It’s been less than six months since Greg Abel took over as Berkshire Hathaway’s (BRK.B) CEO, but it's hard to miss the changes happening at the $1 trillion conglomerate. In Q1 2026, which was the first quarter under his leadership, Abel made several changes to the company’s portfolio of publicly traded securities.

First, Berkshire reduced its holdings of publicly traded stocks from 42 to 29, which, as I noted previously, was a smart move as these small holdings don’t move the needle for the company. Berkshire added a stake in Delta Airlines (DAL), a sector Warren Buffett burnt his fingers in and has long been talking down.

Greg Abel Is On a Check Writing Spree

Meanwhile, despite these changes, Berkshire was a net seller of stocks in Q1 for the 14th consecutive quarter. It is the longest such streak for the company, where it has sold more shares than it bought. However, things look set to change in the current quarter as, in a span of a few days, Berkshire has announced investments worth $16.8 billion.

The company has announced a deal to acquire Taylor Morrison Homes Corp (TMHC) for $6.8 billion and agreed to buy $10 billion worth of Alphabet (GOOG) (GOOGL) shares in a private placement. While we’ll get to know the official numbers later, in all probability Berkshire should be a net buyer of stocks in the current quarter unless, of course, Abel gets rid of a major holding.

Berkshire Repurchased Shares in Q1 After a Gap of Seven Quarters

Abel is not only writing checks to acquire stakes in other companies, but in Q1, the conglomerate repurchased its shares worth $235 million. While the amount is small by Berkshire’s standards, the pivot is noteworthy as the company did not repurchase any shares in the preceding seven quarters. The last couple of years were what Buffett described as his “nightmare” scenario in a 2019 interview with the Financial Times. The legendary investor joked that it would be a scenario wherein he finds stocks expensive, while Berkshire Hathaway shares are fairly valued.

It would also be pertinent to look at Berkshire’s buyback policy. Until 2018, it used to repurchase shares only as long as they were up to 1.2x of the book value, but subsequently, the company made the policy flexible, giving more discretion to Buffett to buy back the shares.

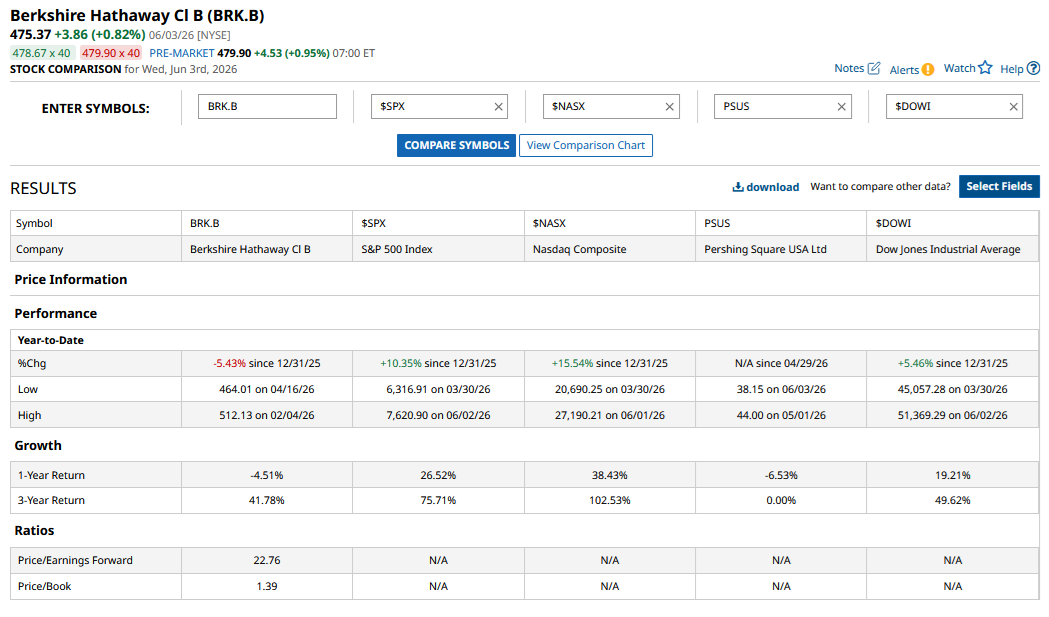

Now that authority should be lying with Abel, who seems to find some value in Berkshire shares, which have underperformed the markets this year. While the S&P 500 Index ($SPX) has been scaling record highs, Berkshire has lost 4.78% this year and trades 11.7% below its all-time highs, which it incidentally hit a day before Buffett announced his retirement at last year’s annual shareholder meeting.

Berkshire Stock Has Underperformed Over the Last Three Years

Notably, Berkshire shares have sagged over the last few years and are up 41.78% over the last three years versus the 75.7% rise in the S&P 500 Index. There have been a couple of reasons why the stock has underperformed. The first is that Berkshire was on a selling spree and raised its cash to subsequent record highs.

While Berkshire is a conglomerate and runs several businesses, it also has a portfolio of publicly traded securities as a hedge/mutual fund does. It's safe to say that any fund that sits on such a massive cash pile would underperform in rising markets, while outperforming when markets fall – and that’s precisely what has been happening with Berkshire stock over the last three years.

Secondly, the market rally over the last couple of years has been led by artificial intelligence (AI) stocks, and Berkshire has limited exposure to the sector. True, Apple (AAPL) is still Berkshire’s top holding, but the iPhone maker hasn’t really been a prominent AI play and is still seen as a laggard in the space.

Meanwhile, Abel has now started writing checks for AI companies, as is visible in his doubling down on Alphabet. After the $10 billion investment is completed, Alphabet would cement its position among Berkshire’s top four holdings and should soon become the third biggest holding after Apple and American Express Company (AXP).

Should You Buy Berkshire Stock?

Valuing a conglomerate like Berkshire is always a complex task given the various moving parts. The price-to-earnings multiple is particularly irrelevant as Berkshire’s accounting earnings don't provide the true picture due to the gains/losses on publicly traded securities. Price-to-book value multiple is a good yardstick, though, and looks reasonable at around 1.4x.

Berkshire has arguably lost the “Buffett premium,” and it has suppressed the stock’s valuation multiples. However, Abel is now trying to come out of “Oracle of Omaha’s” shadow, as is visible in the recent actions. I exited Berkshire shares earlier this year but see it getting attractive here on reasonable valuations and signs that the company is finally looking to deploy its burgeoning cash pile. I see a strong chance of BRK.B outperforming the S&P 500 Index over the next couple of years as markets gain more confidence in Abel’s ability to steer the company.

On the date of publication, Mohit Oberoi had a position in: GOOG . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.