The following is a recent report in The Spread Trader newsletter, published by Klarenbach Research.

My colleague, Brent Futz, a former WCE floor trader with 40 years of experience trading commodities, leads that publication.

The Continued Decline of the Oat Futures Contract

I wrote an article on the Oat Futures Contract two weeks ago, in which I expressed concern about the contract's long-term viability.

My concern was focused on the July/Sept spread, which was trading at $.21 under.

My point was that a perpetual long position held for a year would offer minimal price-risk protection if the position was rolled at a contango of $ 0.10 per month.

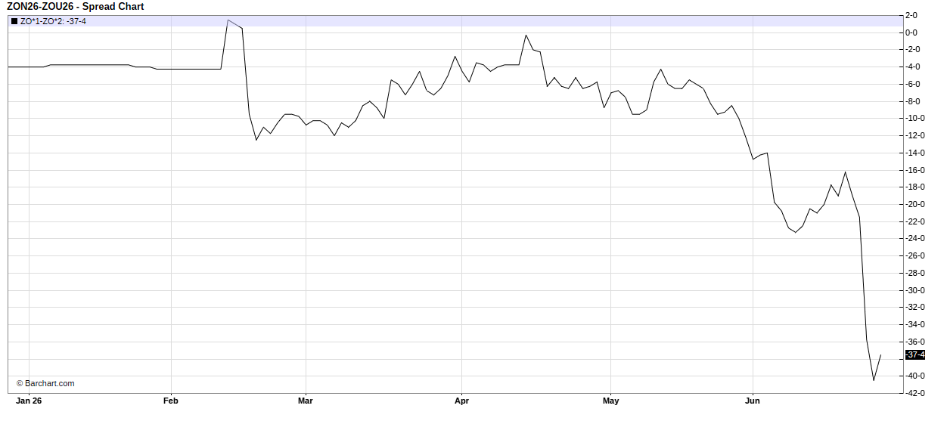

Over the past two weeks, the July/Sept spread has traded into a contango of $ 0.43.

This should be viewed as a red flag for any commodity futures trader.

In 2024, the CME increased storage rates for oats from approximately 6 cents per month to 8 cents per month.

Given that the most recent trade is closer to 21 cents per month, the July/ Sept spread has moved significantly beyond full carry.

The significance of a spread trading beyond carry should not be lost.

I have experienced spreads beyond full carry 4 times in the past 40 years, most recently crude oil in April of 2020.

Chart 1; July/Sept Oat Futures Spread

When a spread moves significantly beyond full carry, it is because the long is either unwilling or unable to take delivery.

In the 2020 crude oil case, the long was unable to take delivery due to contract specifications and limited delivery capacity.

It is impossible to determine why the long has decided to roll its position rather than go through the delivery process, but the effect is a complete breakdown of the July/Sept relationship.

The risk is to the downside of the July, it essentially becomes a “falling knife” much like the May 2020 crude oil contract.

If excessive contango persists in the oat futures contract for an extended period, the oat contract will not serve as a price risk-management tool for the perpetual long hedger.

Likewise, it will not offer a viable trading strategy for speculative positions.

Ultimately, unless measures are taken to make the playing field more “level” between the long and short, the contract will fail.

As a final point, the above analysis is focused on the significance of calendar spreads.

For trading strategies limited to the front month, adopting spreads in their analysis would benefit them.

Happy Trading

Brent Futz (b.futz@hotmail.com)

Brent covers this technical setup and specific price targets in depth in the The Spread Trader

Join 3,500+ farmers getting sell signals and technical roadmaps here:

Trent Klarenbach, BSA AgEc, PAg, publishes the Klarenbach Grain Report, Klarenbach Special Crops Report and The Spread Trader newsletters.

Klarenbach Research

Sign up below for a FREE trial of our newsletters

Wheat Canola Corn Soybeans Soybean Oil Spring Wheat Soybean Meal Hard Red Winter Oil Oats

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)