/Waste%20Management%2C%20Inc_%20truck-by%20hapabapa%20via%20iStock.jpg)

Waste Management, Inc. (WM), doing business as WM, is a leading North American provider of environmental services, offering waste collection, landfill disposal, recycling, and related sustainability solutions to residential, commercial, industrial, and municipal customers. It operates extensive landfill and recycling infrastructure and is headquartered in Houston, Texas, and has a market capitalization of $92.52 billion.

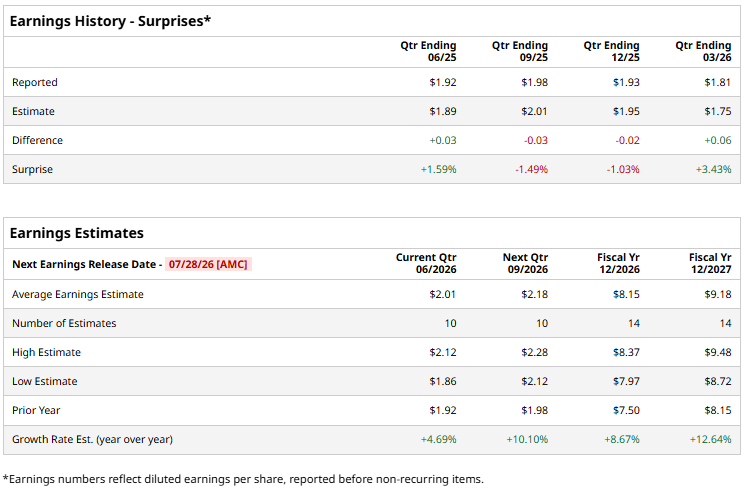

The company is expected to report its second-quarter results for fiscal 2026 on July 28, after the market closes. Ahead of the release, Wall Street analysts are optimistic about the company’s bottom-line trajectory.

Analysts expect WM to report a profit of $2.01 per share on a diluted basis for Q2, up 4.7% year-over-year (YOY). The company has surpassed consensus estimates in two out of four trailing quarters. For the full fiscal year 2026, Wall Street analysts expect the company’s diluted EPS to grow by 8.7% annually to $8.15, followed by a 12.6% improvement to $9.18 in fiscal 2027.

Based on consistent revenues and cash flow growth WM’s stock has been holding up well. Over the past 52 weeks, the stock has gained 3.1%, and year-to-date (YTD), it has climbed 4.9%. On the other hand, the broader S&P 500 Index ($SPX) has increased by 20.2% and 9.3% over the same periods, respectively. Hence, WM has underperformed the broader market over the past year.

Next, we compare the stock's performance with its sector’s performance. The State Street Industrial Select Sector SPDR ETF (XLI) has been up by 24.1% over the past 52 weeks and 18.6% YTD. Therefore, the stock has also underperformed its sector over these periods.

WM’s first-quarter revenues increased by 3.5% YOY to $6.23 billion. Although its topline fell short of expectations, the stock grew 1.3% intraday on Apr. 29 after the results were released. The company’s results were led by Collection and Disposal businesses, which, in turn, benefitted from disciplined price execution and continued optimization of business mix. WM also started operations at new recycling facilities in Ontario and Detroit and completed a recycling automation project in South Florida.

Wall Street analysts have been bullish about WM’s future. Among the 28 analysts covering the stock, the consensus rating is “Moderate Buy.” The rating configuration has remained the same over the past three months. WM has 18 “Strong Buy” ratings, one “Moderate Buy” and nine “Holds.” The mean price target of $256.46 implies an 11.3% upside from current levels. The Street-high price target of $275 implies a 19.4% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)