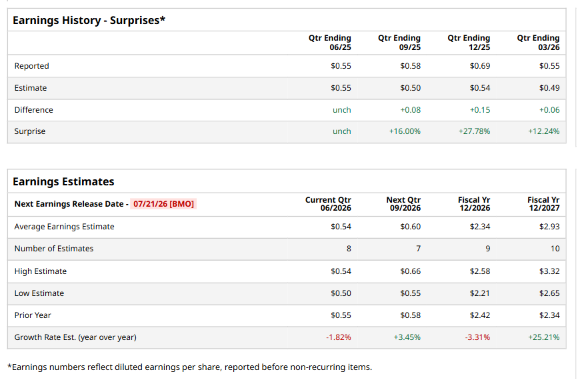

Houston, Texas-based Halliburton Company (HAL) provides energy, engineering, and construction services and manufactures products for the energy industry. Valued at $28.6 billion by market cap, the company offers services and products and integrated solutions to customers in exploration, development, and production of oil and natural gas. The leading energy equipment and services provider is expected to announce its fiscal second-quarter earnings for 2026 before the market opens on Tuesday, Jul. 21.

Ahead of the event, analysts expect HAL to report a profit of $0.54 per share on a diluted basis, down 1.8% from $0.55 per share in the year-ago quarter. The company has surpassed or met Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect HAL to report EPS of $2.34, down 3.3% from $2.42 in fiscal 2025. However, its EPS is expected to rise 25.2% year over year to $2.93 in fiscal 2027.

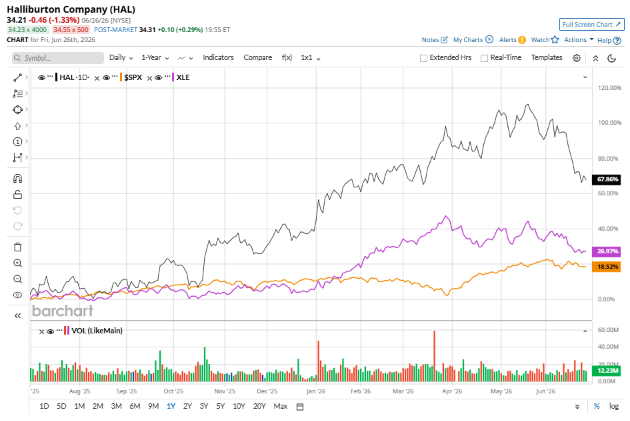

HAL stock has outperformed the S&P 500 Index’s ($SPX) 19.8% gains over the past 52 weeks, with shares up 65.8% during this period. Similarly, it outperformed the State Street Energy Select Sector SPDR ETF’s (XLE) 25.6% returns over the same time frame.

HAL’s strong performance was driven by strong international activity and early North America recovery, offsetting Middle East disruptions in Iraq and Qatar with gains in Latin America and Europe/Africa. CEO Jeffrey Miller highlighted the multi-year YPF Argentina deal for electric fracturing and automation, while the Sekal acquisition and Drilltronics platform boosted automated drilling wins in Guyana and Suriname. Even though North America revenue fell YoY, smaller operators are tightening fracturing capacity and premium equipment use is rising.

Analysts’ consensus opinion on HAL stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 25 analysts covering the stock, 15 advise a “Strong Buy” rating, three suggest a “Moderate Buy,” six give a “Hold,” and one recommends a “Strong Sell.” HAL’s average analyst price target is $44.72, indicating a notable potential upside of 30.7% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)