/Pest%20control%20exterminator%20spraying%20termite%20pesticide%20by%20Andrey%20Popov%20via%20Adobe%20Stock.jpeg)

Currently valued at $20.29 billion by market capitalization, Rollins, Inc. (ROL) is a global leader in pest control services, safeguarding more than 2.8 million residential and commercial customers across North America, South America, Europe, Asia, Africa, and Australia. Backed by a workforce of approximately 22,000 employees and a network of over 850 locations, the company delivers essential protection against termites, rodents, insects, and other pests.

The company’s impressive portfolio of trusted brands includes Orkin, Clark Pest Control, Fox Pest Control, HomeTeam Pest Defense, Northwest Exterminating, Western Pest Services, Critter Control, Saela Pest Control, and many others, making Rollins one of the world's largest and most recognized pest management companies. The Georgia-based company is gearing up to report its fiscal 2026 second-quarter results soon, with Wall Street expecting another solid performance.

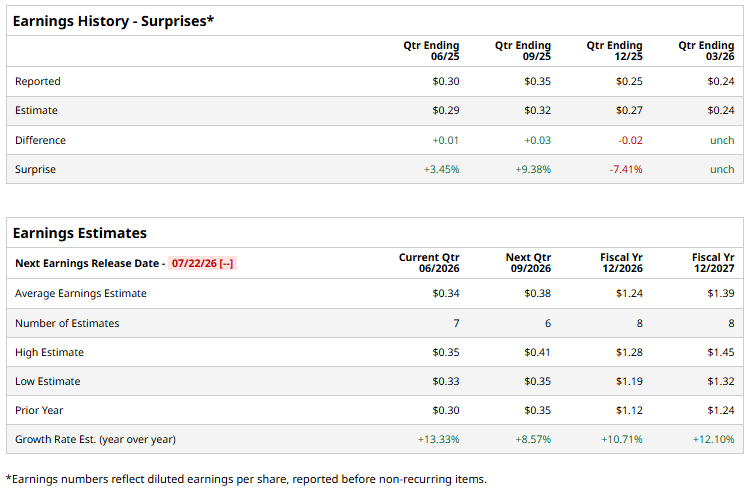

Analysts forecast earnings of $0.34 per share, representing a 13.3% year-over-year increase. Rollins has a strong track record of execution, having met or exceeded analysts' earnings estimates in three of the past four quarters and missing them once. Looking beyond the quarter, analysts expect the company to deliver full-year fiscal 2026 EPS of $1.24, up 10.7% from $1.12 in fiscal 2025. Earnings growth is projected to remain robust, with EPS expected to climb another 12.1% year over year to $1.39 in fiscal 2027.

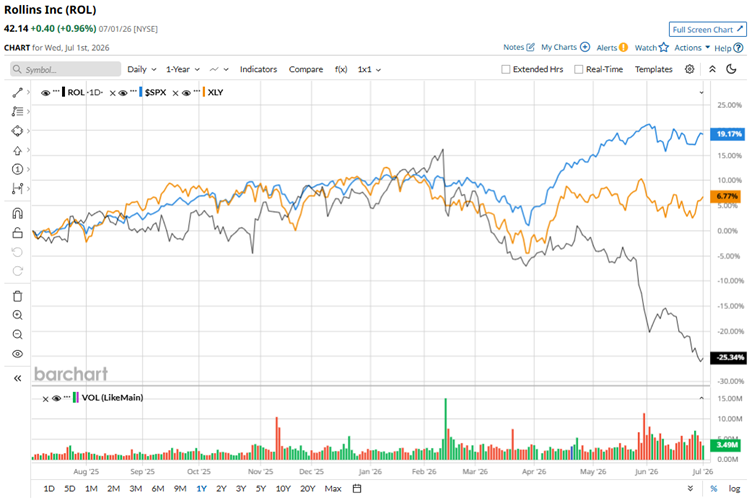

Rollins' stock has had a disappointing run over the past year, significantly underperforming the broader market. Shares have fallen nearly 25.6% during the period, sharply lagging the broader S&P 500 Index ($SPX), which has surged 20.7%. Meanwhile, the State Street Consumer Discretionary Select Sector SPDR ETF (XLY) has delivered a more modest gain of about 8.2% over the same stretch.

Rollins delivered a solid start to fiscal 2026, reporting first-quarter results on April 22 that exceeded revenue expectations. Revenue rose 10.2% year over year to $906 million, while organic revenue increased 6.6%, helping the company surpass Wall Street's revenue estimate of $894.8 million. On the bottom line, GAAP EPS was unchanged from the prior-year period at $0.22, while adjusted EPS increased 9.1% year over year to $0.24, matching analysts' consensus estimate.

Despite the stock's recent weakness, Wall Street remains cautiously optimistic about Rollins' prospects. The stock carries a consensus "Moderate Buy" rating based on coverage from 17 analysts, including nine "Strong Buy" recommendations, two "Moderate Buy" ratings, and six "Hold" calls. The average price target of $62.56 implies a potential upside of 48.5% from current levels, suggesting analysts see meaningful room for a rebound.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)