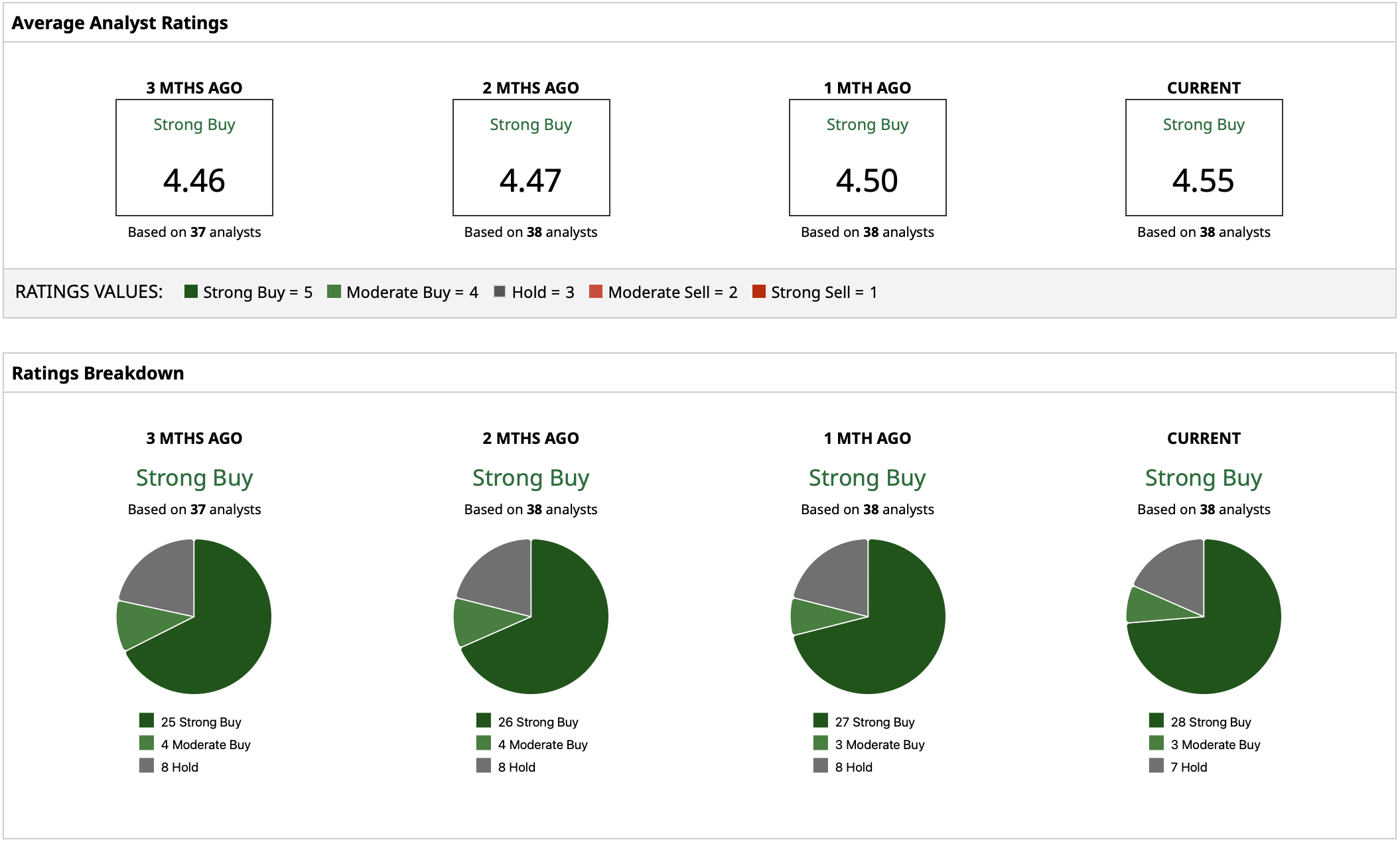

Wall Street analysts assign a consensus “Strong Buy” rating to AMAT stock and have been gradually increasing earnings estimates over the past quarters, but recent comments from management regarding multiyear customer visibility could help raise long-term forecasts further. Currently, the mean price target stands at $631.44, while the high price target is $900 per share. Considering the current share price near $570, the mean target represents potential upside of 11% from here while the high target suggests potential upside of 58%. The wide discrepancy between the consensus target for AMAT stock and the $900 high target reflects that some analysts see significant potential for upside if AI-related semiconductor investment turns out to be more durable than expected.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)