/Person%20holding%20cellphone%20with%20webpage%20of%20US%20security%20equipment%20company%20Axon%20Enterprise%20Inc_%20on%20screen%20with%20logo%20By%20Timon.jpeg)

With a market cap of $45.6 billion, Axon Enterprise, Inc. (AXON) is a global public safety technology company dedicated to protecting more lives through connected hardware, software, and AI-powered solutions. It serves law enforcement, public safety agencies, enterprises, and governments with an integrated ecosystem designed to improve safety and operational effectiveness.

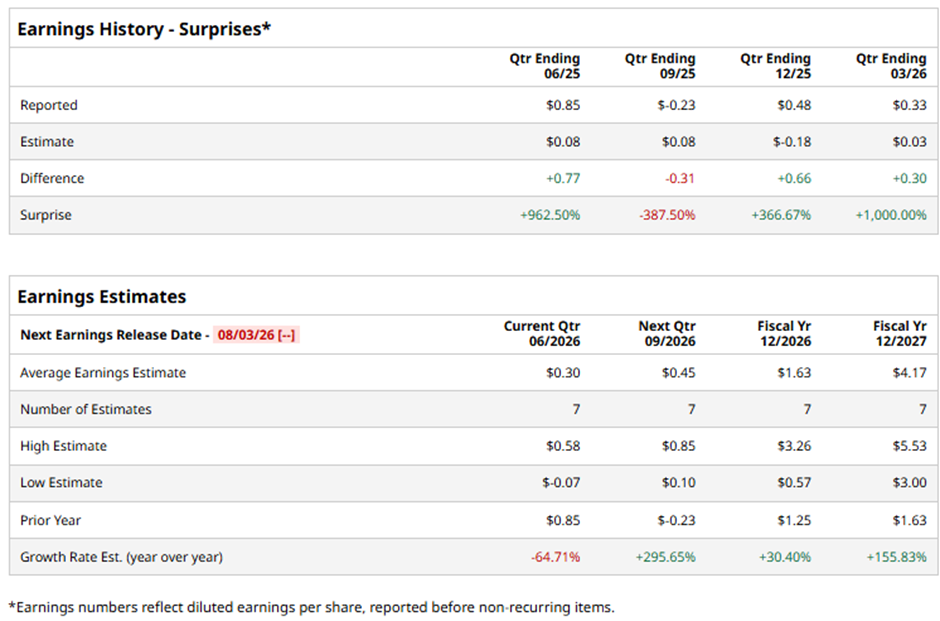

The Scottsdale, Arizona-based company is expected to release its fiscal Q2 2026 results soon. Ahead of this event, analysts project AXON to report an EPS of $0.30, a 64.7% decline from $0.85 in the year-ago quarter. The company has exceeded Wall Street's bottom-line estimates in three of the last four quarters while missing on another occasion.

For fiscal 2026, analysts forecast Axon Enterprise to post EPS of $1.63, up 30.4% from $1.25 in fiscal 2025. Moreover, EPS is projected to surge 155.8% year-over-year to $4.17 in fiscal 2027.

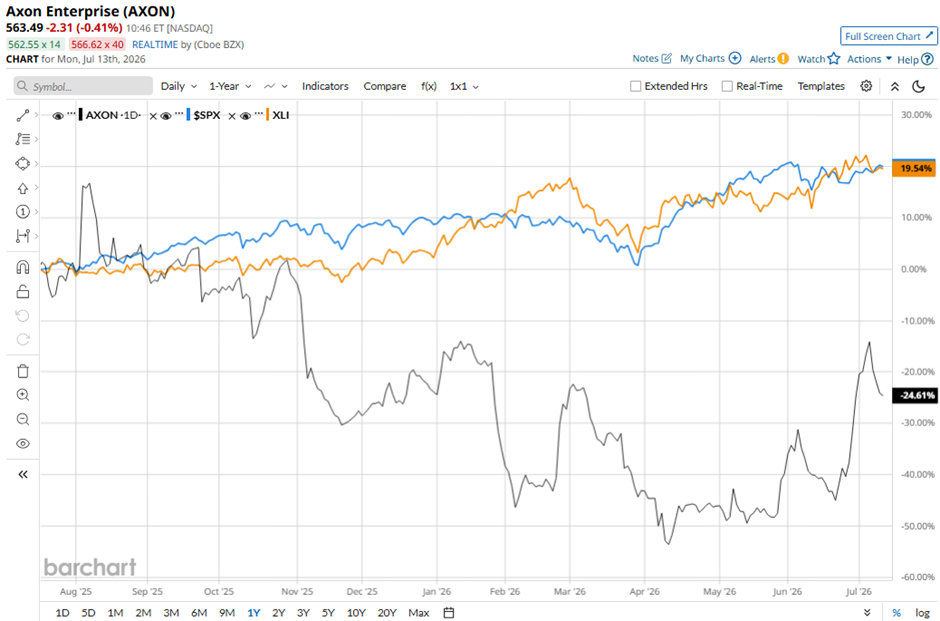

AXON stock has decreased 22.5% over the past 52 weeks, lagging behind the broader S&P 500 Index's ($SPX) 20.8% return and the State Street Industrial Select Sector SPDR ETF's (XLI) 20.9% gain over the same period.

Shares of Axon Enterprise climbed 10.6% following its Q1 2026 results on May 6 as the company reported record quarterly revenue of $807 million, up 34% year-over-year, marking its ninth consecutive quarter of 30%+ growth, driven by strong demand for TASER 10, Axon Body 4, AI products, and counter-drone solutions. Investors were encouraged by Software & Services revenue rising 35% to $355 million, AI-related product revenue surging more than 700% year over year, counter-drone revenue jumping over 300%, and annual recurring revenue reaching $1.5 billion, up 35%, highlighting accelerating adoption across Axon’s ecosystem.

The rally was further supported by Axon raising its full-year 2026 revenue growth outlook to 30% - 32%, while maintaining a strong 25.5% adjusted EBITDA margin forecast and reporting net income of $169 million with adjusted EBITDA of $202 million.

Analysts' consensus view on AXON stock is bullish, with an overall "Strong Buy" rating. Among 20 analysts covering the stock, 15 suggest a "Strong Buy," four give a "Moderate Buy," and one provides a "Hold" rating. The average analyst price target is $677.63, suggesting a potential upside of 20.3% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)