Berkshire Hathaway (BRK.A) (BRK.B) has been a net seller of stocks for 14 consecutive quarters, including Q1 2026, which was the first quarter under CEO Greg Abel, who took over the baton from the legendary Warren Buffett earlier this year.

Abel has, however, been on a check-writing spree in Q2. The company has announced a deal to acquire Taylor Morrison Homes Corp (TMHC) for $6.8 billion and bought $10 billion worth of Alphabet (GOOG) (GOOGL) shares in a private placement. After that investment, Alphabet is now among Berkshire’s top five holdings alongside Apple (AAPL), American Express (AXP), Coca-Cola (KO), and Bank of America (BAC).

Berkshire Has Increased its Alphabet Stake Gradually

Notably, Berkshire first bought Alphabet shares in Q3 2025 and more than tripled its stake in Q1 2026. The conglomerate invested another $10 billion in the Google parent earlier this month as part of the $80 billion capital raise. The capital raise, which was preceded by a bond sale earlier this year, is meant to fund Alphabet’s burgeoning capex to build artificial intelligence (AI) infrastructure. Buffett, who generally shied away from tech stocks, had a nuanced view of AI, though. The nonagenarian compared AI’s risks to those of nuclear bombs and raised concerns about the technology being an enabler for scammers. However, with Alphabet, Berkshire is playing the AI story.

Alphabet Trades Below the Price Berkshire Invested in the Stock

Meanwhile, the conglomerate seemed to have got a good deal in private placement as it received Alphabet shares at a discount of more than 6% over its Monday, June 1, closing price. However, thanks to the recent decline in its shares, Alphabet has fallen below the levels at which Berkshire acquired them in the private placement. It's not often that we get to invest in a stock at levels below what a value-oriented company like Berkshire acquires them.

I was bearish on Alphabet shares for much of this year, not because I found the company’s outlook to be terrible, actually far from it, but because of its valuations, which I found a bit high for comfort. In my previous article, I noted that the stock can be nibbled at as the valuations had corrected. With the stock coming off those levels also, let’s see if it is a screaming buy yet.

Why Has Alphabet Stock Fallen?

It has been kind of a perfect storm for Alphabet over the last few weeks. Hyperscalers have looked weak as markets question their burgeoning capex, which could explode further given the rise in memory prices. Alphabet, particularly YouTube, has also been battling legal and regulatory issues amid the global clamor to ban social media for teens. Stateside, earlier this year, a Los Angeles jury found that Meta Platforms (META) and YouTube were negligent in protecting young users on their platforms and deliberately structured their platforms to make them addictive. In a blow to these companies, the judge recently rejected their bid for a new trial.

In a related move, YouTube settled the case of a minor known by his initial R.K.C., who claimed that the platform damaged his mental health. Thousands of such cases are pending in California courts, both state and federal, and are a hanging sword for Alphabet. Notably, one of the reasons Alphabet stock outperformed last year was because of the legal reprieve in the U.S. Department of Justice antitrust case, as District Judge Amit Mehta allowed it not only to retain Chrome and Android, but also to continue its partnership with Apple that makes it the default choice on iPhones.

If these headwinds weren’t enough, Alphabet has recently witnessed the exodus of leading AI researchers, including John Jumper, who, alongside Demis Hassabis, won the 2024 Nobel Prize for his work on AlphaFold that predicted over 200 million protein structures. While there are fears that AI would eventually replace a lot of humans, for now, tech giants are scrambling for AI talent, and some of the recent acquisitions have seemed like talent hunting rather than buying out companies. Losing key AI talent has dampened sentiments towards Alphabet and added fuel to the sell-off.

Should You Buy GOOG Stock?

All said, I remain bullish on Google given how it has held its ground in search, strong growth in cloud, with the business growing much faster than its two bigger rivals, Amazon (AMZN) and Microsoft (MSFT), in that order, and the expected revenue growth from tensor processing unit (TPU) and graphics processing units (GPUs).

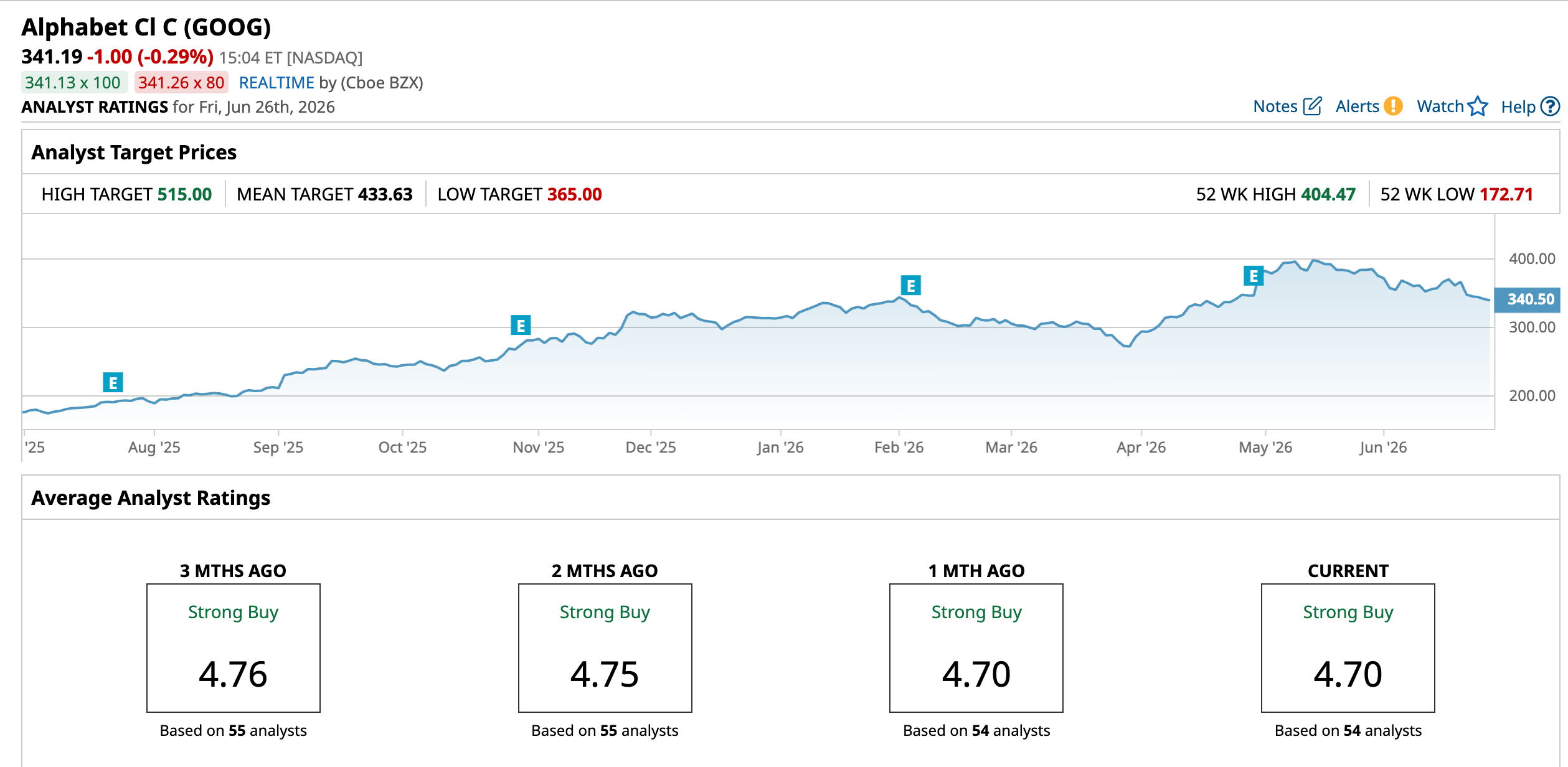

Alphabet’s mean target price of $433.63 implies an upside of 27% over the next 12 months. However, I won't put the stock in the category of a "screaming buy” yet, as I don’t see much margin of safety here at a forward price-to-earnings multiple of 24.13 times. Overall, while I remain invested in the stock after having previously partially booked profits, I am not too keen to add more shares at these levels.

On the date of publication, Mohit Oberoi had a position in: GOOG, AMZN, MSFT, META. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)