/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

With semiconductor giant Nvidia (NVDA) suffering a noticeable downturn in recent sessions, it raises an obvious question: is NVDA stock worth buying today? To spare you the suspense, I believe the answer is “yes” — but with an important caveat.

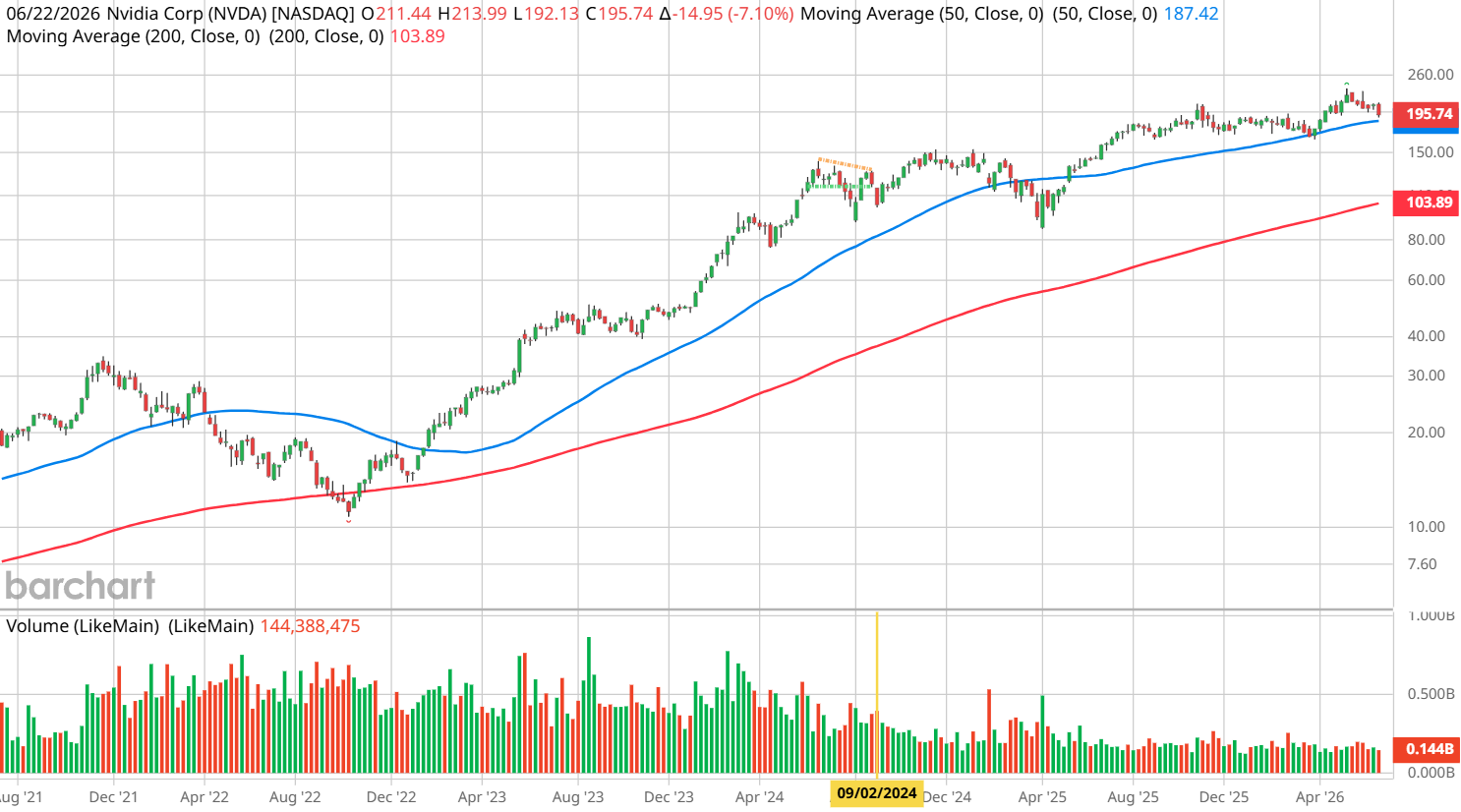

First, let’s consider the basic background that leads us to the potential bull case. Since the beginning of this year, NVDA stock has only gained 5%, a far cry from its blistering performance just a few short years ago. Further, in the trailing month, the security has slipped nearly 9%. Because Nvidia still commands a fundamental fortress, the equity potentially offers a contrarian trade.

Optimists will likely point to the cheapened multiple. Right now, NVDA stock trades at a little over 22-times forward earnings. At the end of July last year, this multiple stood at nearly 40. Subsequently, some folks are quick to jump on the idea that Nvidia is being offered at a compelling discount.

Still, it’s best to avoid a kneejerk reaction to “cheap” multiples. For one thing, tech hardware companies are inherently cyclical. While a software company scales via highly predictable and recurring services revenue, chip architects rely on large-scale infrastructure deployment cycles (capex). That’s fine until hyperscale cloud providers decide to pause or slow their infrastructure buildouts, mathematically causing the multiple to snap backward.

Another point to consider is hardware margin degradation. When NVDA stock traded at its peak multiple, this lofty level symbolized a near-monopoly on high-performance AI computation, thus pushing Nvidia’s gross margins to historic highs. However, with alternative foundries ramping up capacity, it’s going to be difficult for the tech giant to maintain such margins.

It’s very possible, then, that investors simply don’t want to pay the prior premium to earnings. That’s not to say that Nvidia stock isn’t cheap; rather, I’m simply hesitating to absolutely declare a discount based on a mathematical function without considering the context.

Using an Inductive Model to Analyze NVDA Stock

If NVDA stock isn’t necessarily a fundamental discount, is there a reason to consider buying it at this juncture? Let’s consider the basic presupposition of why people believe Nvidia is cheap right now. The theory goes that for NVDA to continue its downward trek, any bad news has to be significantly repugnant. However, because the bears may be in an exhausted state, any bit of good news could disproportionately have a positive impact.

While I’d probably guess that most of us accept this instinct, trading this sentiment is a matter of opinion. Fortunately, with the technology that we have today, we can measure the expected performance of this philosophy. If this forecast can reliably exceed the baseline random performance of NVDA stock, there just might be an opportunity.

Using a dataset going back to January 2019, if we were to buy Nvidia stock and hold it for a 10-week period, the expected forward distribution would place shares between $185 and $230 (assuming a starting price of $195.74), with probability density peaking at around $212.50. In other words, NVDA features an upside bias, with an expected return of 8.56%.

As mentioned earlier, NVDA stock has suffered a slowdown in momentum recently. In the last 10 weeks, shares only printed four up weeks, leading to an overall downward slope. Conditioned for this specific signal, NVDA’s expected 10-week distribution is only between $190 and $225. For the select time period, there’s no statistical incentive in trading this contrarian signal.

However, the near-term picture is nuanced. Over the next five weeks, NVDA stock would be expected (on a median basis) to reach $213 following the flashing of the aforementioned signal. If you were to trade NVDA randomly over the next five weeks, the expected median endpoint would be around $208.

While the outright variance is small (only 2.4%), there is a positive difference between conditionally trading NVDA stock on the previously mentioned signal versus the random benchmark. Combined with the leverage of options, there may be an exploitable opportunity for debit-side traders.

Following the Math

If you have faith in the inductive model, the trade that arguably looks the most enticing is the 205/210 bull call spread expiring July 31. This spread gives you a little more than five weeks for Nvidia stock to rise through the $210 strike at expiration, which it has a legitimate chance of doing based on prior empirical data. Additionally, the cost of each spread is relatively cheap at $170.

If NVDA stock manages to rise through the second-leg strike at expiration, you’d be looking at a maximum payout of over 194%.

Of course, the issue with all options is that they eventually expire. Admittedly, a July 31 expiration date doesn’t give you a whole lot of time for the proposed thesis to pan out. However, based on the inductive data that I extracted, NVDA would be expected to have a negative performance variance relative to the random baseline starting from around the sixth to seventh week. Thus, I’d like to cut off exposure before the trade turns against me.

Having said all that, inductive models always flirt with the black swan risk: just because trends recurred in the past does not necessarily mean they will repeat as expected in the future. Still, if you believe that pattern recognition is statistically more likely to give you an edge, NVDA stock is worth keeping on your radar — but only for a narrow window.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Delta%20Air%20Lines%2C%20Inc_%20passanger%20plane-by%20viper-zero%20via%20iStock.jpg)