/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Micron Technology (MU) just delivered one of the strongest quarters in its history. As hyperscalers and enterprises continue investing heavily in artificial intelligence (AI) infrastructure, demand for memory chips has surged. At the same time, supply remains constrained across the industry, which is pushing DRAM and NAND pricing higher. This combination is driving explosive growth in Micron's revenue, margins, and earnings.

Besides solid demand and high pricing, Micron’s bull case is supported by its strategic customer agreements (SCAs). Micron has been securing long-term customer agreements that lock in favorable pricing for years and improve visibility into future earnings. The agreements indicate that current profitability is much more sustainable than previous memory cycles.

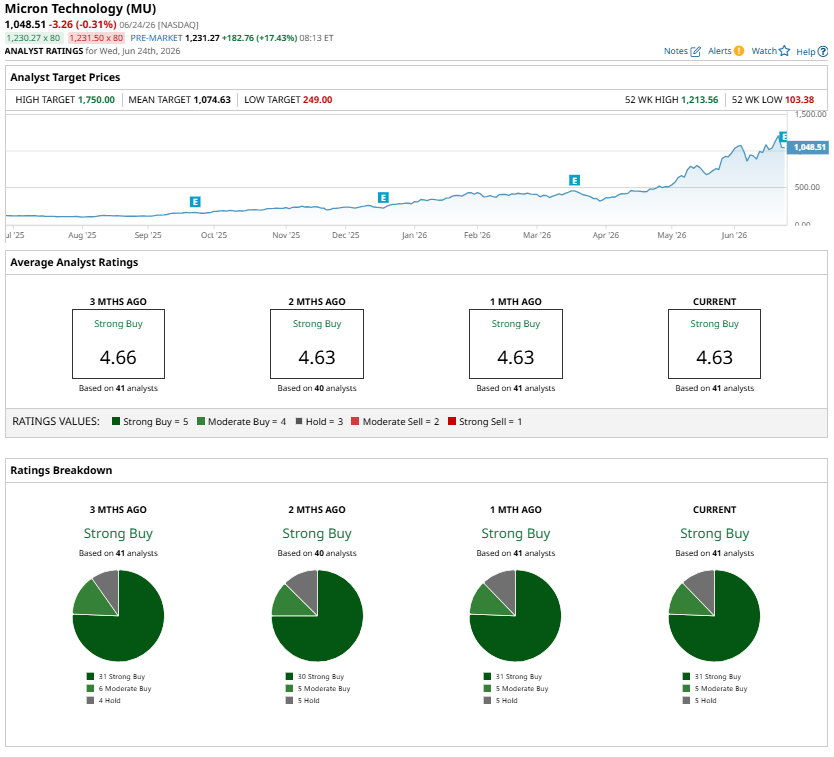

Thanks to Micron’s solid growth prospects, at least one analyst believes Micron could hit $1,750 per share, the Street’s highest price target, implying about 44% potential upside from current levels.

Breaking Down Micron's Q3 Results

Micron delivered a strong fiscal third quarter, driven by robust demand and favorable pricing across its memory portfolio. Revenue reached $41.5 billion, representing a 346% year-over-year (YOY) increase. The company also recorded a sequential revenue increase of $17.6 billion, the largest quarterly jump in its history.

The impressive growth was fueled by higher customer demand for both DRAM and NAND products. Memory pricing remained the key driver, supported by tight industry supply conditions and a more favorable product mix.

DRAM remained Micron’s largest business, accounting for roughly three-quarters of total revenue. The segment benefited from significant price increases and sustained demand for high-bandwidth memory (HBM), a critical component in AI accelerators and data-center infrastructure.

NAND also achieved record results, with average selling prices rising and market conditions improving across storage products.

Profitability improved substantially as well. Higher memory prices translated into significantly stronger margins, while disciplined operational execution and a favorable product mix further boosted earnings. As a result, adjusted EPS climbed sharply to $25.11, compared with $1.91 in the same quarter last year.

Micron’s SCAs Support Further Upside

Micron’s recently signed SCAs represent a major change in how the company operates and significantly improve Micron’s earnings visibility. Micron reported 16 signed multi-year agreements during the quarter. These contracts cover about 20% of Micron’s DRAM volume and one-third of its NAND volume through 2030, with management expecting more than half of future revenue to eventually be covered by similar arrangements.

The significance of SCAs is in the contract structure. Most SCAs are take-or-pay agreements that require customers to purchase committed volumes, reducing demand uncertainty. Many of the agreements also include pricing floors and ceilings, which help protect the company from sharp price declines while still allowing it to maintain attractive profitability. According to management, the pricing floors embedded in these contracts support gross margins that are comfortably above the highest quarterly margins Micron achieved in previous industry cycles.

The financial implications are substantial. Reportedly, 14 of the signed agreements carry roughly $100 billion of minimum contracted revenue. Beyond strengthening cash flow visibility, the agreements enhance supply assurance for customers during a period of tight memory availability. Collectively, these SCAs reduce cyclicality, improve margin stability, and support the case for higher long-term earnings and valuation multiples for Micron.

Micron to Deliver Solid Growth Ahead

Micron is well-positioned to deliver strong growth in the coming years. While demand from data centers remains a major driver, growth is increasingly supported by AI-powered features in consumer devices and applications across the automotive, industrial, and robotics sectors. Emerging technologies such as humanoid robots and autonomous vehicles could further expand demand for memory and storage.

Overall, Micron’s business momentum is expected to remain strong, supported by favorable supply-demand dynamics in both the DRAM and NAND markets. Industry conditions are likely to stay tight beyond 2027, which should continue to support Micron’s revenue growth and profitability.

For Q4, Micron is projected to generate approximately $50 billion in revenue, representing year-over-year (YOY) growth of 342%. Gross margin is expected to reach around 86%, a substantial improvement from 45.7% in the same quarter last year. Finally, EPS is forecast to rise sharply to $31, up from $3.03 a year earlier.

The Bottom Line on MU Stock

Micron is well-positioned to benefit from favorable trends shaping the memory market. Rising demand from AI applications, limited supply, and favorable pricing conditions are creating a strong environment for growth, supporting a rally in MU stock.

Even after a significant share price rally over the past year, Micron's valuation remains appealing. The stock trades at 17.4 times forward earnings, which appears reasonable given the company's growth prospects.

Wall Street analysts continue to assign a “Strong Buy” consensus rating to MU stock. All of these factors indicate that MU stock could reach the high target of $1,750 per share over the next 12 months.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Delta%20Air%20Lines%2C%20Inc_%20passanger%20plane-by%20viper-zero%20via%20iStock.jpg)