Seagate (STX) is one of the best-performing stocks in the S&P 500 Index ($SPX), with shares surging 253.6% this year already. The rally reflects surging investment in AI infrastructure, which is driving unprecedented demand for high-capacity storage solutions. Tight industry supply has further strengthened pricing power, driving sharp improvements in both revenue and profitability.

Despite its massive run, Seagate's growth story is far from over. In its latest quarter, the company generated $3.1 billion in revenue, up 44% year-over-year (YOY), with its data center business growing at a solid pace and accounting for the majority of its revenue. Demand from hyperscale cloud providers and enterprise customers continues to accelerate as AI workloads require larger, more cost-efficient storage systems.

The company's profitability is also improving quickly. Higher pricing and an improved mix of high-capacity drives lifted adjusted gross margin to 47%, up from 42.2% in the previous quarter, supporting Seagate's bottom line.

Looking ahead, Seagate remains well-positioned to capitalize on favorable industry dynamics. Its Mozaic platform and Heat-Assisted Magnetic Recording (HAMR) technology enable higher storage density while supporting future margin expansion. At the same time, the company's build-to-order (BTO) manufacturing model provides better visibility into customer demand, helping maintain pricing discipline and a balanced supply environment.

In addition, Seagate is strengthening its balance sheet. During the last reported quarter, it repaid $641 million of debt, reducing gross debt to approximately $3.9 billion. Since the start of fiscal 2026, total debt has fallen by roughly $1.1 billion, bringing net leverage down to just 0.7x. Combined with strong cash generation, the company's improving financial position provides greater flexibility to invest in future growth while returning capital to shareholders.

These factors suggest that Seagate remains well-positioned to benefit from the long-term expansion of AI-driven data storage demand. However, Sandisk stock looks like a better option.

Why Sandisk Looks Like the Better Buy

Sandisk (SNDK) stock offers a more attractive risk-reward profile in the memory market. Its relatively lower valuation and solid earnings growth trajectory make it a better buy.

Sandisk is growing rapidly. During the last reported quarter, Sandisk’s revenue surged 251% YOY, driven by the strong performance of the data center business. The data center business reported 233% sequential revenue growth, driven by soaring average selling prices and shipments. The company’s profitability also improved sharply, with adjusted gross margin expanding to 78.4% from 51.1% in the previous quarter.

Also, Sandisk is strengthening its operating structure. Its new business models (NBMs), which are multi-year supply agreements, reduce reliance on volatile spot-market pricing, improving revenue visibility and production planning. During the third quarter, the company signed three contracts with minimum revenue commitments totaling approximately $42 billion, backed by financial guarantees. Some agreements extend up to five years and allow revenue to grow as customer commitments increase.

Importantly, these contracts combine fixed and variable pricing, allowing Sandisk to participate in upside from memory prices while providing downside protection during weaker market conditions. This combination of structural improvements and strong AI-driven demand supports a more sustainable earnings outlook.

Valuation Makes the Difference

Both Seagate and Sandisk are well-positioned to benefit from the growing demand for memory and storage solutions, and Wall Street remains highly optimistic about both companies, with a "Strong Buy" consensus rating. However, when valuation is factored in, Sandisk stands out as the more compelling opportunity.

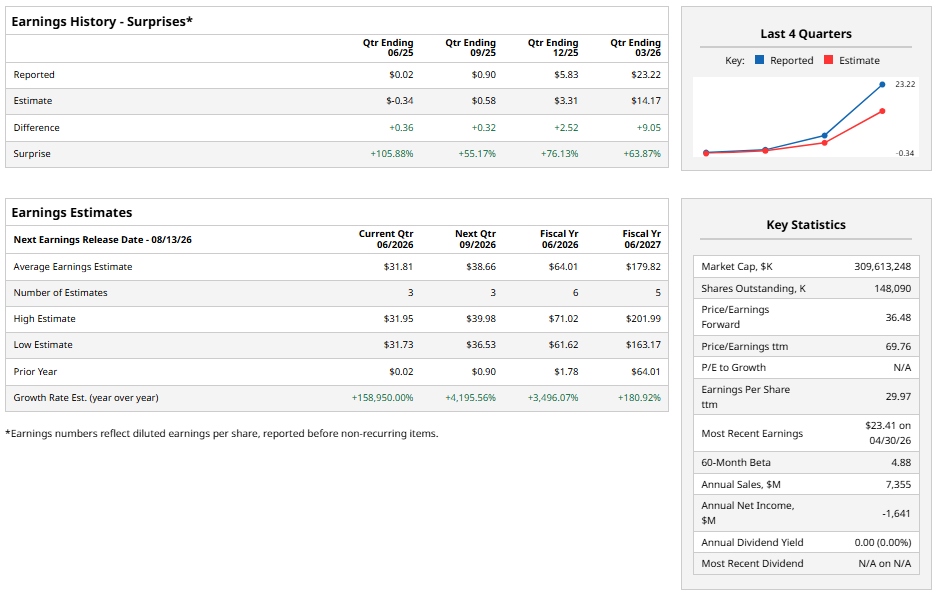

Despite its impressive rally, Sandisk still trades at a relatively reasonable valuation. The stock is valued at 32.66 times forward earnings, a multiple that looks attractive considering analysts expect earnings per share to surge 3,496% in fiscal 2026, followed by another 181% growth in fiscal 2027.

Seagate, by comparison, trades at a much steeper 63.65 times forward earnings. While analysts expect the company to deliver healthy 94.8% EPS growth in fiscal 2027, that growth appears less compelling given its higher valuation multiple.

Overall, both stocks have strong growth prospects, but Sandisk currently offers a more attractive risk-reward profile.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)