/Verisk%20Analytics%20Inc%20office%20building-by%20JHVEPhoto%20via%20iStock.jpg)

New Jersey-based Verisk Analytics, Inc. (VRSK) is a leading global data analytics and technology company that provides risk assessment, decision-support, and software solutions primarily to the insurance industry. Valued at a market cap of $24.6 billion, the company helps insurers, reinsurers, brokers, corporations, governments, and financial institutions analyze risk, improve underwriting accuracy, detect fraud, and streamline claims management.

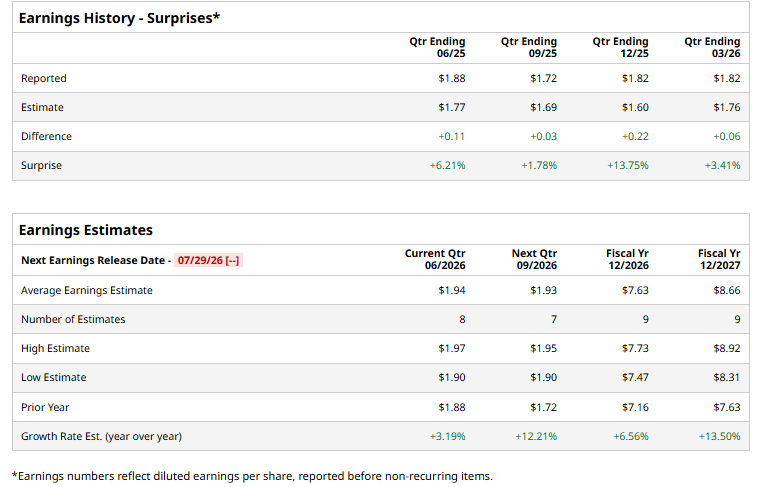

VRSK is expected to release its Q2 2026 earnings shortly. Ahead of the event, analysts expect the company’s EPS to be $1.94 on a diluted basis, up 3.2% from $1.88 in the year-ago quarter. The company has exceeded Wall Street’s EPS estimates in all of its last four quarters.

For fiscal 2026, analysts project the company’s EPS to be $7.63, up 6.6% from $7.16 in fiscal 2025. Moreover, its EPS is expected to rise 13.5% year over year to $8.66 in fiscal 2027.

Verisk’s shares have declined 39% over the past 52 weeks, underperforming the S&P 500 Index’s ($SPX) 33.5% rise and the State Street Industrials Select Sector SPDR ETF’s (XLI) 36.7% return during the same time frame.

Verisk has trailed the broader market over the past year as investor sentiment weakened over concerns that advances in generative AI could erode the company's competitive advantage in insurance data and analytics. The stock also faced pressure from slowing revenue growth, softer demand for catastrophe-related analytics, reduced federal contract activity, and a lower revenue outlook. More recently, sentiment was further dented after Nasdaq announced that Verisk would be removed from the Nasdaq-100 Index as part of its June 2026 quarterly rebalance, a move that likely triggered passive fund outflows and weighed on the shares.

Analysts are moderately bullish on VRSK, with the stock having a “Moderate Buy” rating overall. Among the 20 analysts covering the stock, nine are recommending a “Strong Buy,” one recommends a “Moderate Buy,” and ten suggest a “Hold.” VRSK’s average analyst price target is $220.67, indicating an upside of 14.8% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)