Dividend stocks have quietly been some of the better performers in 2026. In June, chip stocks came under pressure after Broadcom (AVGO) issued a weaker-than-expected chip sales outlook, which sparked a broader selloff across the sector and pulled the Nasdaq 100 ($IUXX) down as much as 3.29% in one session on June 23.

At the same time, dividend stocks were moving the other way, attracting investors looking for income and a bit more stability. HSBC Holdings (HSBC) raised its dividend by 350% in March after previously cutting it, while Crown Holdings (CCK) lifted its payout by 34.62%. That trend shows big dividend hikes are becoming a notable theme in 2026.

DuPont de Nemours (DD) just made one of the biggest moves in that group. On June 24, 2026, DuPont's board declared a quarterly dividend of $0.60 per share, payable on Sept. 15, 2026, to shareholders of record as of August 31. That marks a 200% increase from its previous payout and ranks among the sharpest single-quarter dividend resets announced by a blue-chip industrial company this year.

After a strong run in the stock over the past year, DuPont is now backing its outlook with a much bigger cash return to shareholders. But does this 200% dividend hike point to stronger business ahead? Let’s take a look.

The Numbers Supporting a 200% Hike

DuPont de Nemours makes specialty products used across areas like electronics, healthcare, industrial markets, and water treatment. Its business is built around materials and solutions that serve essential end markets.

DD stock has performed well, rising 58% over the past 52 weeks and another 13% so far this year.

Even after that run, DuPont trades at a forward P/E of 19.44x, which is a bit above the sector average of 15.91x.

The big news is the dividend increase. DuPont raised its most recent payout to $0.60 per share, a 200% jump from the previous level. Reported dividend yield figures stand at 145.55 and 106.07%, while the payout ratio is 1,517.50%, showing just how large this increase is compared with current earnings.

The company’s latest quarterly numbers were solid. In Q1 2026, net sales rose 4% to $1.7 billion, with organic sales up 2%. Operating EBITDA was $414 million, GAAP income from continuing operations was $150 million, GAAP EPS came in at $0.36, and adjusted EPS was $0.55. DuPont also generated $232 million in cash from operating activities and $147 million in transaction-adjusted free cash flow.

At the same time, it completed the Aramids divestiture on April 1 and said a $275 million accelerated share repurchase would begin shortly. For Q2, the company expects about $1.8 billion in sales, $430 million in operating EBITDA, and adjusted EPS of about $0.59. Full-year guidance now points to about 4% organic sales growth, including about 1% pricing to fully offset higher input costs tied to the Middle East conflict.

Business Drivers Powering Future Growth

DuPont is working with Uncountable to improve how it runs its labs and develops new products. The partnership brings an AI-based platform into its R&D process, helping the company organize data better and move from testing to real-world products faster. It also makes it easier to design and refine complex materials, cutting down development time and improving overall efficiency.

The same approach is showing up in its water business. DuPont recently launched an AI-powered Reverse Osmosis Operations Advisor that studies past system data and suggests when to clean or replace membranes. This helps operators avoid downtime, extend equipment life, and lower operating costs, while also improving system performance over time.

In healthcare, DuPont is expanding its product lineup with Liveo Pharma TPE Overmolded Assemblies. These are used in pharmaceutical and biopharma production to move ultrapure fluids safely. They help reduce contamination risk, prevent leaks, and cut down setup time and labor. The products are built to handle demanding conditions and fit into the company’s growing range of single-use solutions for drug manufacturing.

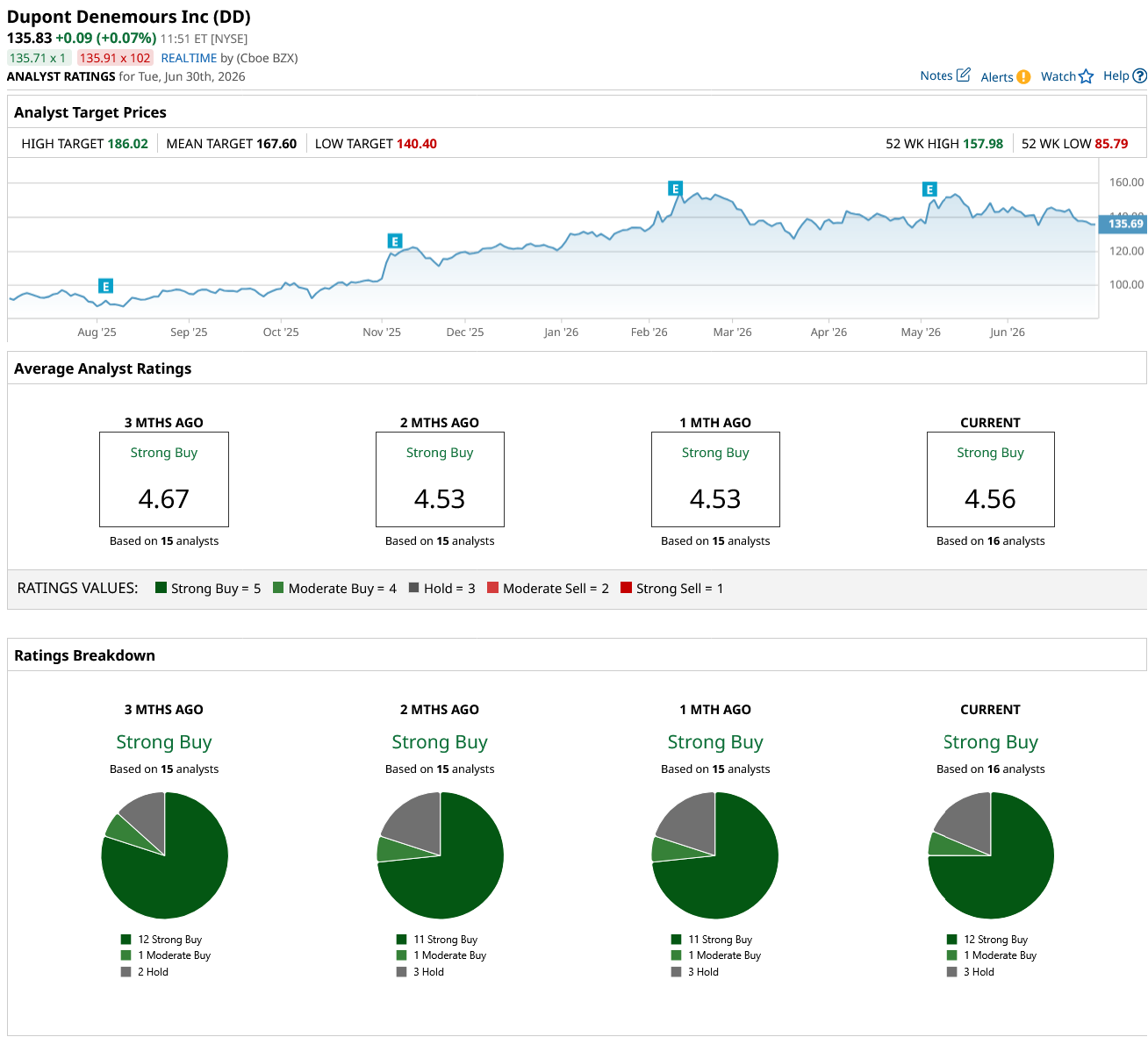

Analyst Views and Price Targets for DD Stock

DuPont de Nemours is set to report its next earnings on Aug. 4, 2026. For the current quarter ending in June, analysts expect $1.76 per share, down sharply from $3.36 a year ago, a drop of about 47.6%. The next quarter does not look much better, with estimates at $1.80 versus $3.27 last year, down roughly 45%. But for the full year, expectations improve, with 2026 earnings projected at $7.18, up 42.5% from $5.04 in 2025.

After a solid Q1 report in May, RBC Capital Markets analyst Arun Viswanathan raised his price target from $56 to $60 before the stock’s reverse split in June and kept an “Outperform” rating, pointing to steady underlying momentum.

Not everyone is as positive. Goldman Sachs started coverage in mid-June with a “Neutral” rating and a $53 target, saying DuPont may grow slower than others in its coverage group through 2028.

Even with that split, overall sentiment remains strong. The 16 analysts covering DD stock tracked by Barchart rate it a consensus “Strong Buy,” with an average price target of $167.60, implying about 22% upside from current levels.

Conclusion

DuPont’s 200% dividend hike is a bold signal, but it is not happening in isolation. The company is pairing strong recent price performance, steady cash generation, and clear innovation-driven growth initiatives with a willingness to return more capital to shareholders. While near-term earnings comparisons look soft, the longer-term outlook and analyst optimism suggest confidence in a rebound. Shares are likely to remain supported if execution stays on track, with a bias toward gradual upside rather than sharp moves, especially as income-focused investors continue rotating into stable, dividend-paying names.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)