/Elements%20of%20cardboard%20boxes%20collected%20in%20stack%20packaging%20by%20Aleksandr%20Matveev%20via%20Adobe%20Stock.jpeg)

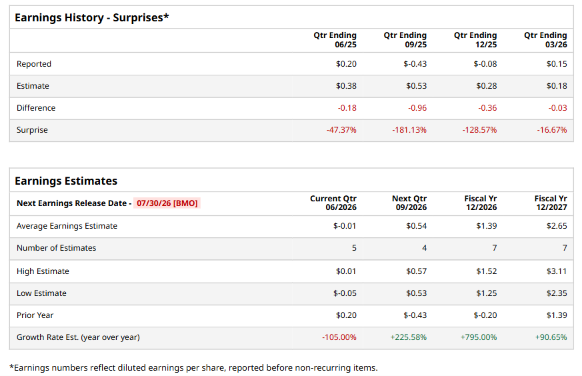

Memphis, Tennessee-based International Paper Company (IP) produces and sells renewable fiber-based packaging and pulp products. Valued at $20.4 billion by market cap, the company offers linerboard, medium, whitetop, recycled linerboard, recycled medium and saturating kraft, and pulp for a range of applications, such as diapers, towel and tissue products, feminine care, and other personal care products. The global leader in sustainable packaging solutionsis expected to announce its fiscal second-quarter earnings for 2026 before the market opens on Thursday, Jul. 30.

Ahead of the event, analysts expect IP to report a loss of $0.01 per share on a diluted basis, down 105% from profit of $0.20 per share in the year-ago quarter. The company missed the consensus estimates in each of the last four quarters.

For the full year, analysts expect IP to report EPS of $1.39, recovering 795% from loss per share of $0.20 in fiscal 2025. Its EPS is expected to rise 90.7% year over year to $2.65 in fiscal 2027.

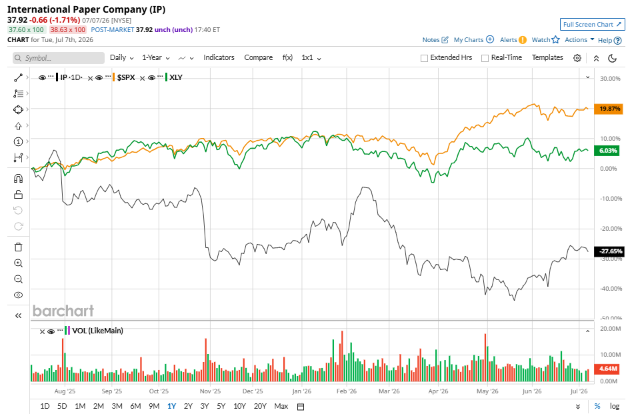

IP stock has underperformed the S&P 500 Index’s ($SPX) 20.5% gains over the past 52 weeks, with shares down 24% during this period. Similarly, it underperformed the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) 7.5% returns over the same time frame.

IP lagged despite beating earnings as $53 million in weather impacts, inflation, and restructuring costs outweighed North America volume growth and productivity wins. In addition, reliability issues and higher freight/energy also weighed on margins. EMEA is witnessing progress via 31 facility closures targeting $200 million+ in savings, but demand remains soft. Management expects H2 to improve on pricing actions and cost reductions, yet remains cautious on energy volatility and demand visibility.

Analysts’ consensus opinion on IP stock is moderately bullish, with a “Moderate Buy” rating overall. Out of 13 analysts covering the stock, eight advise a “Strong Buy” rating, one suggests a “Moderate Buy” three give a “Hold,” and one recommends a “Strong Sell.” IP’s average analyst price target is $40.59, indicating a potential upside of 7% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)