/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

Intel (INTC) has been working hard to rebuild its position as one of the world’s leading chipmakers. The company has made encouraging progress in artificial intelligence (AI), advanced chip manufacturing, and its foundry business, but investors are still looking for clear signs that major customers believe in its technology. Sometimes, those signals come from the most unexpected places.

One such signal may have arrived with the departure of Intel veteran Gary Jiang, who spent 18 years at the company before recently joining Tesla’s (TSLA) Terafab semiconductor project in Austin, Texas. While losing a long-time employee would normally raise concerns, Wall Street is viewing this move through a different lens.

Wedbush believes Jiang’s appointment — along with Tesla’s decision to use Intel’s upcoming 14A process for Terafab — reflects growing confidence in Intel’s next-generation chipmaking capabilities. If that confidence turns into a successful partnership, Intel may have said goodbye to a veteran employee while welcoming something even more important: a catalyst that could support the next phase of growth for INTC stock.

Let’s take a closer look.

About Intel Stock

Intel has been a cornerstone of the semiconductor industry for decades. Headquartered in Santa Clara, California, the company has a market capitalization of roughly $555 billion and remains a leading supplier of the chips powering personal computers, data centers, and AI infrastructure. Its broad portfolio includes client and server processors, graphics chips, system-on-chip (SoC) solutions, networking products, and a rapidly expanding foundry business that manufactures advanced semiconductors for third parties.

As AI reshapes the tech landscape, Intel is investing aggressively to regain its leadership through next-generation process nodes, AI-focused products, and contract chip manufacturing. While competition remains intense, Intel's improving execution and expanding opportunities have strengthened investor confidence, making it one of the semiconductor sector’s most closely watched turnaround stories.

Optimism has been clearly reflected in the remarkable performance of INTC stock. Rather than being driven by a single event, the rally has unfolded through a series of catalysts that have steadily strengthened the bullish narrative. The AI investment boom provided the initial spark, while U.S. government support for domestic semiconductor manufacturing reinforced confidence in Intel’s long-term strategy. Investor sentiment received another boost when SoftBank (SFTBY) and Nvidia (NVDA) threw their weight behind initiatives tied to Intel’s ecosystem, strengthening the view that Intel may once again emerge as a major force in both advanced processors and semiconductor manufacturing.

Momentum accelerated further after Intel reported a stronger-than-expected first-quarter earnings performance. Reports of Apple (AAPL) partnering with Intel’s foundry business, along with a string of higher price targets from firms like Bank of America and Cantor Fitzgerald, also added fresh fuel to the rally.

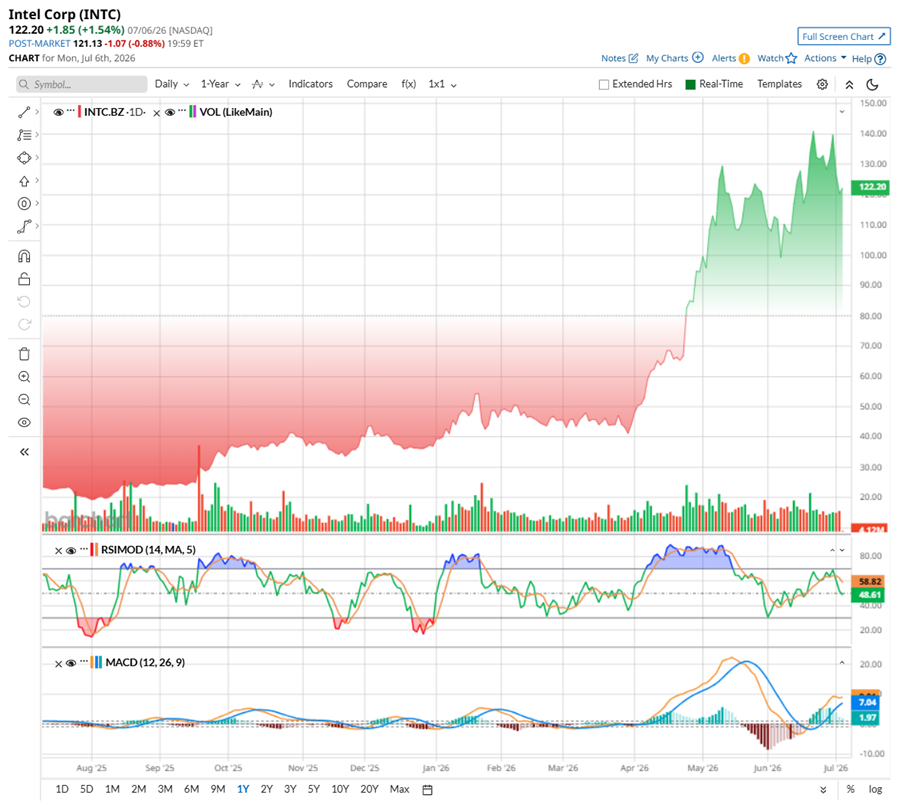

Shares have surged roughly 200% on a year-to-date (YTD) basis and are up 367% over the past 52 weeks. Since touching a 52-week low of $18.97, INTC stock has staged a remarkable 480% rebound. Last week, the stock climbed to a record high of $142.35 before retreating about 14%. Even after that pullback, Intel stock remains up by 87% over the last three months.

Still, the valuation remains demanding. INTC stock currently trades at 192 times forward earnings and 11.6 times sales, well above both the sector average and the company’s historical valuation. Such elevated pricing suggests that investors have already factored in a significant portion of Intel's expected turnaround and long-term AI-driven growth. While continued execution in its AI and foundry businesses could justify the premium, any slowdown in growth or operational setbacks may leave the stock vulnerable to a reset.

Intel Shares Rise After Strong Q1 Report

Intel started fiscal 2026 with a strong Q1 performance, delivering better-than-expected revenue and earnings. The encouraging results strengthened investor confidence, sending ITNC stock up almost 24% following the release. Revenue increased 7% year-over-year (YOY) to $13.6 billion, driven by solid execution across the company’s AI-focused operations and expanding manufacturing business. Meanwhile, adjusted EPS more than doubled YOY to $0.29, comfortably surpassing Wall Street’s expectations and marking another quarterly earnings beat.

Growth was led by Intel's Data Center and AI (DCAI) segment, where revenue surged 22% YOY to $5.1 billion, reflecting robust demand for AI infrastructure and enterprise computing solutions. Intel Foundry also maintained its positive trajectory, with revenue climbing 16% to $5.4 billion as the company continued to expand its contract chip manufacturing capabilities. The Client Computing Group, Intel’s largest business, posted a modest 1% increase to $7.7 billion. While demand remained stable, growth was constrained by ongoing supply limitations and a personal computer market that has yet to experience a broad-based recovery.

Cash generated from operating activities rose to $1.1 billion, up from $813 million, while cash and cash equivalents stood at $17.7 billion at quarter-end. This healthy liquidity provides Intel with substantial flexibility to support its long-term AI investments and foundry expansion.

Looking ahead, Intel provided an encouraging outlook for Q2, forecasting revenue of $13.8 billion to $14.8 billion and non-GAAP EPS of $0.20. The company is scheduled to report Q2 results on July 23, after the market closes, with investors watching closely for further evidence that the turnaround remains on track.

Meanwhile, analysts estimate Q2 revenue to be around $14.4 billion while EPS is expected to be $0.10. For fiscal 2026, EPS is anticipated to surge by 625% YOY to $0.63, before rising by another 54% YOY to $0.97 in fiscal 2027.

Why Wedbush Thinks This Veteran’s Departure Could Strengthen the Bull Case

Wedbush believes Jiang’s move to Terafab could ultimately work in Intel’s favor. While the company is losing an executive who spent years helping lead manufacturing operations, analyst Matt Bryson sees the appointment as an encouraging signal for Intel’s technology rather than a negative development.

Jiang is expected to lead the Terafab facility in Austin, Texas, which Tesla plans to build using Intel’s next-generation 14A manufacturing process. According to Bryson, the decision suggests growing confidence in Intel’s advanced process nodes and could become a meaningful long-term catalyst for the chipmaker.

That said, Bryson remains cautious about the project’s execution, noting that Terafab is based on a manufacturing process that is still being finalized and is intended to produce chips for products and markets that have yet to be fully defined. Even so, the partnership itself points to increasing industry confidence in Intel’s foundry ambitions, which could strengthen the long-term outlook for INTC stock.

What Do Analysts Expect for Intel Stock?

Last week, HSBC turned bullish on Intel, raising its price target to $200 from $100 while maintaining a “Buy” rating. The bank believes investors are still underestimating Intel’s growth potential, particularly in its server CPU and foundry businesses.

Analyst Frank Lee expects server CPU shipments to grow faster than previously forecast, supported by Intel’s decision to allocate more manufacturing capacity to high-demand server chips and the strong rollout of its 18A process technology. Lee also sees meaningful upside in Intel’s foundry business, as more companies look beyond Taiwan Semiconductor (TSM) for advanced chip manufacturing. He believes Intel’s Embedded Multi-die Interconnect Bridge (EMIB) packaging technology, along with growing interest from companies like Tesla, Apple, Alphabet (GOOGL), and Nvidia, could further strengthen the company’s long-term growth prospects.

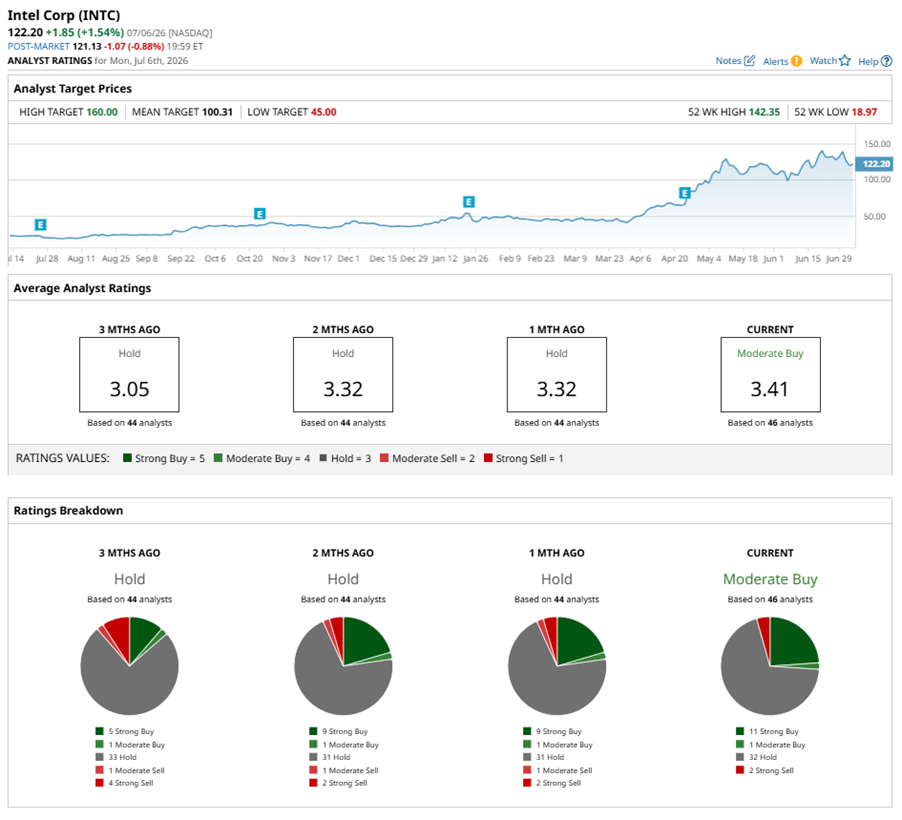

Wall Street is definitely starting to see Intel in a different light. Just a month ago, the stock had a consensus “Hold” rating, but it has since moved to a “Moderate Buy." Among the 46 analysts with coverage, 11 suggest a “Strong Buy" rating, one has a “Moderate Buy," 32 analysts recommend a “Hold,” and two have a “Strong Sell” rating. Intel's rally has moved faster than analyst price targets, with INTC stock already trading above the average price target of $102.87. Still, the Street-high target of $200 from HSBC suggests potential upside of 81% from current levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)