Berkshire Hathaway (BRK.B) has released its 13F for the first quarter. The filing was all the more important as it provides insights into the investing philosophy of new CEO Greg Abel, who took over the baton from the legendary Warren Buffett earlier this year.

The filing showed that Berkshire reduced the number of positions from 42 to 29, which I would term as a smart move. Incidentally, earlier this year, I noted that Abel should exit the smaller holdings in Berkshire’s portfolio, particularly those valued below $1 billion, as they don’t move the needle for the $1 trillion behemoth.

Meanwhile, as part of the churn, which marked the 14th consecutive quarter in which Berkshire sold more shares than it bought, the conglomerate exited Amazon (AMZN) while doubling down on Alphabet (GOOG) (GOOGL), the best-performing Magnificent 7 stock this year. Notably, in 2017, Buffett had admitted to missing out on both Alphabet and Amazon.

Berkshire Bought Amazon in 2019

Berkshire bought Amazon in Q1 2019, and Buffett categorically said that the decision wasn't his. This would mean that the purchase was made either by Ted Weschler or Todd Combs. Combs has since left Berkshire to join JPMorgan (JPM), and reports suggest that Berkshire has sold the portfolio he managed.

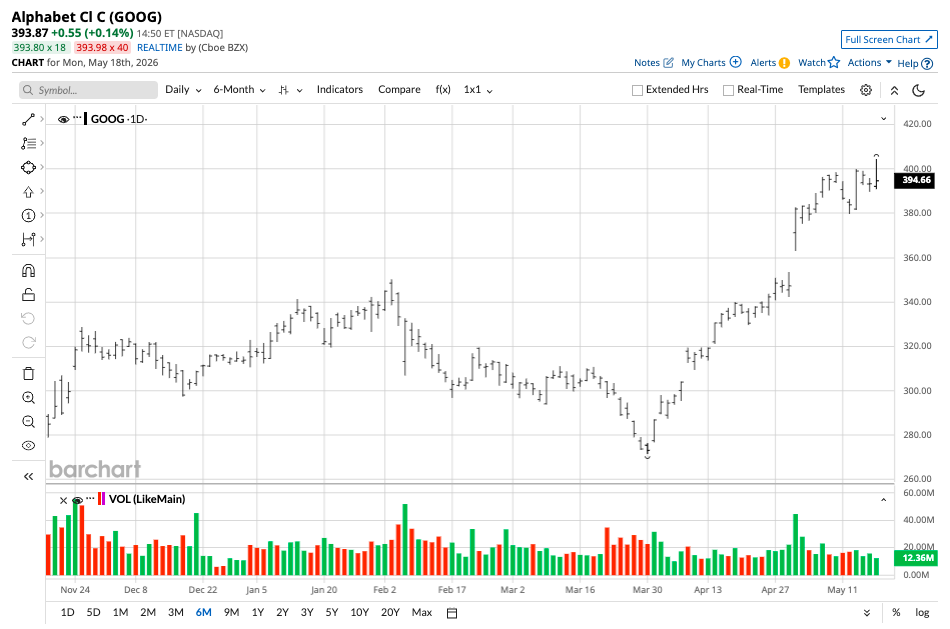

As for Alphabet, Berkshire initiated the position in Q3 2025 and has now tripled its stake in the search giant. We can be reasonably sure that Buffett did not make the initial purchase, given his reluctance to buy tech stocks. Also, since Berkshire’s stake in Alphabet is now upwards of $20 billion, we can make a smart guess that the decision was made by Abel himself, as Weschler manages a much smaller portfolio.

Let’s now explore whether ditching Amazon to buy Alphabet would be a wise strategy for us.

Alphabet Has Proven Its Prowess in AI

Alphabet has proved its mettle in artificial intelligence (AI) even as some of the high-flying startups (read: OpenAI), which had the initial lead, are now somewhat struggling. The Sundar Pichai-led company always had a captive base of users, and all it needed was a good product proposition, something it now has with Gemini.

Moreover, Alphabet’s cloud segment has been growing at a phenomenal pace. The segment's revenues rose 63% year-over-year in Q1 2026, with the growth far outstripping what Amazon and Microsoft (MSFT) delivered. Its tensor processing unit (TPU) and graphics processing units (GPUs) are also gaining traction with third-party customers. Citizens JMP, which has a “Market Outperform” rating on GOOG, expects TPU sales to reach about $3 billion in 2026 and $25 billion in 2027.

Meanwhile, thanks to the rally over the last year, Alphabet’s forward price-to-earnings (P/E) multiple has expanded to nearly 28x. The multiples are not exorbitant, but don’t leave much on the table for the short term.

While we don’t know the price levels at which Berkshire bought Alphabet shares, at these levels, I don’t find the Google-parent’s risk-reward as particularly attractive for the short term. However, the stock could still deliver strong returns over the next couple of years, considering its enviable progress in AI.

Amazon Does Not Look Like a Sell

There is indeed a bearish thesis for Amazon as the company continues to lose cloud market share, and in percentage terms, both Microsoft and Alphabet, the next two leading players in that order, are growing at a much faster pace. The company’s core e-commerce growth in the U.S. market is flattening, while the rise of AI agents is seen as a major risk for Amazon’s lucrative digital advertising business.

However, I believe that the bullish narrative is stronger. Firstly, instant deliveries and groceries should help buoy Amazon’s e-commerce growth. Amazon’s chip business is also growing, and according to the company, if its chip segment were a standalone company, its annual revenues would be $50 billion.

New initiatives like the Leo satellite network should also help drive growth over the long term. The company has secured commitments from both private enterprises and government agencies for its satellites. Overall, I don’t believe Amazon is a sell at current price levels, even as I don’t find it a tempting buy either, given the fair valuations.

On the date of publication, Mohit Oberoi had a position in: AMZN, GOOG, MSFT. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)