/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

For years, the artificial intelligence (AI) boom has been viewed through the lens of chipmakers racing to meet soaring demand. Now, Bank of America (BAC) is arguing that the opportunity may be even larger than Wall Street previously imagined. BofA’s analysts, led by Vivek Arya, increased the estimate for the global semiconductor market to a massive $2.7 trillion by 2030, fueled by relentless spending on AI data centers, stronger memory demand, and an expected recovery across automotive and industrial markets.

That outlook is leading analysts to expect the semiconductor industry to keep growing for years to come. BofA now sees semiconductor equipment spending accelerating well into the latter part of the decade, supported by expanding manufacturing capacity, long-term customer commitments, and tech advances that require increasingly complex chip production. The bank also highlighted improving momentum at major foundry players, including Intel Corporation (INTC), as the industry gears up for the next wave of AI-driven investment.

Against that backdrop, BofA raised price targets across several semiconductor names. Intel’s price target was raised from $135 to $160 – a new Street-high target. The upgrade certainly grabs attention, but can the company deliver on those lofty expectations?

About Intel Stock

Intel has long been one of the defining names in the semiconductor industry. Headquartered in Santa Clara, California, the chipmaker commands a market capitalization of roughly $667.8 billion and plays a central role in powering everything from personal computers to AI infrastructure.

Its portfolio spans client and server processors, graphics chips, system-on-chip (SoC) solutions, and a fast-growing foundry business that manufactures advanced semiconductors for third parties. As the AI race accelerates, Intel is working to reclaim its technological edge. While its opportunities are significant, the company's long-term success will ultimately depend on consistently executing its ambitious turnaround strategy.

Intel has turned into one of the market’s biggest comeback stories this year. The stock has not climbed on a single headline but has ridden a wave of catalysts that have kept investors coming back for more. The AI spending boom lit the initial spark, but the rally quickly gathered steam as Intel secured U.S. government backing, attracted support from SoftBank (SFTBY) and Nvidia (NVDA) and convinced more investors that it could once again become a serious player in both advanced CPUs and semiconductor manufacturing.

In addition to Intel’s blowout first-quarter results triggering a rally, reports of Apple’s (AAPL) foundry partnership with Intel and BofA’s raised price target gave bulls another reason to stay in the trade.

There were plenty of side stories that kept sentiment humming. A regulatory filing showed the spouse of former House Speaker Nancy Pelosi purchased 200 call options on Intel, catching the attention of retail traders.

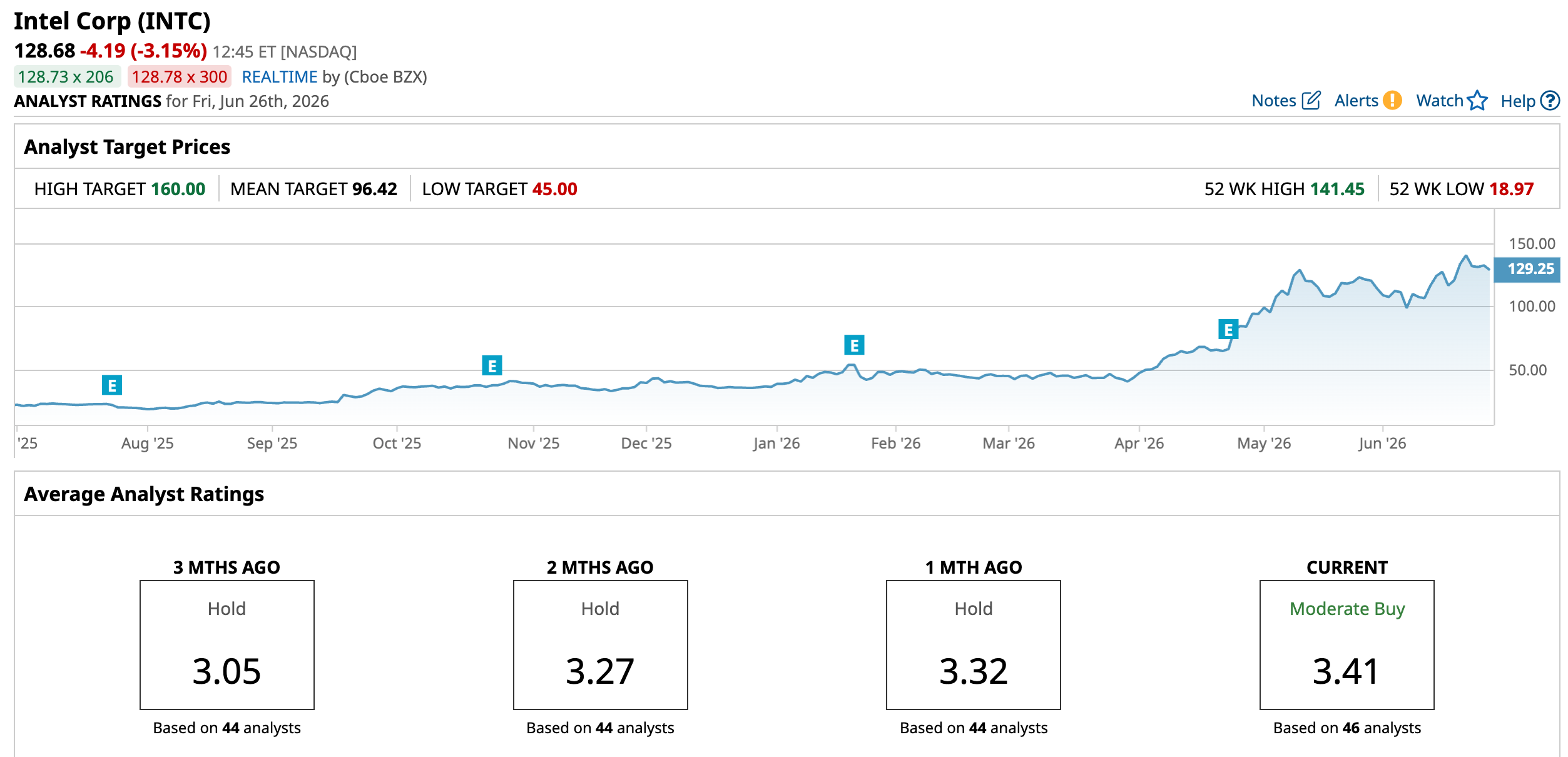

Intel’s shares are up 248% year-to-date (YTD) and beyond 470% over the past year. From the 52-week low of $18.97, INTC has staged an eye-popping 578% rebound. Earlier this week, Intel touched an all-time high of $141.45 before pulling back 8.8%. The stock is down 4.16% over the past five days, but up 3.97% over the past month, and an impressive 191.20% during the last three months.

Technically, the bulls still appear to have the upper hand. Intel’s 14-day RSI sits at 56.86, suggesting the stock has strong momentum without yet reaching deeply overbought territory. Meanwhile, the MACD oscillator flashes bullish signals, with the MACD line holding above the signal line and positive histogram bars indicating buyers are still calling the shots.

There is still one wrinkle investors can’t afford to ignore – Intel’s valuation is not exactly cheap. INTC is priced at 121.63 times forward adjusted earnings and 11.37 times forward sales. Those figures sit well above both sector peers and Intel’s own historical norms.

The market is betting on Intel’s future, leaving little room for missteps. If the AI and foundry push pays off, the premium makes sense. If not, the valuation could quickly look stretched.

Intel Sprints Higher After Strong Q1 Report

Intel began 2026 on a high note, posting a clean double beat on both revenue and earnings as signs of its turnaround continued to gain traction. Investors liked what they saw, and the stock rose 23.6% after its Q1 earnings results in April. Revenue for the quarter climbed 7% year-over-year (YOY) to $13.6 billion, powered by strong momentum in the company’s AI and manufacturing businesses. EPS more than doubled to $0.29, comfortably topping Wall Street’s expectations and marking Intel’s third straight quarterly earnings beat.

Data Center and AI segment revenue jumped 22% annually to $5.1 billion as demand for AI infrastructure remained strong. Intel’s Foundry business also continued to make progress, growing 16% to $5.4 billion. Additionally, the Client Computing Group – the company’s largest division – grew a modest 1% to $7.7 billion, weighed down by supply constraints and a PC market that’s still searching for its next growth catalyst.

Furthermore, Intel’s balance sheet showed improvement. Cash generated from operations rose to $1.1 billion from $813 million a year earlier, while the company finished the quarter with $17.7 billion in cash, giving Intel plenty of financial flexibility as it continues investing in its AI and foundry ambitions.

What added more fuel to the rally was Intel’s outlook for Q2. Sales for the quarter is expected to be between $13.8 billion and $14.8 billion, with non-GAAP EPS of about $0.20.

Meanwhile, analysts monitoring the company are bullish, estimating Q2 revenue at around $14.4 billion, and profit at $0.10 per share. For fiscal 2026, EPS is anticipated to surge impressively by 625% YOY to $0.63, before rising by another 54% annually to $0.97 in fiscal 2027.

What Do Analysts Expect for Intel Stock?

BofA analyst Vivek Arya is not just betting on today’s AI boom. He believes the investment cycle has much more room to run. The key reason is that spending on AI infrastructure is becoming increasingly visible well beyond the next couple of years, with customers continuing to commit capital through at least 2028.

Reflecting that confidence, Arya and his team raised their forecasts for wafer fabrication equipment (WFE) spending across the board. They now expect the spending to reach $190 billion in 2027, up from their previous estimate of $183 billion. The analysts also see it climbing to $250 billion in 2028, before rising further to $268 billion in 2029 and $292 billion in 2030, underscoring their belief that the AI-driven chip investment cycle still has plenty of runway.

According to Arya, several factors support that outlook. More semiconductor cleanroom capacity is expected to come online by 2028, giving manufacturers greater ability to expand production. Plus, long-term agreements in the memory market provide stronger demand visibility, while advances in chip technology continue to increase the amount of manufacturing equipment required for every wafer produced. Arya also pointed to customer and capacity progress at Intel and Samsung, along with the long-term potential of Terafab initiatives, as additional positives for advanced logic and foundry businesses.

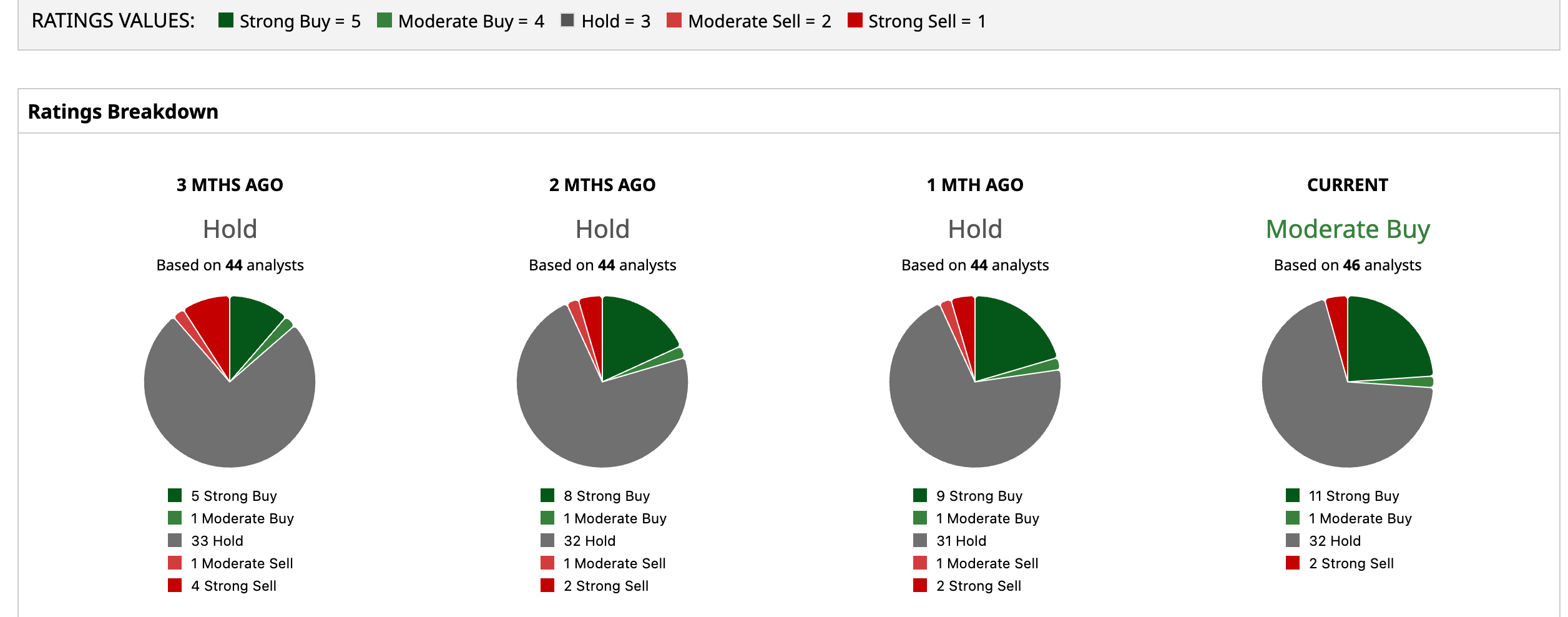

Wall Street has started changing its tune on Intel. The stock now carries a consensus “Moderate Buy” rating after climbing out of “Hold” territory just a month ago – a sign that analysts believe the company may finally be turning the corner. Among the 46 analysts in coverage, 11 suggest a “Strong Buy,” and one has a “Moderate Buy” rating. A majority of 32 analysts recommend a “Hold,” and the remaining two give a “Strong Sell” rating.

Intel has already run well ahead of the pack, with shares trading above the Street’s average price target of $96.42. Still, BofA’s Street-high target of $160 suggests roughly 24.34% upside potential if the AI story keeps gaining steam.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)