AI is no longer just changing technology; it is changing the how we invest, too.

Over the past year, investors have continued to reward companies connected to artificial intelligence, especially those helping build the systems behind it. For income investors seeking AI-related growth, the question is not only which company has greater AI exposure but also which one offers a better mix of growth, valuation, and shareholder returns.

And for companies seeking both AI exposure and dividend yields, the conversation ultimately turns to NVIDIA and Broadcom. So let’s look at the two companies side by side.

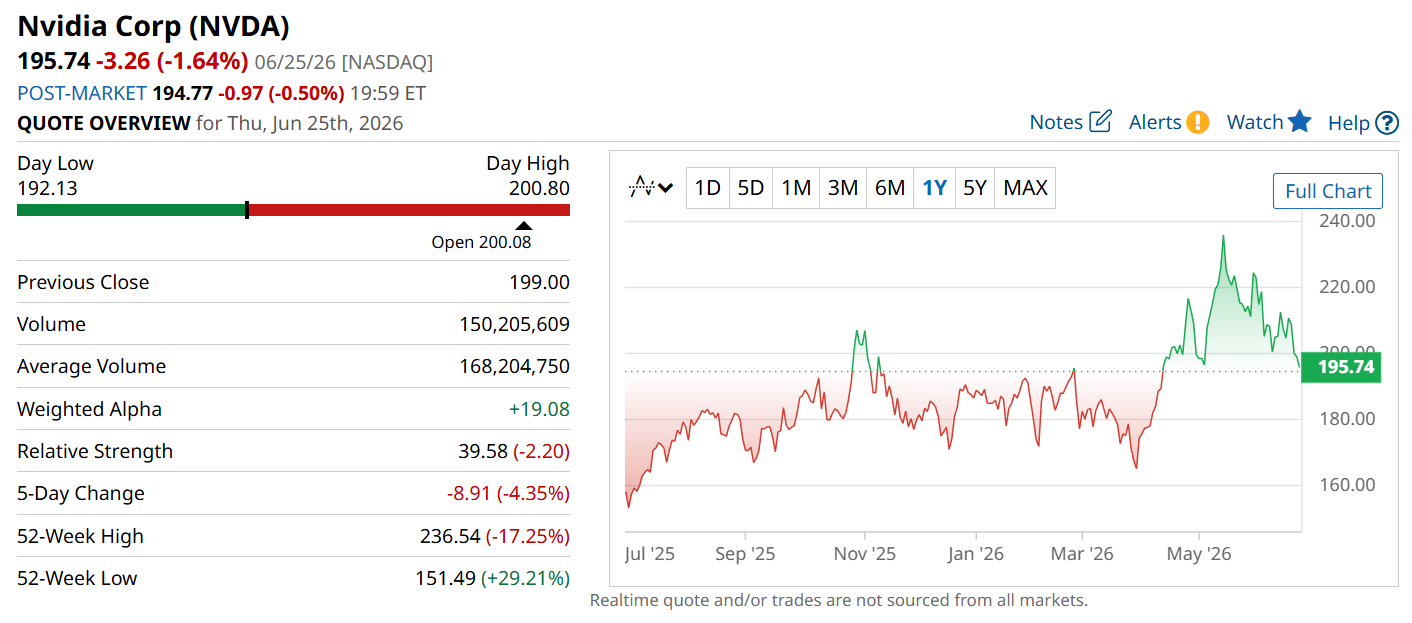

NVIDIA (NVDA)

NVIDIA is the world’s leading AI chip company, known for its graphics processing units (GPUs), which power AI models and advanced computing systems. The company has the biggest market cap in the world, currently at $4.8 trillion. While I'm on the topic, NVDA stock has traded between $151 and $236 in the last year.

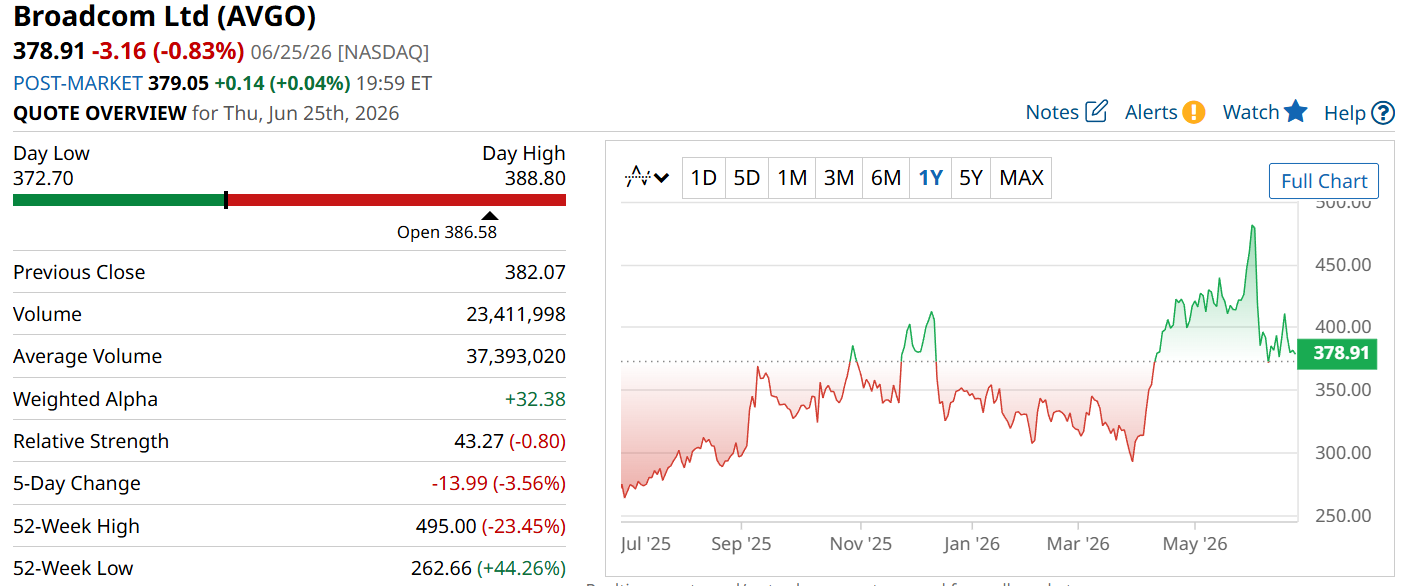

Broadcom (AVGO)

On the other hand, Broadcom is best known for its semiconductors and infrastructure software. While NVIDIA is strongly tied to GPUs that power AI computing, Broadcom plays a role in the systems around it, making it an important AI-related company with a more diversified business.

Broadcom currently has a market cap of $1.8 trillion, roughly a third of Nvidia’s, and the stock has traded between $267 and $495 in the last 52 weeks.

Business model comparison

NVIDIA and Broadcom both benefit from the rise of artificial intelligence, but their businesses aren't the same.

NVIDIA is more focused on AI computing. Its biggest growth driver is its GPU business, which powers the training and running of today's most advanced AI models. This gives NVIDIA stronger direct exposure to AI demand, as practically every hyperscaler is buying its chips.

Broadcom, however, is more diversified. It earns revenue from custom semiconductors used in a wide range of systems, including networking, wireless, data centers, and more. It is also growing its infrastructure software business through VMware. Its AI opportunity is more tied to customizing those semiconductors that support large AI data centers.

Simply put, NVIDIA is the more “off the shelf” AI chip play, while Broadcom is in the broader AI infrastructure and software business.

Financial health

Now let’s look at their latest reported numbers and their current valuations.

| Metric | NVIDIA | Broadcom |

| Sales | $81.6 billion (+85% YOY) | $22.2 billion (+48% YOY) |

| Net Income | $58.3 billion (+210% YOY) | $9.3 billion (+88% YOY) |

| Operating Cash Flow | $50.3 billion | $18.8 billion |

| Forward P/E | 23.02x | 37.13x |

| Price/Sales Ratio | 24.76x | 28.31x |

Right off the bat, NVIDIA looks better with sales up 85% YOY to $81.6 billion and net income up 210% to $58.3 billion.

Meanwhile, Broadcom’s sales rose 48% YOY to $22.2 billion, and net income increased 88% to $9.3 billion.

To no one’s surprise, operating cash flow also favors NVIDIA, at $50.3 billion versus Broadcom’s $18.8 billion. This is an important metric because it shows how much cash the business produces from regular operations.

Moving on to valuation, NVIDIA looks like a better buy, trading at around 23x forward earnings and 25x sales, while Broadcom trades at 37x forward earnings and 28x sales. So, despite trading at a near $5-trillion market cap, NVIDIA still looks cheaper compared to Broadcom, at least based on traditional metrics.

Overall, NVIDIA takes the win here.

Dividend story

NVIDIA pays a forward annual dividend of $1.00, translating to a yield of 0.50%. The company also has a dividend payout ratio of just 0.7%. That means it mostly reinvests its earnings into business activities, which makes sense since the company is gearing for massive growth.

Meanwhile, Broadcom pays $2.60 per share a year, translating to a yield of around 0.66%, with a more reasonable 35% dividend payout ratio. However, Broadcom has something that NVIDIA does not- a 15-year streak of consecutive dividend increases.

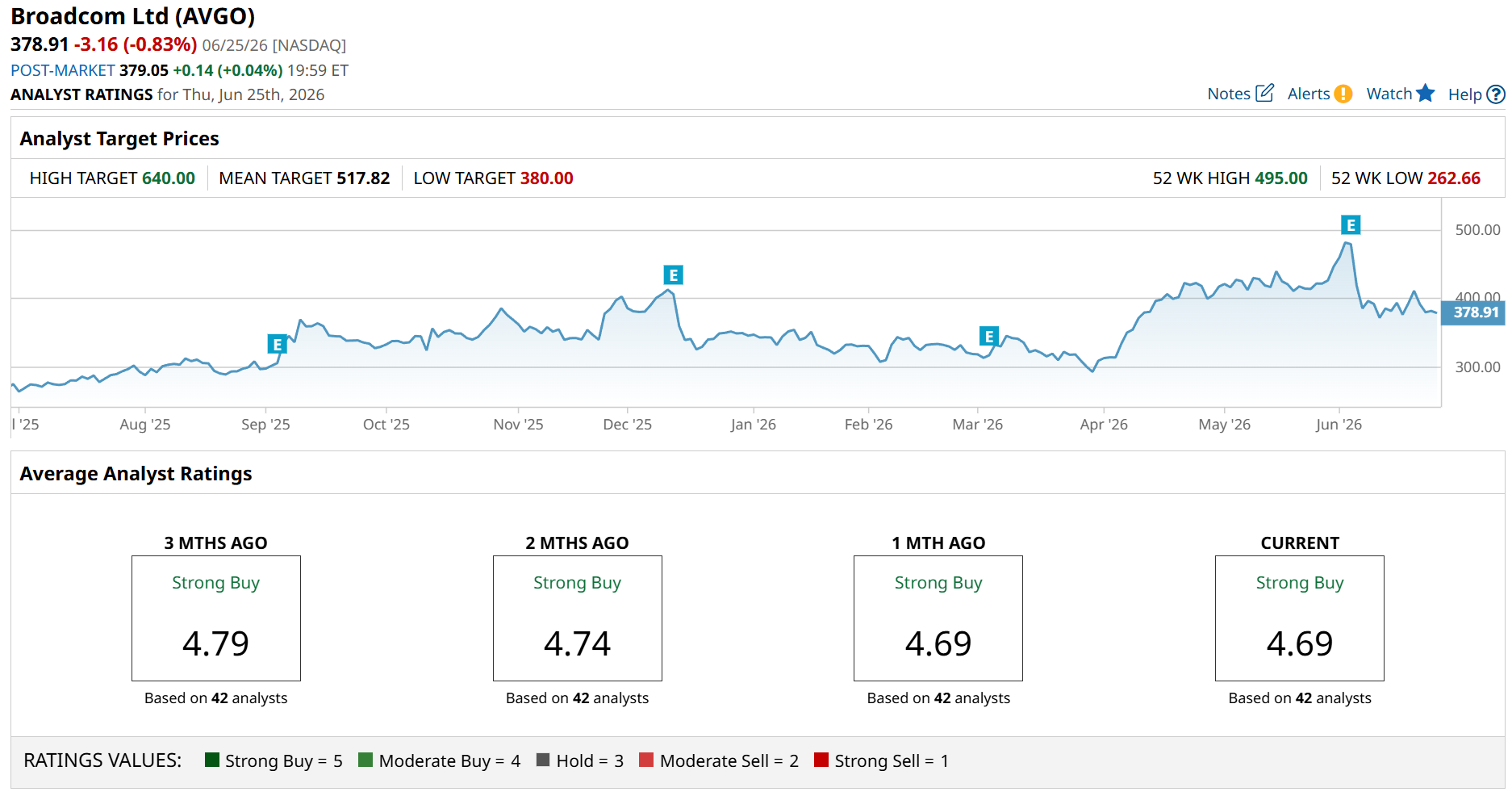

What do the analysts say?

Now let’s see what Wall Street says.

A consensus among 49 analysts rate NVIDIA stock a “Strong Buy,” with its mean-to-high target prices suggesting massive potential upside, reaching up to 155%.

Broadcom has a similar story, with a “Strong Buy” rating from 42 analysts, though its average score is lower. Its target prices indicate moderate potential growth up to 69%.

Verdict

Both companies are performing well and make good additions to a long-term portfolio. However, they’re doing very different things, both with the business and their commitment to shareholder value. If you’re aiming for potentially higher capital gains, I think NVIDIA is the better choice. But if you prefer to give up AI exposure in exchange for a little more dividend yield and growth, then Broadcom is the best bet.

In any case, the choice is always up to you. Just as long as you understand what you’re investing in.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)