/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

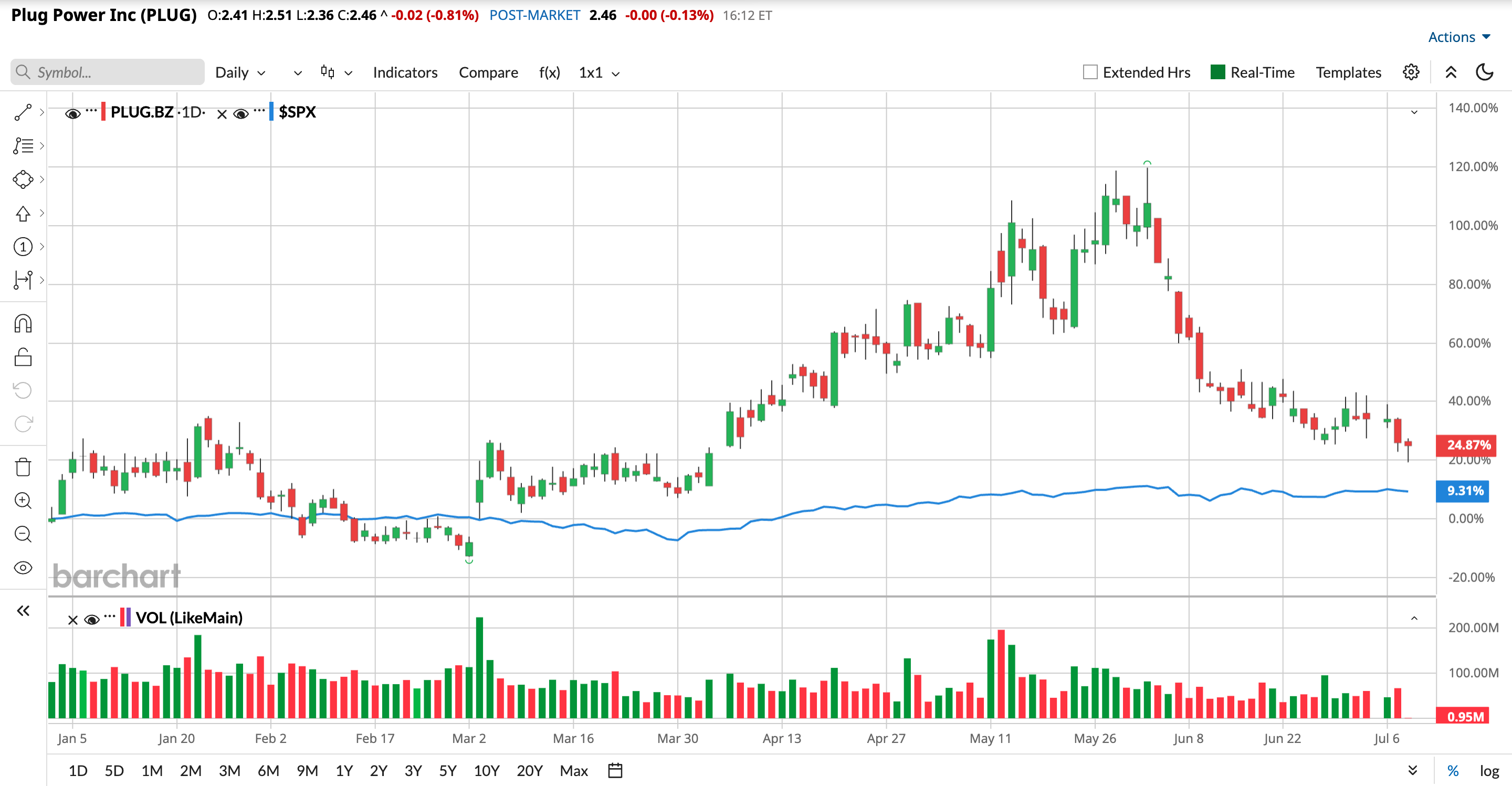

Plug Power (PLUG) shares have been nothing short of a rollercoaster ride over the past few years. At times, investors have flocked to the stock, encouraged by the hydrogen company's rapid sales growth, steadily narrowing losses, and massive long-term opportunity as artificial intelligence (AI) data center expansion fuels electricity demand and the global push for green hydrogen gathers pace. But those bursts of optimism have often been followed by sharp sell-offs, highlighting the market's uncertainty over the company's path forward.

And that uncertainty has resurfaced in recent weeks. Plug Power shares have slumped 22.7% over the past month as investors booked profits, while escalating geopolitical tensions and rising oil prices revived inflation fears, weighing on the broader industrial sector. Adding to the pressure are the slower-than-expected adoption of hydrogen technology and the company's still-distant path to profitability, both of which have continued to test investor patience.

However, the latest headline has given investors something to cheer about. Plug Power recently secured a major 50-megawatt electrolyzer contract for the Hunter Valley Hydrogen Hub in Newcastle, New South Wales, Australia, the country's largest green hydrogen project to reach a final investment decision. Developed by Orica alongside its ammonia plant on Kooragang Island, the facility will use Plug's GenEco Proton Exchange Membrane electrolyzers to produce approximately 4,700 tons of renewable hydrogen annually, replacing a meaningful portion of Orica's natural gas consumption.

So, with this significant project adding fresh momentum to the story, here's a closer look at whether Plug Power stock is worth considering now.

About Plug Power Stock

Rather than focusing on a single segment of the hydrogen value chain, New York-based Plug Power has built an integrated business spanning hydrogen production and storage, distribution and power generation. As one of the industry's early pioneers, the company offers a broad portfolio that includes electrolyzers, liquid hydrogen, fuel cell systems, storage tanks, and fueling infrastructure, serving customers across material handling, industrial operations, and the energy sector while supporting the broader shift toward lower-carbon energy.

Plug has established a significant global footprint, with its electrolyzer technology deployed on six continents and a growing pipeline of large-scale hydrogen production projects. The company has installed more than 74,000 fuel cell systems and over 280 hydrogen fueling stations worldwide, while also standing as the largest consumer of liquid hydrogen. To strengthen domestic supply, Plug continues to expand its hydrogen production network, with operational plants in Georgia, Tennessee, and Louisiana that can produce a combined 40 tons of hydrogen per day.

The company's operations are supported by a global workforce and advanced manufacturing facilities, enabling it to supply hydrogen solutions to a roster of leading companies, including Walmart (WMT), Amazon.com (AMZN), and Home Depot (HD). However, Plug shares have delivered a dramatic ride for investors. With a market capitalization of roughly $3.46 billion, the hydrogen stock has shed 46.3% from its 52-week high of $4.58, reached in October last year, as concerns over profitability and the pace of hydrogen adoption weighed on sentiment.

Yet, the bigger picture tells a different story. Even after the sharp correction, Plug Power shares remain up an impressive 73.6% over the past 12 months and have gained 25% so far in 2026. That's well ahead of the broader S&P 500 Index's ($SPX) 20.1% return over the past year and 9.2% gain year-to-date (YTD), underscoring the stock's ability to outperform despite its pronounced volatility.

Plug Power’s Q1 Earnings Snapshot

Plug delivered an encouraging set of first-quarter 2026 results on May 11, signaling that its turnaround efforts are beginning to gain traction. For the quarter ended March 31, the company generated revenue of $163.5 million, up a solid 22% year-over-year (YOY) from $133.7 million and comfortably ahead of Wall Street's expectations of approximately $141.1 million.

The strong top-line performance was primarily fueled by continued momentum in its material handling and electrolyzer businesses, while hydrogen fuel sales also climbed 22% from the prior-year quarter, supported by customer growth, higher pricing, and lower customer warranty charges. Beyond the revenue beat, Plug made meaningful progress on profitability.

The company improved its overall margin by an impressive 71%, with its GAAP gross margin narrowing sharply from negative 55% in the year-ago quarter to negative 13%. The improvement was driven by aggressive cost-cutting initiatives, a 30% reduction in per-unit service costs for its GenDrive systems, and greater operating efficiencies across its hydrogen production facilities in Georgia, Tennessee, and Louisiana. The bottom line also showed signs of improvement.

Plug reported an adjusted loss of $0.18 per share, beating analysts' consensus estimate of a $0.10 loss and improving significantly from the adjusted loss of $0.17 per share reported in the first quarter of 2025. However, on a GAAP basis, the company recorded a wider net loss of $245.3 million, largely due to approximately $140 million in mostly non-cash charges related to changes in the valuation of its convertible debt and warrants, which were driven by volatility in the company's share price.

Further, Plug exited the quarter with a solid liquidity position, holding more than $802 million in total cash, including $223 million in unrestricted cash and roughly $579 million in restricted cash. The company expects around $50 million of that restricted cash to be released each quarter over the next few years. Management further noted that cash usage tracked modestly better than its internal expectations and anticipates sequential improvement throughout the remainder of 2026, while continuing to target positive EBITDA in the fourth quarter of the year.

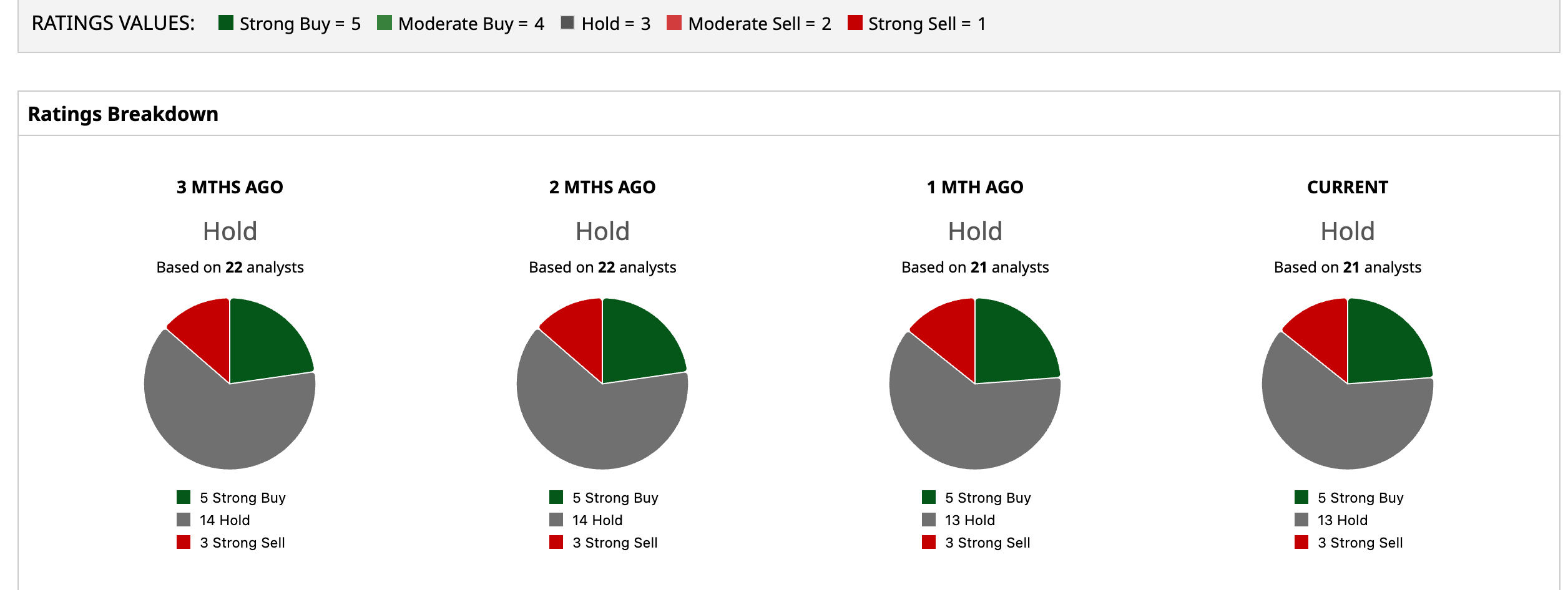

What Analysts Think About Plug Power Stock

Wall Street remains on the fence when it comes to Plug Power. The stock currently carries a consensus "Hold" rating, reflecting analysts' mixed views on its near-term prospects. Among the 21 analysts covering the company, five recommend a "Strong Buy," 13 advise "Hold," while three maintain a "Strong Sell" rating. Even so, analysts see meaningful upside if Plug Power can successfully execute its turnaround strategy.

The average price target of $3.61 implies a potential gain of 46.75% from current levels, while the Street-high target of $7 points to a possible upside of as much as 184.6% from here.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)